Key figures

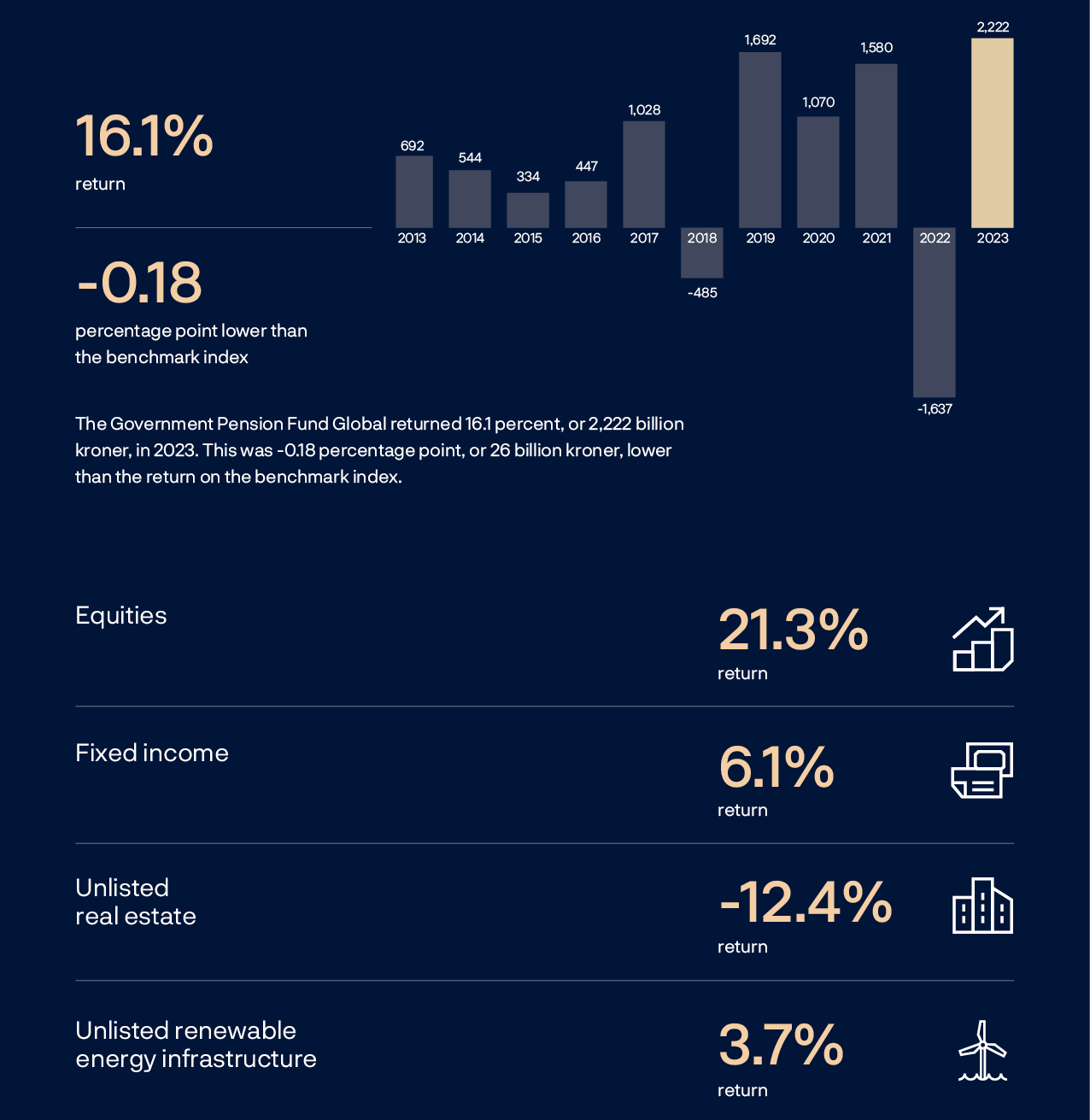

Return

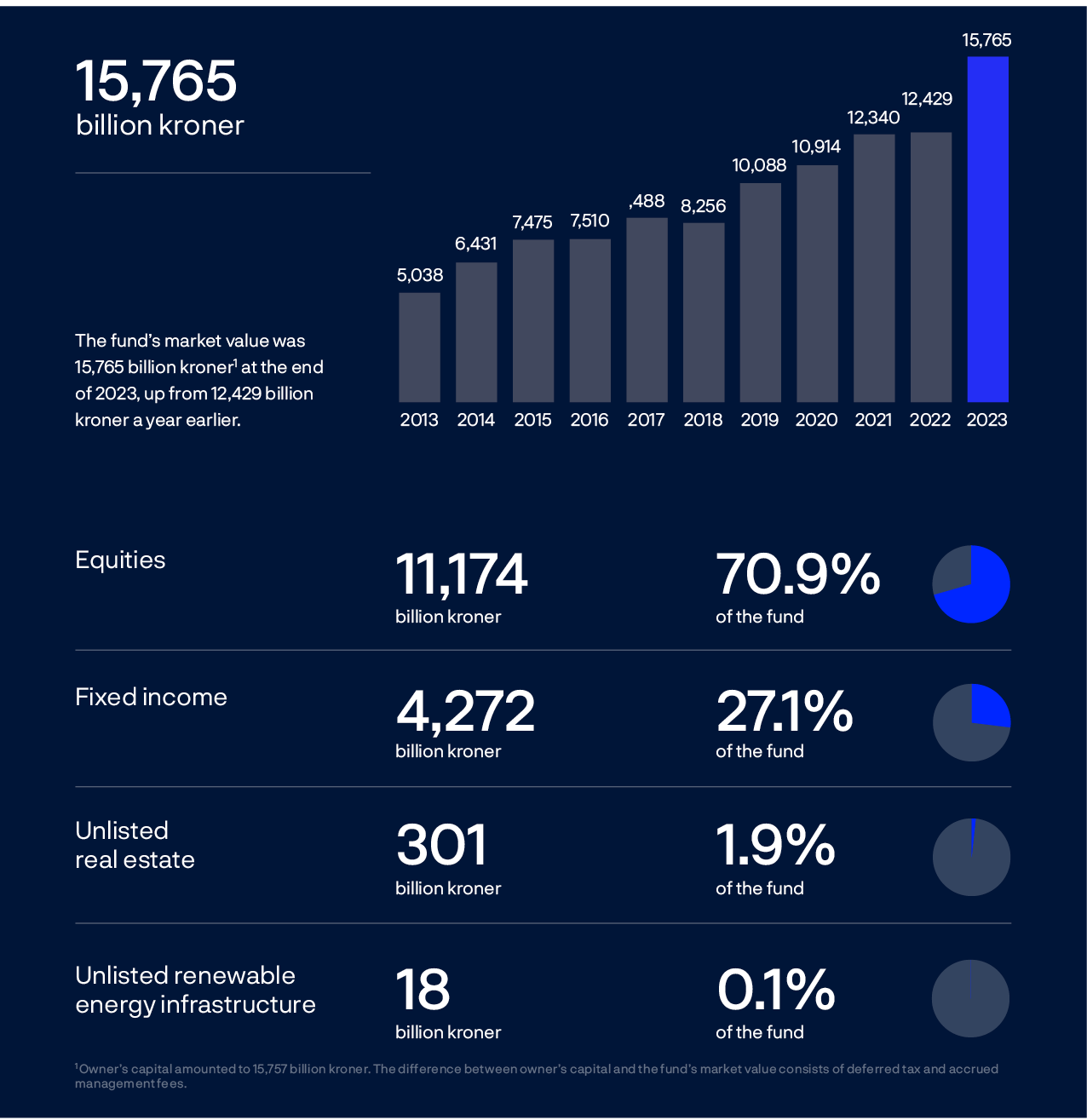

Market value

The Executive Board’s assessment of the results

The investments in the Government Pension Fund Global returned 16.1 percent in 2023. There was considerable variation between the results for the different investment strategies. Overall, the return was 0.18 percentage point less than on the benchmark index. Over time, however, the return has been higher than the return on the benchmark index.

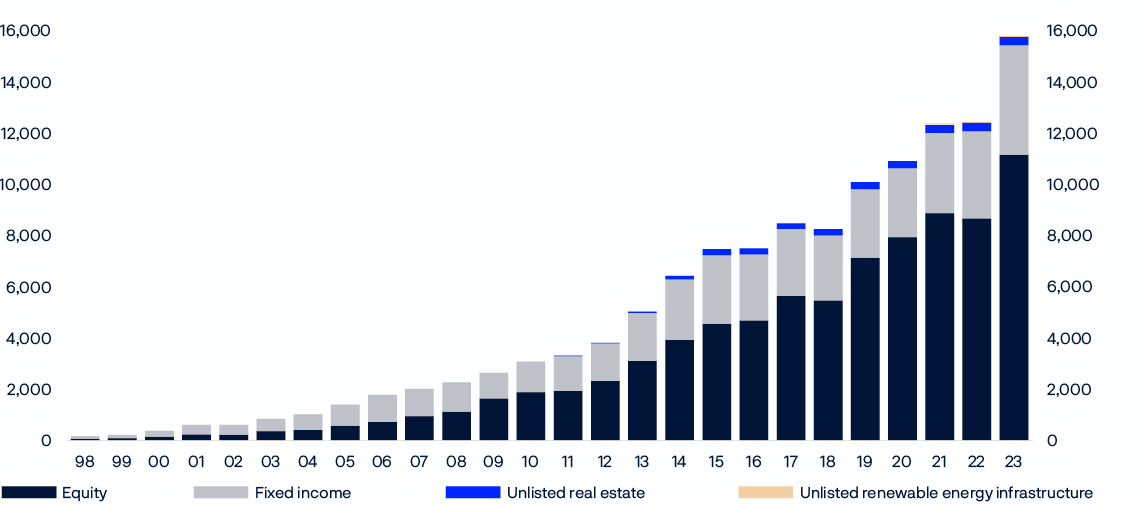

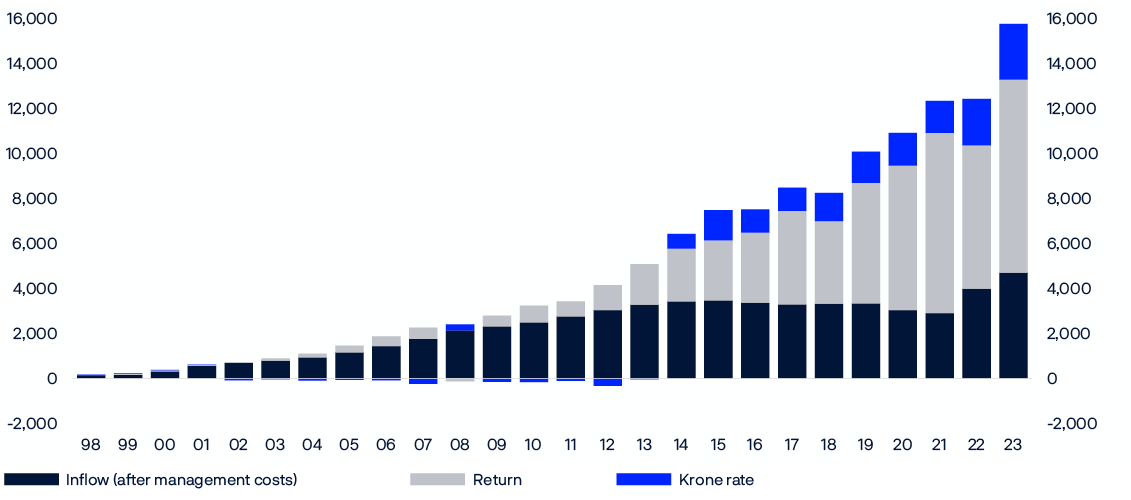

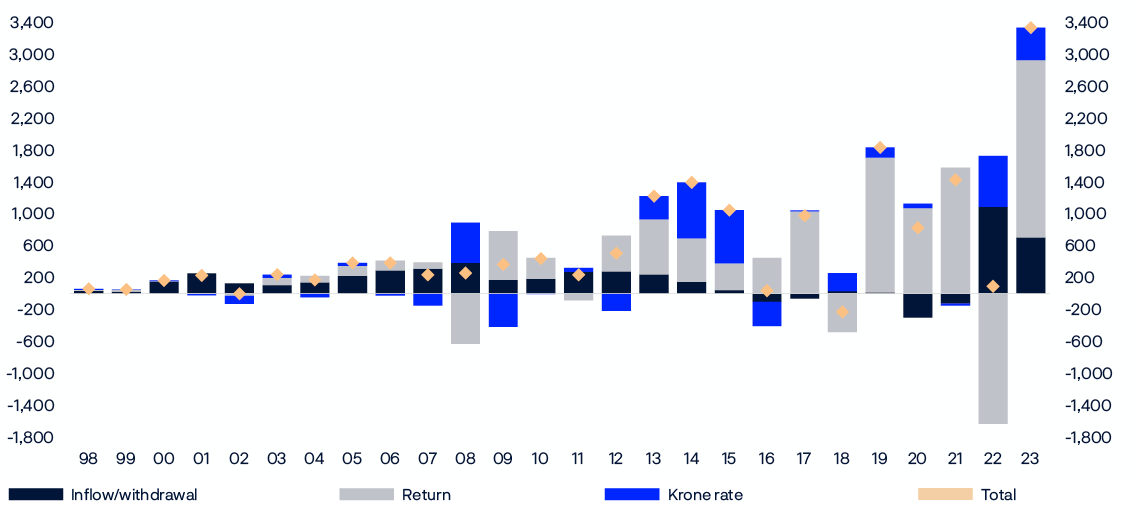

The fund’s market value increased by 3,336 billion kroner during the year to 15,765 billion kroner at the end of 2023. The increase was due mainly to strong returns on the fund’s equity and fixed-income investments. High prices for sales of oil and gas led to a net inflow of capital from the government of 704 billion kroner after the payment of management fees. A weaker krone against the currencies in which the fund is invested also increased its market value measured in kroner.

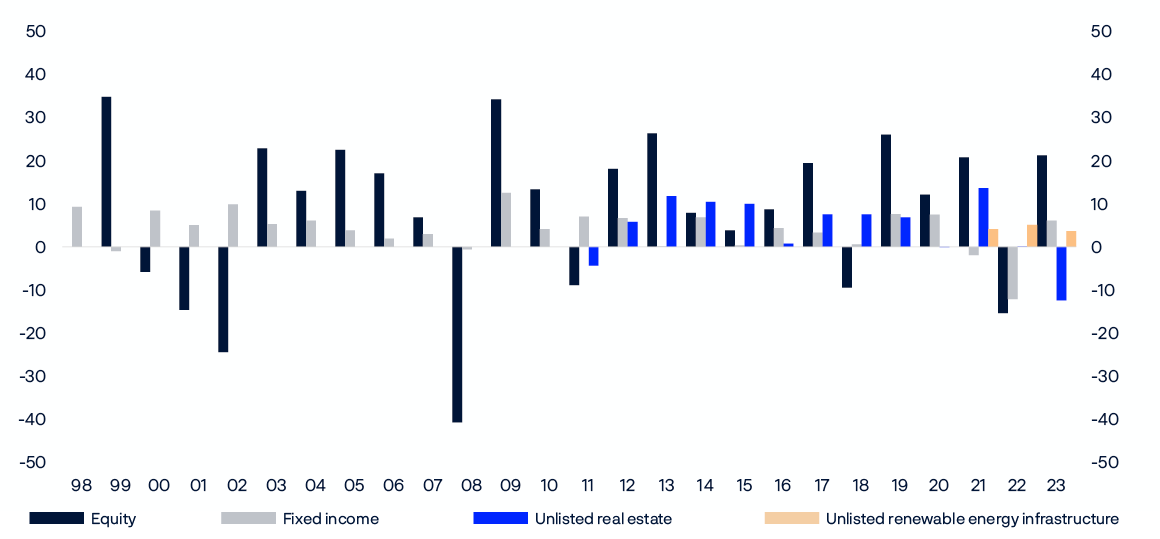

Measured in the fund’s currency basket, the return for the year was 16.1 percent, or 2,222 billion kroner, before management costs. Equities returned 21.3 percent. Stock markets were lifted by a surge in prices for technology stocks. A continued rise in central bank policy rates due to high inflation affected bond markets, but a drop in long yields towards the end of the year contributed to a return on fixed-income investment of 6.1 percent in 2023.

Investments in unlisted real estate returned -12.4 percent, and unlisted renewable energy infrastructure 3.7 percent. The return on unlisted real estate was weak both in absolute terms and relative to other asset classes. The return was pulled down by lower valuations as a result of higher real interest rates and decreased demand for office properties since the pandemic.

The fund’s investments at the end of the year broke down into 70.9 percent equities, 27.1 percent fixed income, 1.9 percent unlisted real estate and 0.1 percent unlisted renewable energy infrastructure.

With such a large fund and an equity share of around 70 percent, we have to be prepared for considerable fluctuations in the fund’s return and market value. Each year, Norges Bank publishes the results of both historical and hypothetical stress tests. The tests conducted at the end of 2023 include shocks such as an economic recession linked to high public and private debt, long-term geoeconomic conflict and repricing of the equity market. In these stress tests, the decrease in the value of the fund is estimated at around 30 percent over a period up to five years.

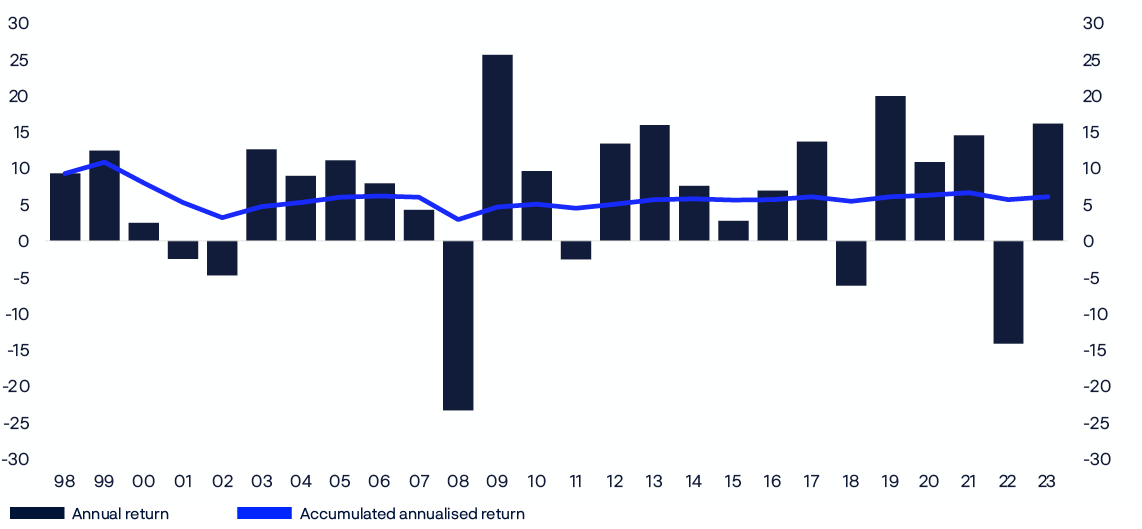

The Executive Board considers the return on the fund over time to have been good. In the period from 1998 to 2023, the average annual return was 6.1 percent. The annual net real return, after deductions for inflation and management costs, was 3.8 percent in the same period.

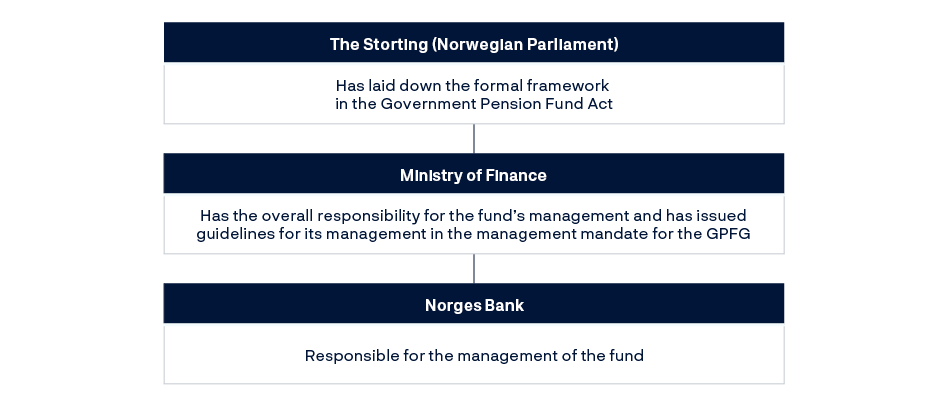

Norges Bank manages the fund with a view to achieving the highest possible long-term return within the constraints laid down in the mandate from the Ministry of Finance. The return achieved by Norges Bank is measured against the return on the fund’s benchmark index. In 2023, the fund’s return was 0.18 percentage point less than the return on the benchmark index.

Norges Bank’s investment strategies are grouped into three main categories: market exposure, security selection and fund allocation. These strategies are complementary and aim to take advantage of the fund’s size and long investment horizon. Each strategy has evolved over time.

Under the strategy for market exposure, the fund is invested broadly in the equities and bonds included in the benchmark index. The investments are made cost-effectively and with a view to contributing to the objective of the highest possible return. The strategy for security selection is based on fundamental analysis of companies, and Norges Bank uses both internal and external managers. Fund allocation consists of a number of strategies that aim to improve the fund’s long-term risk and return characteristics. Investments in real estate and unlisted renewable energy infrastructure are part of the fund allocation strategy.

The results for both market exposure and security selection were good in 2023 and contributed positively to the fund’s relative return. However, the results for fund allocation, especially investments in unlisted real estate, meant that the fund’s overall return before costs was 0.18 percentage point lower than the return on the benchmark index.

The fund’s unlisted real estate investments are almost entirely in office, logistics and retail properties. Office properties account for around half of the portfolio, and investments in office and retail premises are concentrated in a small number of major cities. Higher real interest rates since the pandemic have resulted in weak returns on real estate in general, and especially in the part of the office market where the fund is invested. The rise in working from home following the pandemic has also reduced demand for office space. The fund’s office properties returned -15.4 percent in 2023. The valuation of the office portfolio peaked in the first quarter of 2022 and has since been written down by 25.2 percent.

Unlisted real estate is not part of the benchmark index and is funded by investing less in equities and bonds. Substantial variations may occur between the return on real estate investments and their funding from year to year. The results must be assessed over time. The return on unlisted real estate investments in 2023 was considerably lower than the return on the equities and bonds sold to fund them. This meant that unlisted real estate made a contribution of -0.58 percentage point to the fund’s relative return.

Investments in listed real estate returned 16.6 percent in 2023. In isolation, this made a positive contribution to the fund’s relative return of 0.11 percentage point. The value of these investments fluctuated widely during the year but surged in the fourth quarter along with the rest of the equity market.

There was considerable variation in the results of the different investment strategies in 2023. The Executive Board considers it important for the fund’s performance to be assessed as a whole and over time, and is satisfied that the overall return over time has been higher than the return on the benchmark index, against which the return is measured.

Norges Bank has reported contributions to the relative return for the same three strategies in the period from 2013 to 2023. In this period, the average annual excess return before management costs was 0.29 percentage point. Market exposure and security selection made positive contributions to the relative return, while fund allocation made a negative contribution.

In the period from 1998 to 2023, the average annual return before management costs was 0.28 percentage point higher than the return on the benchmark index from the Ministry of Finance.

The objective of the highest possible return is to be achieved with acceptable risk. The risk in the fund is measured, analysed and followed up using a broad set of measures and different types of analysis. The management mandate requires Norges Bank to manage the fund with a view to ensuring that expected relative volatility (tracking error) does not exceed 1.25 percentage points. Expected relative volatility was 0.34 percentage point at the end of 2023, compared with 0.39 percentage point a year earlier.

Measured over the full period from 1998 to 2023, realised relative volatility has been 0.64 percentage point.

The management of the fund is to be cost-effective. Low costs are not an end in themselves, but cost-effective management supports the objective of the highest possible return after costs. In the period from 2013 to 2023, annual management costs averaged 0.05 percent of assets under management. In 2023, management costs amounted to 6.6 billion kroner, or 0.05 percent of assets under management. The Executive Board is satisfied that management costs are low compared with other managers.

The mandate from the Ministry of Finance requires responsible investment to be an integral part of the management of the fund. A good long-term return depends on sustainable economic, environmental and social development. Norges Bank published expectations of companies on consumer interests during the year, as well as views on the responsible use of artificial intelligence.

Climate risk management is a priority for responsible investment, and in 2023 Norges Bank published sharpened expectations for how companies should manage climate risk and views on the use of voluntary carbon credits. A number of companies in the portfolio committed to net zero carbon emissions during the year.

It is hard to measure the effects of work on responsible investment. Provisional results from a research project in 2023 indicate that Norges Bank’s publication of its voting decisions five days before shareholder meetings leads to increased support for the fund’s position from other shareholders.

Norges Bank’s Executive Board

A tremendous year

I began my introduction to last year’s annual report by calling 2022 “a turbulent year”. War, inflation and plummeting tech stocks had all impacted the fund negatively.

Was 2023 any less turbulent? By no means. There was even more war and conflict around the world, and inflation remained high in many countries. But equity markets – and especially US tech stocks – bounced back strongly. The big losers in 2022 were the big winners in 2023.

Some of these companies are so large and valuable that they make up more of the fund than all of our investments put together in countries such as Sweden and Australia. Microsoft, Apple and Nvidia contributed most to the fund’s return for the year.

2023 was also the year when AI was on everyone’s lips. Again, it was the tech clusters on the US West Coast that led the way. AI will undoubtedly affect the fund, both in the way we work and not least at the companies we invest in.

The fund's value increased by 90 billion kroner in 2022. In 2023 the fund’s market value jumped 3,336 billion kroner, thanks mainly to a strong return of 2,222 billion kroner and a weak krone. This took the fund past the 16 trillion kroner mark for the first time.

In 2023, we were also named the world's most open and transparent investment fund in the Global Pension Transparency Benchmark. Openness builds trust, and trust is capital which we are completely reliant on as an investment fund but can by no means take for granted. This ranking provides real motivation to continue to be as open as possible.

It is in our interest for everyone to know our views on the markets and how companies can be run as sustainably as possible. It is also in our interest for our owners – the Norwegian people – to know how we invest on their behalf.

2023 was a tremendous year for the fund. We saw the biggest increase in the value of the fund in its history, and we were crowned the world’s most transparent investment fund for the first time. Openness, as I say, is important for trust.

Eagle-eyed readers will have noticed a degree of alliteration as we moved from “a turbulent year” to“a tremendous year”. Trust also begins with a T.

Oslo, 27 February 2024

Nicolai Tangen

CEO, Norges Bank Investment Management

Strong return on the fund’s investments

The Government Pension Fund Global returned 16.1 percent, or 2,222 billion kroner, in 2023. The return in kroner was the largest in the fund’s history.

The fund’s market value grew by a record 3,336 billion kroner in 2023. A strong return on the fund’s equity investments made the greatest contribution to this growth. The krone also weakened against many of the currencies the fund is invested in, and there was an inflow of capital from the government.

The fund’s investments spanned 72 countries and 43 currencies at the end of the year. The fund is invested in international securities and unlisted real estate and infrastructure in foreign currency. We measure returns in a basket of international currencies. This basket is defined in the management mandate as a weighted combination of the currencies in the fund’s benchmark indices for equities and bonds, and consisted of 35 currencies at the end of 2023. Unless otherwise stated, the results in this report are measured in this currency basket.

TABLE 1 The fund's ten largest holdings in percent as at 31 December 2023, by country.

|

Country |

Total |

Equity |

Fixed income |

Unlisted real estate |

Unlisted infrastruture |

|---|---|---|---|---|---|

|

US |

46.9 |

33.8 |

12.2 |

0.9 |

|

|

Japan |

7.4 |

4.9 |

2.5 |

0.0 |

|

|

UK |

6.3 |

4.3 |

1.6 |

0.4 |

|

|

Germany |

4.8 |

2.5 |

2.2 |

0.1 |

0.0 |

|

France |

4.4 |

3.0 |

1.1 |

0.3 |

|

|

Switzerland |

3.4 |

2.8 |

0.5 |

0.1 |

|

|

Canada |

3.0 |

1.4 |

1.6 |

||

|

Netherlands |

2.3 |

1.6 |

0.6 |

0.0 |

0.1 |

|

China |

2.1 |

2.1 |

0.0 |

||

|

Australia |

2.0 |

1.4 |

0.6 |

CHART 1 The fund’s investments as at 31 December 2023. Equities, unlisted real estate and infrastructure distributed by country and bonds by currency. In percent.

TABLE 2 Return figures in percent.

|

2023 |

2022 |

20211 |

2020 |

2019 |

|

|---|---|---|---|---|---|

|

Returns measured in the fund's currency basket |

|||||

|

Equity investments |

21.25 |

-15.36 |

20.76 |

12.14 |

26.02 |

|

Fixed-income investments |

6.13 |

-12.11 |

-1.93 |

7.46 |

7.56 |

|

Unlisted real estate investments |

-12.37 |

0.07 |

13.64 |

-0.08 |

6.84 |

|

Unlisted infrastructure investments |

3.68 |

5.12 |

4.15 |

||

|

Return on fund |

16.14 |

-14.11 |

14.51 |

10.86 |

19.95 |

|

Relative return on fund (percentage points) |

-0.18 |

0.87 |

0.75 |

0.27 |

0.23 |

|

Management costs |

0.05 |

0.04 |

0.04 |

0.05 |

0.05 |

|

Return on fund after management costs |

16.09 |

-14.15 |

14.47 |

10.81 |

19.90 |

|

Returns in kroner |

|||||

|

Equity investments |

26.26 |

-9.27 |

20.67 |

12.70 |

28.20 |

|

Fixed-income investments |

10.51 |

-5.78 |

-2.01 |

8.00 |

9.41 |

|

Unlisted real estate investments |

-8.75 |

7.27 |

13.55 |

0.42 |

8.68 |

|

Unlisted infrastructure investments |

7.96 |

12.69 |

7.24 |

||

|

Return on fund |

20.93 |

-7.93 |

14.42 |

11.41 |

22.01 |

1 First unlisted infrastructure investment was made in second quarter of 2021.

TABLE 3 Historical key figures as at 31 December 2023. Annualised data, measured in the fund's currency basket.

|

Since 01.01.1998 |

Last 15 years |

Last 10 years |

Last 5 years |

Last 12 months |

|

|---|---|---|---|---|---|

|

Fund return (percent) |

6.09 |

8.46 |

6.71 |

8.72 |

16.14 |

|

Annual price inflation (percent) |

2.10 |

2.29 |

2.43 |

3.52 |

3.20 |

|

Annual management costs (percent) |

0.08 |

0.06 |

0.05 |

0.05 |

0.05 |

|

Net real return on fund (percent) |

3.83 |

5.96 |

4.13 |

4.97 |

12.49 |

|

The fund's actual standard deviation (percent) |

8.46 |

9.42 |

9.62 |

12.05 |

10.68 |

|

Relative return on fund (percentage points)1 |

0.28 |

0.53 |

0.22 |

0.42 |

-0.18 |

|

The fund's tracking error (percentage points)1 |

0.64 |

0.53 |

0.41 |

0.46 |

0.44 |

|

The fund's information ratio (IR)1,2 |

0.44 |

0.95 |

0.51 |

0.83 |

-0.42 |

1Based on aggregated equity and fixed-income investments until end of 2016.

2The fund's information ratio (IR) is the ratio of the fund's average monthly relative return to the fund's tracking error. The IR indicates how much relative return has been achieved per unit of relative risk.

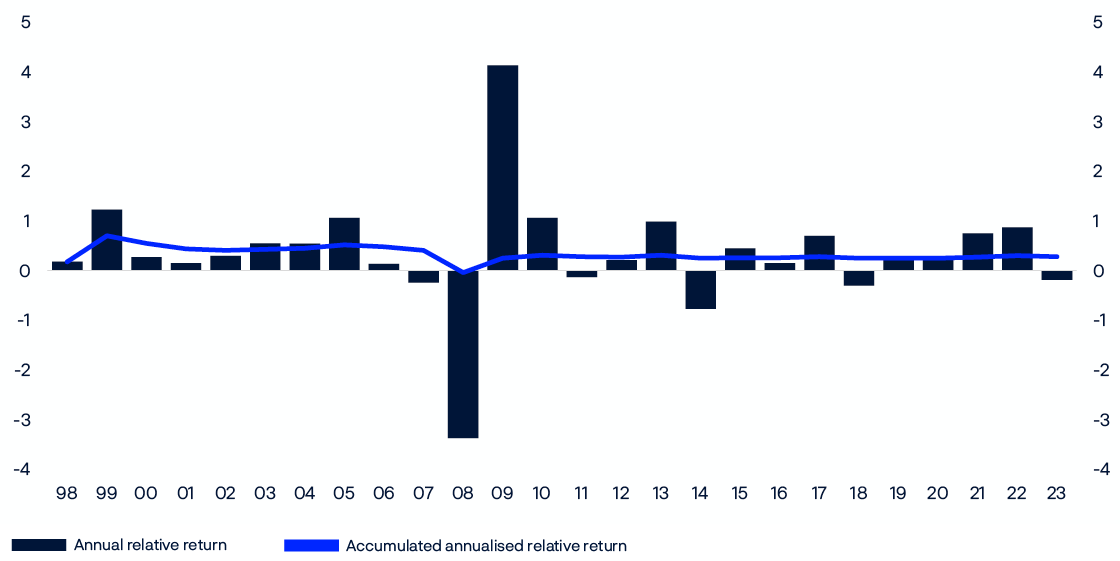

CHART 2 The fund’s annual return and accumulated annualised return in percent.

TABLE 4 Return on the fund in percent as at 31 December 2023, measured in various currencies.

|

Since 01.01.1998 Annualised figures |

2023 |

2022 |

2021 |

2020 |

2019 |

|

|---|---|---|---|---|---|---|

|

US dollar |

6.15 |

17.30 |

-17.58 |

11.09 |

14.35 |

20.24 |

|

Euro1 |

6.13 |

13.33 |

-12.18 |

19.53 |

4.90 |

22.45 |

|

British pound |

7.23 |

10.68 |

-7.19 |

12.12 |

10.82 |

15.59 |

|

Norwegian krone |

7.50 |

20.93 |

-7.93 |

14.42 |

11.41 |

22.01 |

|

Currency basket |

6.09 |

16.14 |

-14.11 |

14.51 |

10.86 |

19.95 |

1Euro was introduced as currency on 01.01.1999. WM/Reuters' euro rate is used as estimate for 31.12.1997.

TABLE 5Key figures in billions of kroner.

|

2023 |

2022 |

2021 |

2020 |

2019 |

|

|---|---|---|---|---|---|

|

Market value |

|||||

|

Equity investments |

11,174 |

8,672 |

8,878 |

7,945 |

7,145 |

|

Fixed-income investments |

4,272 |

3,412 |

3,135 |

2,695 |

2,670 |

|

Unlisted real estate investments |

301 |

330 |

312 |

273 |

273 |

|

Unlisted infrastructure investments1 |

18 |

15 |

14 |

||

|

Market value of fund2 |

15,765 |

12,429 |

12,340 |

10,914 |

10,088 |

|

Deferred tax |

-8 |

||||

|

Accrued, not paid, management fees3 |

0 |

0 |

1 |

-5 |

-4 |

|

Owner's capital2 |

15,757 |

12,429 |

12,340 |

10,908 |

10,084 |

|

Inflow of capital |

711 |

1,090 |

80 |

4 |

32 |

|

Withdrawal of capital |

0 |

0 |

-199 |

-302 |

-14 |

|

Paid management fees4 |

-7 |

-5 |

-10 |

-4 |

-5 |

|

Return on fund5 |

2,222 |

-1,637 |

1,580 |

1,070 |

1,692 |

|

Changes due to fluctuations in krone |

409 |

642 |

-25 |

58 |

127 |

|

Total change in market value |

3,336 |

90 |

1,426 |

826 |

1,832 |

|

Changes in value since first capital inflow in 1996 |

|||||

|

Total inflow of capital |

5,455 |

4,744 |

3,654 |

3,574 |

3,570 |

|

Total withdrawal of capital3 |

-687 |

-687 |

-687 |

-482 |

-182 |

|

Return on equity investments |

7,326 |

5,280 |

6,485 |

4,897 |

4,023 |

|

Return on fixed-income investments |

1,192 |

970 |

1,401 |

1,446 |

1,249 |

|

Return on unlisted real estate investments |

71 |

119 |

120 |

84 |

85 |

|

Return on unlisted infrastructure investments1 |

2 |

2 |

1 |

||

|

Management fees4 |

-70 |

-63 |

-58 |

-53 |

-48 |

|

Changes due to fluctuations in krone |

2,474 |

2,065 |

1,423 |

1,448 |

1,390 |

|

Market value of fund |

15,765 |

12,429 |

12,340 |

10,914 |

10,088 |

|

Return on fund |

8,592 |

6,370 |

8,007 |

6,427 |

5,358 |

|

Return after management costs |

8,522 |

6,307 |

7,949 |

6,374 |

5,309 |

1First unlisted infrastructure investment was made in the second quarter of 2021.

2From 2023, market value is presented before management fee receivable and deferred tax. Up to and including 2022, market value was presented before management fee receivable.

3Total inflow and withdrawal of capital shown in this table is adjusted for accrued, not paid, management fees.

4Management fees are describe in note 12 in the financial statements.

5Fund return reflects the return on the market value of the investment portfolio, that does not include deferred tax. The portfolio result of 2,214 million kroner in the financial statements includes the impact of changes in deferred tax.

CHART 3 Historical returns on the fund’s investments in percent, by asset class.

CHART 4 The fund’s market value in billions of kroner, by asset class.

CHART 5 The fund’s market value in billions of kroner.

CHART 6 Changes in the fund’s market value in billions of kroner.

Strong year for equity investments

The fund’s equity investments returned 21.3 percent in 2023. Despite strong inflation, rising policy rates and geopolitical turmoil, the stock market rallied after a weak 2022. Higher interest rates reined in inflation during the year without sparking a sharp economic downturn.

US technology stocks in particular contributed to the positive return, driven mainly by the largest technology companies.

Tech stocks perform best

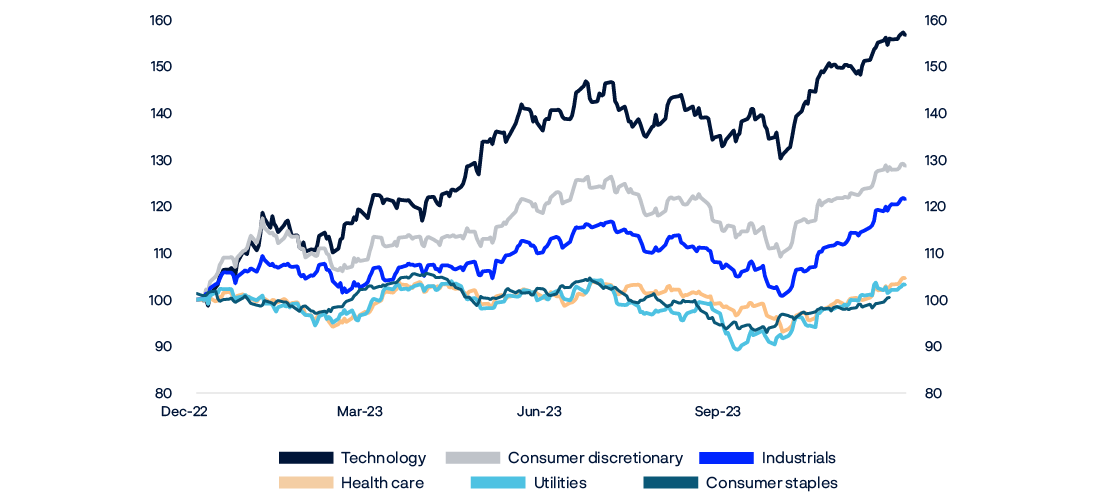

Technology stocks were the best performers in 2023 with a return of 51.9 percent. The sector benefited from efficiencies and increased demand for new AI solutions from the biggest internet and software companies and their semiconductor suppliers.

Consumer discretionary was the next-strongest sector, returning 26.0 percent. Consumption and economic activity generally held up over the year despite higher prices and rising interest rates, but there were signs of weaker demand in the second half, especially among producers of luxury goods and drinks.

Industrials were the third-strongest sector with a return of 22.1 percent. Despite fears of recession, demand remained strong. Prices for products held up despite the strong inflation of 2022. Raw materials costs fell, and in many cases this led to higher margins than expected.

Consumer staples produced the weakest return of 1.0 percent. Sales of household goods such as food and drink fell. Consumers adjusted to higher prices and shifted their spending towards activities such as travel and dining out.

Individual investments

The fund was invested in 8,859 companies at the end of 2023, down from 9,228 a year earlier. The decrease was mainly due to ongoing portfolio adjustments made by our internal and external managers.

The investments in technology companies Microsoft, Apple and Nvidia made the biggest contributions to the return for the year. The worst-performing investments were in health care company Pfizer, technology company Meituan and energy company NextEra Energy.

We participated in 45 initial public offerings during the year. The largest of these were at Adnoc Gas PLC, Kenvue Inc and in Societatea De Producere A Energiei Electrice. The offerings in which the fund invested the most were at Birkenstock Holding PLC and Maplebear Inc.

At the end of the year, the fund had holdings of more than 2 percent in 1,186 companies, and more than 5 percent in 65 companies. Its average holding in the world’s listed companies was 1.5 percent.

Excluding listed real estate companies, the largest percentage holding in any one company was in industrial company Nikola. The fund’s 9.2 percent stake was worth 950.9 million kroner. With the exception of listed real estate companies, the fund may hold no more than 10 percent of the voting shares in a company.

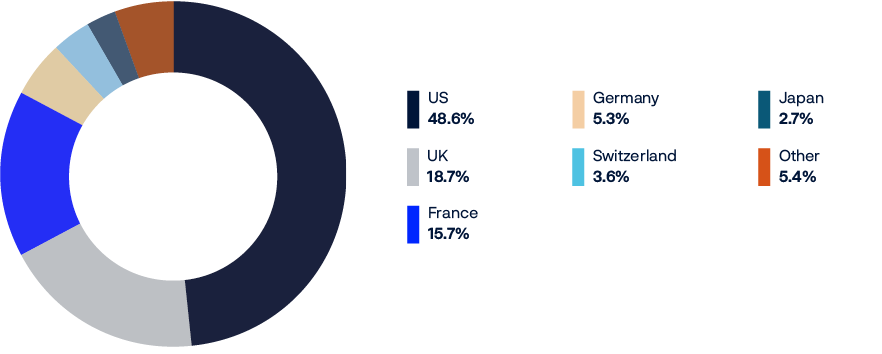

TABLE 6 Return on the fund's largest equity investments in 2023 by country. In percent.

|

Country |

Return in international currency |

Return in local currency |

Share of equity investments1 |

|---|---|---|---|

|

US |

27.0 |

28.3 |

48.6 |

|

Japan |

18.2 |

27.5 |

7.1 |

|

UK |

16.1 |

10.7 |

6.3 |

|

France |

19.7 |

16.8 |

4.3 |

|

Switzerland |

16.9 |

7.4 |

4.1 |

|

Germany |

23.7 |

20.7 |

3.6 |

|

China |

-14.4 |

-11.8 |

3.0 |

|

Australia |

23.6 |

20.6 |

2.2 |

|

Netherlands |

26.3 |

28.3 |

2.2 |

|

Canada |

34.4 |

35.6 |

2.1 |

1 Does not sum up to 100 percent because cash and derivatives are not included.

TABLE 7 Return on the fund's equity investments in 2023. Measured in international currency and sorted by sector. In percent.

|

Sector |

Return |

Share of equity investments1 |

|---|---|---|

|

Technology |

51.9 |

22.3 |

|

Financials |

18.3 |

15.0 |

|

Consumer discretionary |

26.0 |

14.1 |

|

Industrials |

22.1 |

13.1 |

|

Health care |

5.0 |

11.1 |

|

Consumer staples |

1.0 |

5.6 |

|

Real estate |

12.8 |

5.5 |

|

Basic materials |

10.8 |

4.0 |

|

Energy |

6.0 |

3.7 |

|

Telecommunications |

11.9 |

3.3 |

|

Utilities |

5.5 |

2.4 |

1 Does not sum up to 100 percent because cash and derivatives are not included.

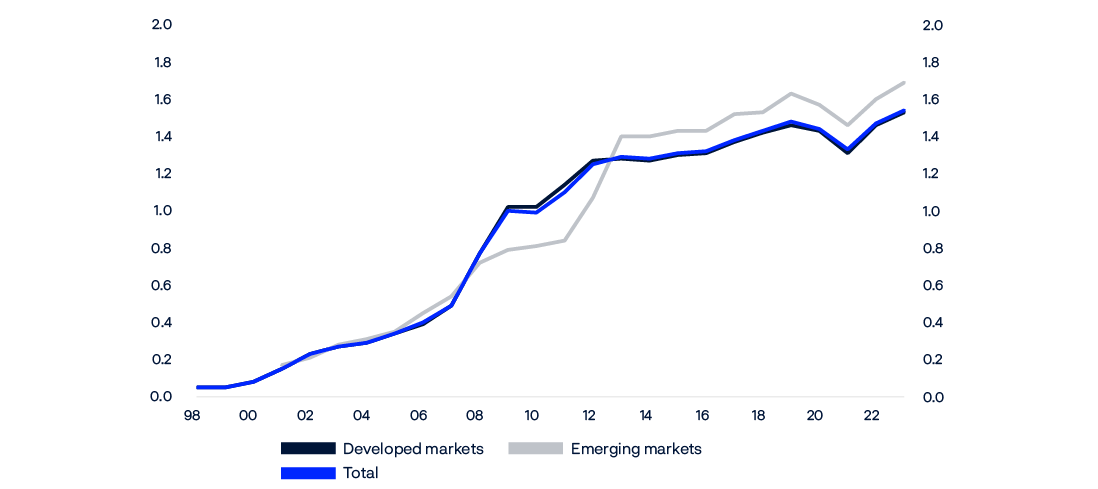

CHART 7 The fund’s holdings in equity markets. Percentage of market value of equities in the benchmark index.

Source: FTSE Russell, Norges Bank Investment Management

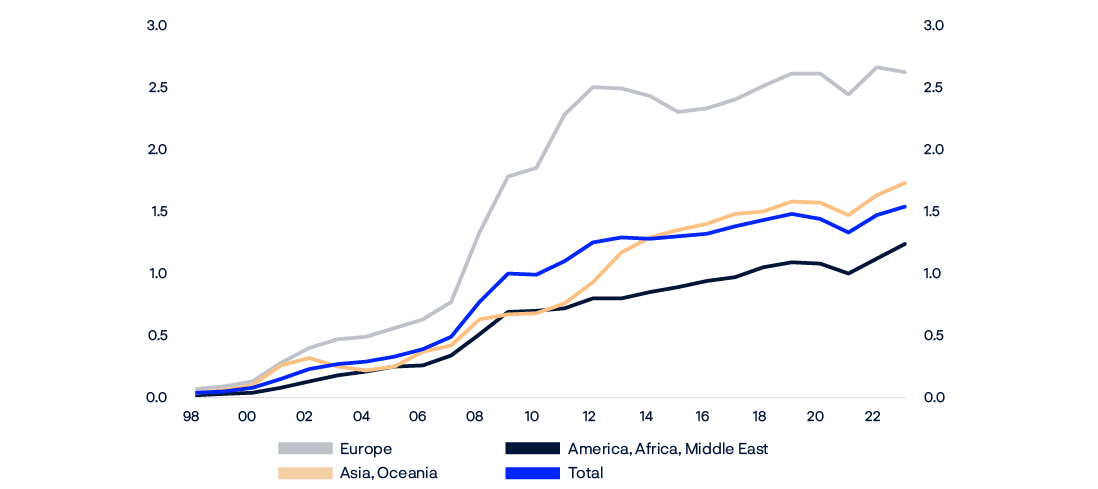

CHART 8 The fund’s holdings in equity markets. Percentage of market value of equities in the benchmark index.

Source: TSE Russell, Norges Bank Investment Management

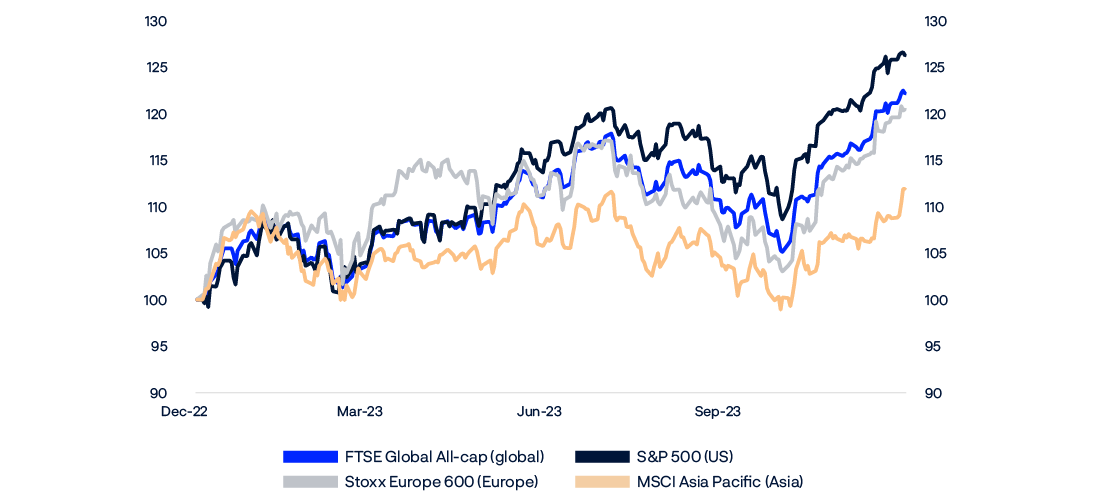

CHART 9 Price developments in regional equity markets. Measured in dollars. Indexed total return 31.12.2022 = 100.

Source: Bloomberg

CHART 10 Price developments of the three sectors with the highest and weakest return in the FTSE Global All Cap index. Measured in dollars. Indexed total return 31.12.2022 = 100.

Source: FTSE Russell

Positive return on fixed-income investments

The fund’s fixed-income investments returned 6.1 percent in 2023. Yields rose for much of the year before dropping back in the last two months.

The drop in yields at the end of the year was a result of inflation falling faster than expected. The world’s central banks, led by the Federal Reserve, therefore signalled rate cuts in the coming year.

Strongest return on corporate bonds

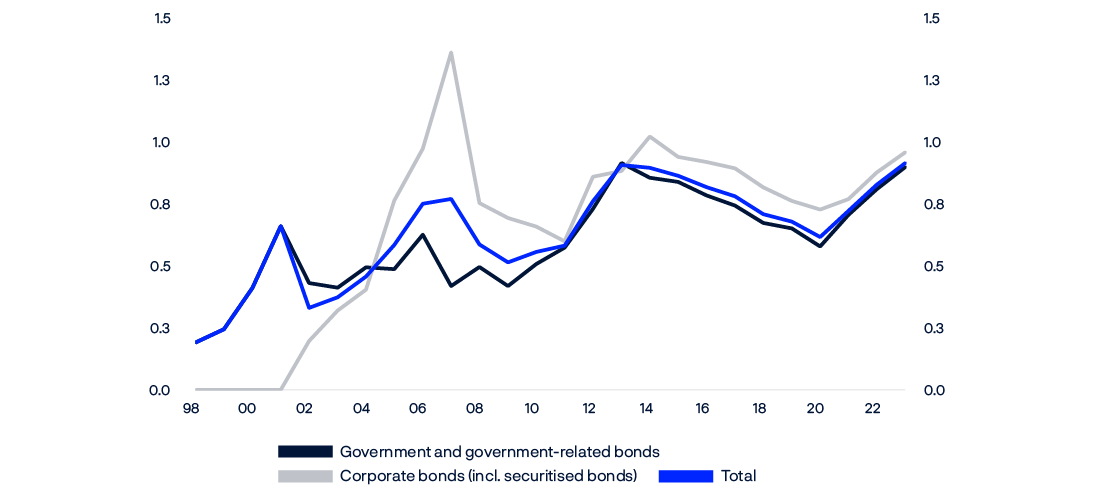

Government bonds returned 3.9 percent in 2023 and made up 60.7 percent of the fund’s fixed-income investments at the end of the year.

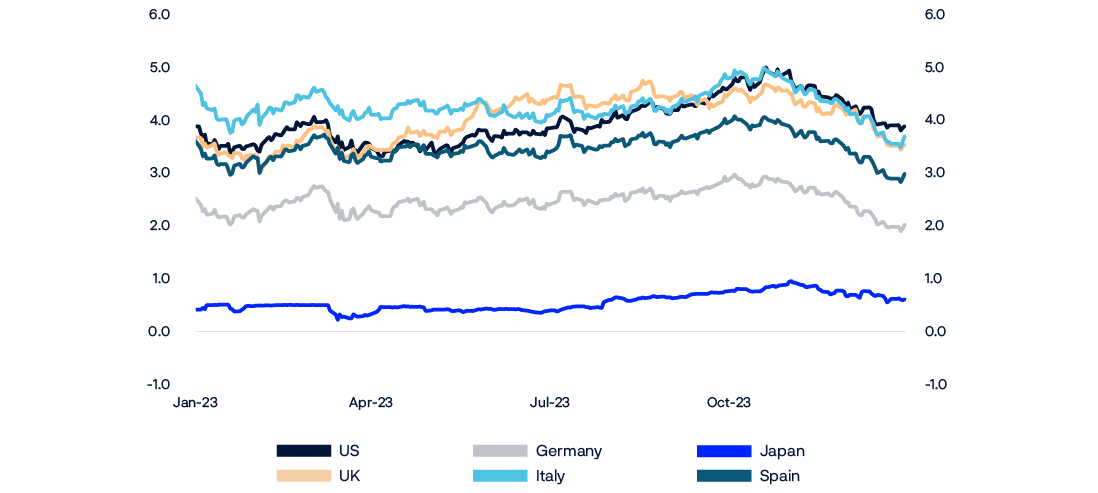

US Treasuries returned 3.1 percent and accounted for 28.3 percent of fixed-income investments. The Federal Reserve raised its policy rate by a total of 1 percentage point during the year in response to a tight labour market and high inflation. Ten-year Treasury yields hit 5 percent in October, their highest since 2007, before dropping back below 4 percent at the end of the year.

Euro-denominated government bonds returned 10.3 percent and amounted to 11.1 percent of fixed-income investments. The European Central Bank tightened its monetary policy considerably during the year, raising its policy rate by a total of 2 percentage points. This had little impact on market pricing of bonds with long maturities. Together with a strong euro, this resulted in good returns.

Japanese government bonds made up 8.0 percent of fixed-income holdings and returned -7.0 percent. The Bank of Japan made only minor adjustments to its monetary policy during the year. The weak return was mainly a result of a sharp fall in the yen during the year.

Corporate bonds returned 8.9 percent and made up 23.5 percent of the fund’s fixed-income investments at the end of the year. The return was boosted by a reduction in the credit premium, which is the compensation that investors demand for holding bonds of this type rather than less risky government bonds.

TABLE 8 Return on the fund's largest bond holdings by currency in 2023. In percent.

|

Currency |

Return in international currency |

Return in local currency |

Share of fixed-income investments |

|---|---|---|---|

|

US dollar |

4.8 |

5.8 |

49.3 |

|

Euro |

10.1 |

7.5 |

26.8 |

|

Japanese yen |

-6.9 |

0.4 |

8.6 |

|

Singapore dollar |

6.7 |

6.0 |

5.3 |

|

Canadian dollar |

7.6 |

5.7 |

5.1 |

|

British pounds |

10.3 |

5.1 |

4.9 |

|

Australian dollar |

6.1 |

6.5 |

2.3 |

|

Swiss franc |

17.1 |

7.6 |

0.8 |

|

Swedish krona |

7.7 |

5.2 |

0.7 |

|

New Zealand dollar |

5.4 |

6.4 |

0.6 |

TABLE 9 Return on the fund's fixed-income investments in 2023. Measured in international currency and sorted by sector. In percent.

|

Sector |

Return |

Share of fixed-income investments1 |

|---|---|---|

|

Government bonds2 |

3.9 |

60.7 |

|

Government-related bonds2 |

8.5 |

9.5 |

|

Inflation-linked bonds2 |

4.5 |

6.6 |

|

Corporate bonds |

8.9 |

23.5 |

|

Securitised bonds |

8.1 |

6.6 |

1Does not sum up to 100 percent because cash and derivatives are not included.

2Governments may issue different types of bonds, and the fund’s investments in these bonds are grouped accordingly. Bonds issued by a country’s government in the country’s own currency are categorised as government bonds. Bonds issued by a country’s government in another country’s currency are government-related bonds. Inflation-linked bonds issued by governments are grouped with inflation-linked bonds.

CHART 11 The fund’s holdings in fixed-income markets. Percentage of market value of bonds in the benchmark index.

SOURCE: Bloomberg Barclays Indices, Norges Bank Investment Management

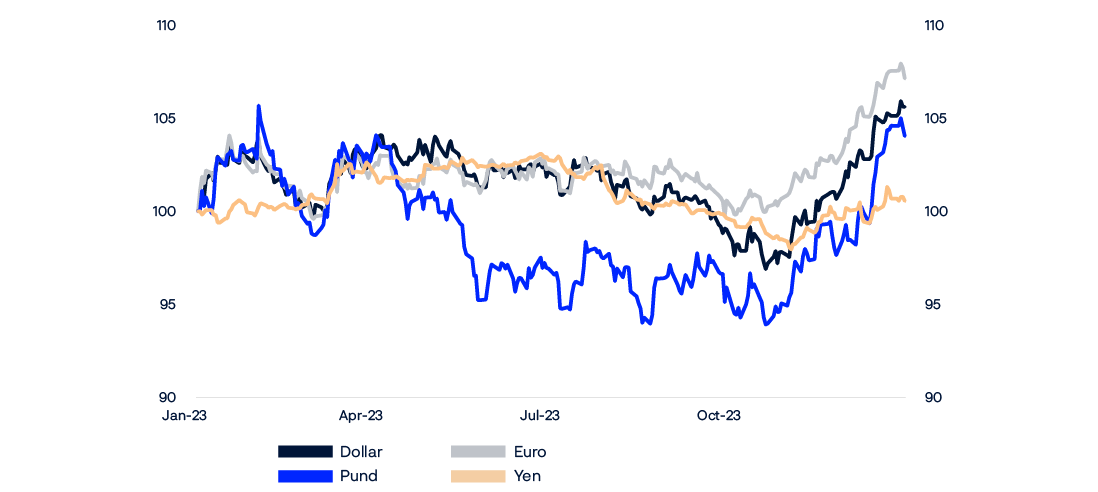

CHART 12 Price developments for bonds issued in various currencies. Measured in local currencies. Indexed total return 31.12.2022 = 100.

SOURCE: Bloomberg Barclays Indices

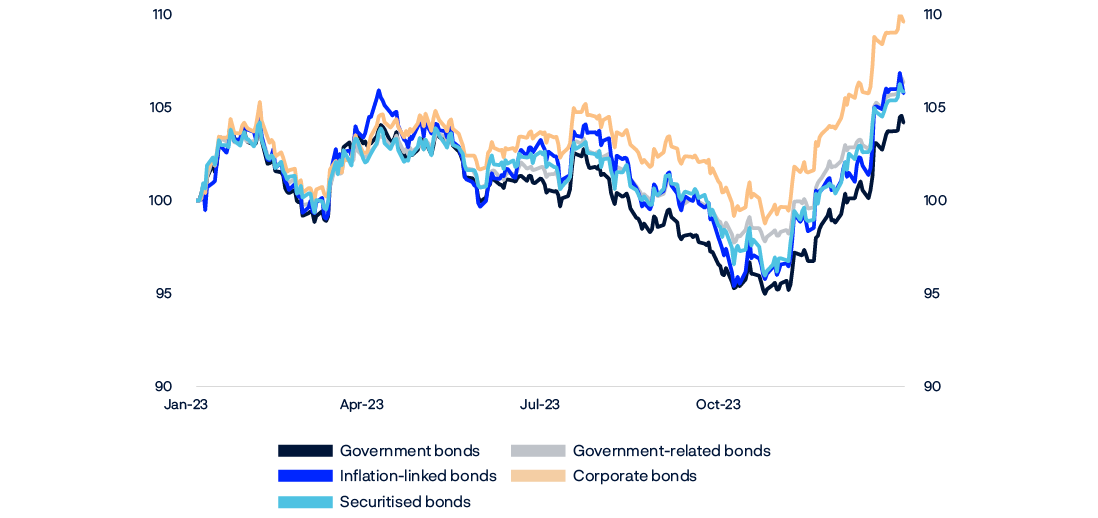

CHART 13 Price developments in fixed-income sectors. Measured in dollars. Indexed total return 31.12.2022 = 100.

SOURCE: Bloomberg Barclays Indices

CHART 14 10-year government bond yields in percent.

SOURCE: Bloomberg

Weak year for real estate

The fund’s investments in real estate returned -0.2 percent in 2023 and made up 3.9 percent of the fund at the end of the year. Unlisted real estate investments returned -12.4 percent, and listed real estate investments 16.6 percent.

The fund’s real estate strategy covers both unlisted and listed real estate investments. Altogether, these investments amounted to 611 billion kroner at the end of the year.

TABLE 10 Value of real estate investments in millions of kroner as at 31 December 2023.

|

Value1 |

|

|---|---|

|

Unlisted real estate investments |

301,128 |

|

Listed real estate investments |

309,443 |

|

Aggregated real estate investments |

610,572 |

1Including bank deposits and other receivables.

Unlisted real estate

The fund’s investments in unlisted real estate had a market value of 301 billion kroner at the end of the year, equivalent to 1.9 percent of the fund and 49.3 percent of our total real estate investments.

The fund’s unlisted real estate investments are almost entirely in office, retail and logistics properties. Office properties account for around half of the portfolio, and investments in office and retail premises are concentrated in a small number of major cities.

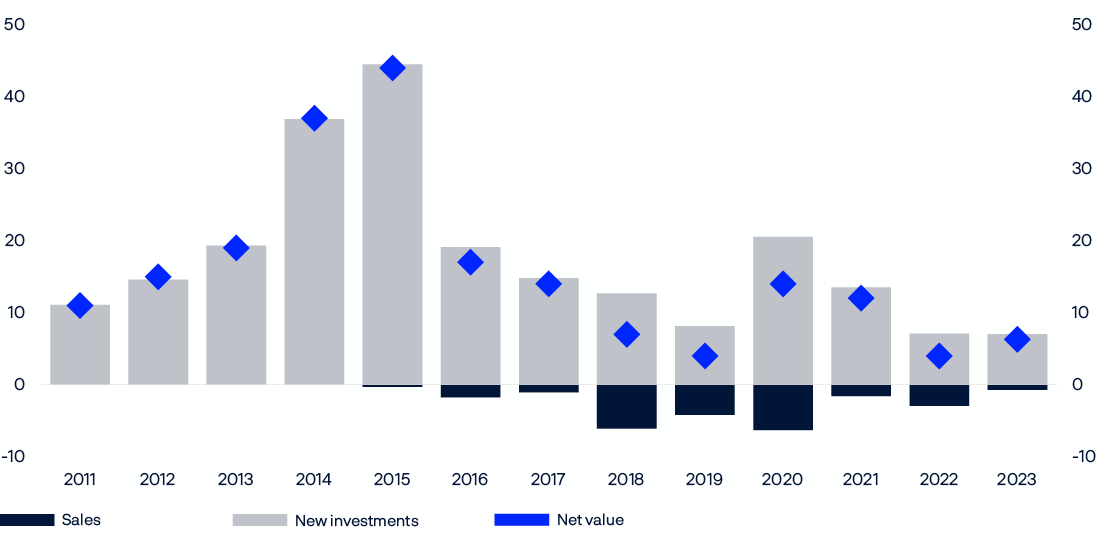

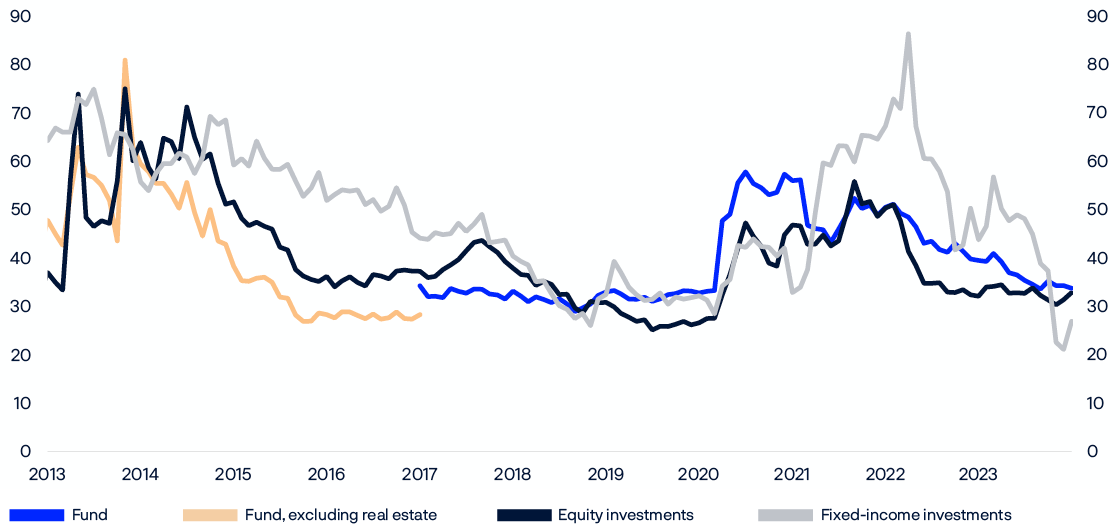

2023 was a year of uncertainty in the real estate market. The return on investments in unlisted real estate were affected by lower valuations in the wake of higher real interest rates and reduced demand for office space since the pandemic. The portfolio’s cumulative return peaked in mid-2022 and has since fallen by 22.4 percent.

The fund’s office properties returned -15.4 percent in 2023. The valuation of the office portfolio peaked in the first quarter of 2022 and has since been written down by 25.2 percent. Despite weaker valuations, rental income was stable from 2022 to 2023 and contributed 3.4 percentage points to the return for the year.

The management mandate from the Ministry of Finance sets an upper limit for unlisted real estate investments of 7 percent of the fund’s value. The fund has a long-term investment strategy and limited borrowing needs, which means that we can invest selectively when market corrections create attractive opportunities.

TABLE 11 Return on the fund's unlisted real estate investments in percentage points.

|

Since 01.04.2011 |

2023 |

2022 |

2021 |

2020 |

2019 |

|

|---|---|---|---|---|---|---|

|

Rental income |

3.7 |

3.4 |

3.1 |

3.4 |

3.4 |

3.6 |

|

Change in value |

1.2 |

-16.2 |

-3.0 |

9.8 |

-3.5 |

3.1 |

|

Transaction costs |

-0.7 |

-0.1 |

-0.1 |

-0.1 |

-0.2 |

-0.1 |

|

Currency effect |

0.2 |

1.1 |

0.1 |

0.2 |

0.3 |

0.1 |

|

Total (percent) |

4.3 |

-12.4 |

0.1 |

13.6 |

-0.1 |

6.8 |

TABLE 12 The fund's largest unlisted real estate investments as at 31 December 2023.

|

Retail, office and other by city1 |

Percent |

|---|---|

|

Paris |

21.8 |

|

London |

20.5 |

|

New York |

15.2 |

|

Boston |

13.9 |

|

Berlin |

7.0 |

|

Zurich |

5.7 |

|

Washington, D.C. |

5.4 |

|

San Francisco |

4.4 |

|

Tokyo |

4.1 |

|

Sheffield |

1.2 |

|

Cambridge |

0.5 |

1Excluding investments in logistics.

|

Logistics by country |

Percent |

|---|---|

|

US |

65.6 |

|

UK |

12.5 |

|

France |

4.5 |

|

Netherlands |

3.3 |

|

Spain |

3.0 |

|

Italy |

2.6 |

|

Germany |

2.4 |

|

Czech Republic |

2.3 |

|

Other countries |

3.8 |

TABLE 13 Return on the fund's unlisted real estate investment by market as at 31 December 2023. In percent.

|

Market |

Return |

Share of portfolio |

|---|---|---|

|

Europe |

-10.4 |

48.7 |

|

US |

-16.8 |

48.6 |

|

Japan |

5.1 |

2.7 |

CHART 15 The fund’s unlisted real estate investments by sector as at 31 December 2023.

1Other sectors, bank deposits and other claims.

CHART 16 The fund’s unlisted real estate investments by country as at 31 December 2023.

CHART 17 Annual investments in unlisted real estate. Completed transactions in billions of kroner.

Listed real estate

Investments in listed real estate made up 2.0 percent of the fund and 50.7 percent of our total real estate investments at the end of the year.

These investments were spread across 49 listed companies. The largest percentage stake was 25.2 percent of Shaftesbury Capital. The fund also had holdings above 10 percent in Vonovia and Great Portland Estates. The single largest investment was in Vonovia at 38,759 million kroner.

TABLE 14 Ownership shares in percent for the ten largest listed real estate investments as at 31 December 2023.

|

Company |

Country |

Ownership share1 |

|---|---|---|

|

Shaftesbury Capital PLC |

UK |

25.2 |

|

Vonovia SE |

Germany |

14.9 |

|

Great Portland Estates PLC |

UK |

12.0 |

|

Alexandria Real Estate Equities Inc |

US |

9.4 |

|

Gecina SA |

France |

9.3 |

|

Equity Residential |

US |

9.2 |

|

Grainger PLC |

UK |

9.1 |

|

Vornado Realty Trust |

US |

9.1 |

|

Segro PLC |

UK |

9.1 |

|

Regency Centers Corp |

US |

8.9 |

1Including holdings held as part of equity management.

TABLE 15 The fund's ten largest listed real estate investments. In millions of kroner as at 31 December 2023.

|

Company |

Country |

Holding1 |

|---|---|---|

|

Vonovia SE |

Germany |

38,759 |

|

Simon Property Group Inc |

US |

25,895 |

|

Welltower Inc |

US |

24,793 |

|

Equity Residential |

US |

21,711 |

|

Digital Realty Trust Inc |

US |

21,650 |

|

Alexandria Real Estate Equities Inc |

US |

21,132 |

|

Equinix Inc |

US |

15,798 |

|

Invitation Homes Inc |

US |

13,627 |

|

AvalonBay Communities Inc |

US |

12,850 |

|

Segro PLC |

UK |

12,765 |

1Including holdings held as part of equity management.

Unlisted renewable energy infrastructure

Investments in unlisted renewable energy infrastructure returned 3.7 percent and made up 0.1 percent of the fund at the end of the year.

The return on investments in renewable energy infrastructure comprises the net income from these assets and the change in their value during the period. Expected future power prices, expected future production volumes and the estimated cost of capital impact valuations. The value of the assets decreases over time due to the shorter expected remaining life of the investment.

The positive return in 2023 was due primarily to net income from sales of power. Valuations fell during the year, mainly as a result of a decrease in expected future power prices.

The fund made two new investments in unlisted renewable energy infrastructure during the year. In January, we signed an agreement to acquire a 49 percent interest in a portfolio of solar and onshore wind assets in Spain for 600 million euros, or around 6.4 billion kroner. In March, we signed an agreement to purchase a 16.6 percent stake in He Dreiht, a 960 MW offshore wind project under construction in Germany, for 430 million euros, or around 4.9 billion kroner. This investment was made as part of a consortium that acquired a total of 49.9 percent of the project. The management mandate from the Ministry of Finance sets an upper limit for investments in unlisted renewable energy infrastructure of 2 percent of the fund’s value.

TABLE 16Value of unlisted infrastructure investments in millions of kroner as at 31 December 2023.

|

Value1 |

|

|---|---|

|

Unlisted infrastructure investments |

17,660 |

1Including bank deposits and other receivables.

TABLE 17 Return of unlisted infrastructure investments in percent as at 31 December 2023.

|

Return |

|

|---|---|

|

Unlisted infrastructure investments |

3.68 |

Investment risk

With a large, global fund and a 70 percent allocation to equities, we have to be prepared for considerable fluctuations in the fund’s return and market value.

Risk management and volatility

The risk in the fund is driven largely by the share invested in equities and how much equity prices fluctuate. Movements in interest rates, credit risk premiums and exchange rates will also affect risk, as will changes in the value of investments in unlisted real estate and renewable energy infrastructure. As an investor, we need to have good systems for analysing and managing the risk in the fund.

Measuring the risk to which the fund is exposed is a challenge. To obtain the broadest possible picture, we use a variety of analyses and calculations. We monitor the fund’s concentration risk, expected fluctuations in markets and fund value, factor exposures and liquidity risk. We also perform stress tests and hypothetical scenario analyses on the portfolio. Some investment strategies expose the fund to an increased risk of rare but large and to some extent unpredictable losses. We closely monitor exposure to strategies of this type.

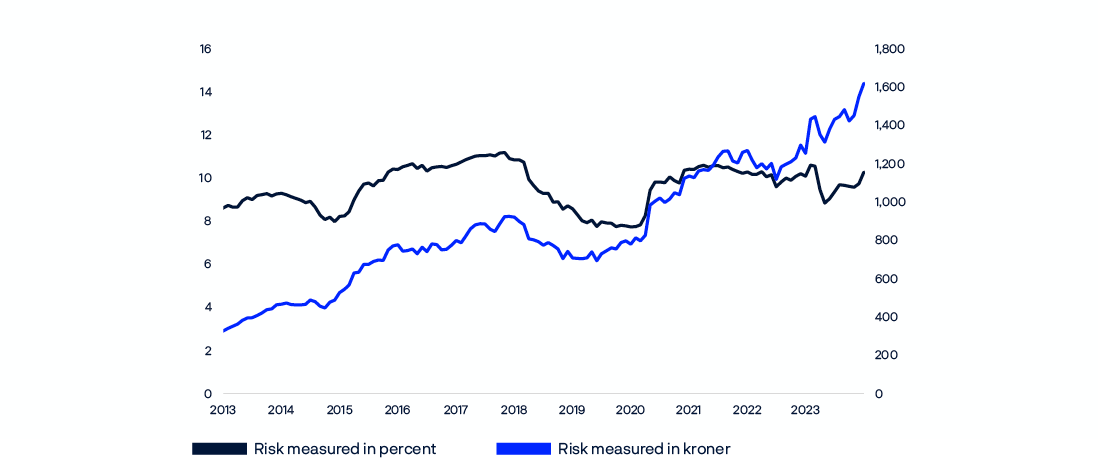

Expected absolute volatility is a measure of how much the annual return on the fund’s investments can normally be expected to fluctuate. This is calculated using standard deviation based on a three-year price history. The fund’s expected absolute volatility was 10.3 percent at the end of 2023, or about 1,620 billion kroner. In other words, the value of the fund can be expected to fluctuate by more than 1,620 billion kroner in one out of three years.

CHART 18 Expected absolute volatility for the fund. Percent (left-hand axis) and billions of kroner (right-hand axis).

Scenario analyses

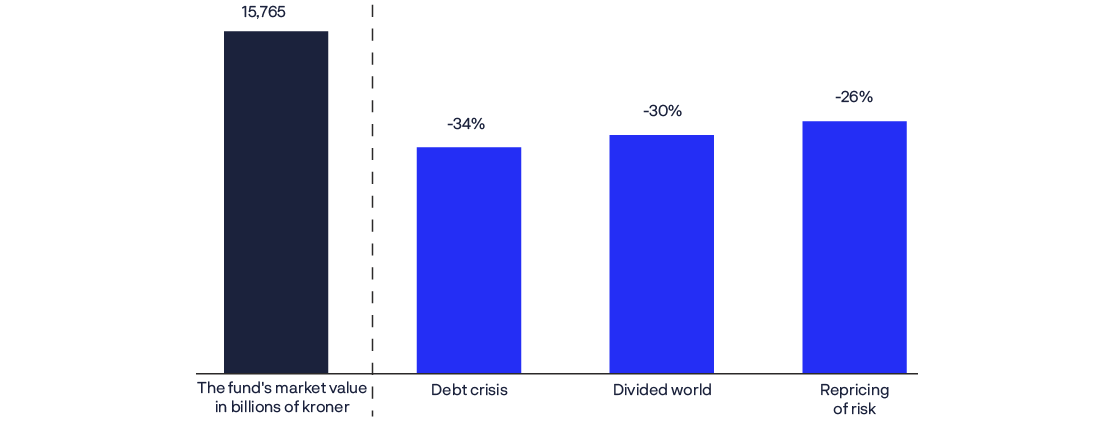

Each year, we publish the results of analyses of a number of hypothetical scenarios. These scenarios may change from year to year to reflect market developments and events that could impact economic performance. Aspects of our scenario analyses from 2022 remain relevant, such as the consequences of a regional military conflict. The risk of this scenario is still present, but a lasting economic conflict could also lead to substantial losses for the fund. We have therefore included such a scenario in our latest report.

In 2023, we analysed three potential scenarios that could have a significant adverse impact on the fund’s value over time:

Debt crisis

High real interest rates and high public and private debt trigger a deep and long recession in both developed and emerging markets. This could hit the real estate sector particularly hard. High levels of debt limit governments’ ability to combat the recession.

Divided world

Tensions between countries increase, resulting in a protracted geoeconomic conflict. A splintering into two economic blocs leads to a persistent decrease in growth and higher inflation. Trade and capital flows between the two blocs decline permanently. Competition between the blocs means that investment in strategic sectors grows.

Repricing of risk

Equity risk premiums – or the compensation that investors receive for taking risk in the stock market – appears to be at historically low levels. Inflation does not come down, and central banks have to manage a difficult trade-off between stimulating economic growth and fighting inflation.

We analysed how these scenarios might affect the fund’s value and calculated potential losses over a period of up to five years. The equity market is vulnerable in all these scenarios. The sharp rise in real interest rates over the past two years means that the risk of losses on fixed-income investments has fallen.

A full report on this stress testing can be found on our website: www.nbim.no.

CHART 19 Estimated market value of the fund under each scenario and potential losses in percent.

Weaker return than the benchmark index

We aim to leverage the fund’s long-term investment horizon and considerable size to generate a high return with acceptable risk. In 2023, the fund’s return was 0.18 percentage point lower than the return on the benchmark index.

The return on the fund’s investments is measured against the return on the fund’s benchmark index from the Ministry of Finance, which is made up of global equity and bond indices. The equity portion of the benchmark index is based on the FTSE Global All Cap index and comprised 9,191 listed companies at the end of the year. The bond portion of the benchmark index is based on indices from Bloomberg Indices and comprised 17,565 bonds from 2,398 issuers.

At the end of 2023, the fund was invested in 8,859 listed companies and 6,378 bonds from 1,390 issuers. The fund also had investments in 897 unlisted properties and four investments in unlisted renewable energy infrastructure. To make all these investments in a way that contributes to the objective of the highest possible return after costs, we delegate the responsibility for individual investments to our portfolio managers through individual investment mandates. These mandates are awarded within the fund’s three main strategies: market exposure, security selection and fund allocation. A delegated mandate structure helps us build deep insight into selected market segments and companies. This insight puts us in a better position to be a responsible investor. At the end of 2023, we had 261 individual equity and bond mandates, of which 111 were assigned to external equity managers. This approach ensures precise management and control of risk, performance measurement, costs and incentives for each investment mandate.

The fund’s investments in real estate and unlisted renewable energy infrastructure are not part of the benchmark index from the Ministry. We sell equities and bonds in the benchmark index to fund investments in real estate and unlisted infrastructure. Which equities and bonds are sold depends on the country and currency in which the investment is made. The relative return for equity management and bond management is measured against the benchmark index adjusted for the equities and bonds sold to fund investments in real estate and unlisted renewable energy infrastructure. The return on real estate and infrastructure investments is measured against the equities and bonds sold to fund them.

The fund’s relative return

In 2023, the fund’s return was 0.18 percentage point lower than the return on the benchmark index1. The fund has outperformed the benchmark index by 0.28 percentage point annually since 1998, 0.22 percentage point over the past decade, and 0.42 percentage point over the past five years.

TABLE 18 Relative return in 2023.

|

Percentage points |

|

|---|---|

|

Fund |

-0.18 |

|

Equity investments |

0.50 |

|

Fixed-income investments |

0.48 |

CHART 20 The fund’s annual relative return and accumulated annualised relative return in percentage points. Calculations based on aggregated equity and fixed-income investments until end of 2016.

Equity management

Equity management is measured against the equity portion of the benchmark index, adjusted for sales of equities to fund investments in real estate and renewable energy infrastructure. The return on equity management was 0.38 percentage point higher than on this adjusted benchmark in 2023 and made a positive contribution of 0.25 percentage point to the fund’s total relative return. Investments in the financial and technology sectors contributed most to the relative return, while investments in consumer goods and energy made negative contributions. Broken down by country, investments in the US, Switzerland and the UAE contributed most to the relative return, while investments in Italy and Singapore made negative contributions.

Equity management has outperformed the benchmark index by 0.48 percentage point annually since 1999, 0.32 percentage point over the past decade, and 0.64 percentage point over the past five years.

Fixed-income management

Fixed-income management is measured against the bond portion of the benchmark index, adjusted for sales of bonds to fund investments in real estate and renewable energy infrastructure. The return on fixed-income management was 0.51 percentage point higher than on this adjusted benchmark in 2023 and contributed 0.14 percentage point to the fund’s relative return. Government bonds from Europe and emerging markets made the most positive contributions, while investments in corporate bonds made a negative contribution. Fixed-income management also had a lower duration than the benchmark in a year when interest rates rose, resulting in a positive contribution to the relative return.

Fixed-income management has outperformed the benchmark index by 0.24 percentage point annually since 1998, 0.29 percentage point over the past decade, and 0.64 percentage point over the past five years.

Real estate

We invest in real estate to improve the fund’s risk/return profile. The fund’s overall strategy for real estate covers both unlisted and listed real estate investments. The relative return for real estate management is the difference between the return on the fund’s total real estate investments and the return on the bonds and equities sold to buy them. Real estate management contributed -0.47 percentage point to the fund’s relative return in 2023. Unlisted real estate investments made a contribution of -0.58 percentage point. All markets had negative returns in 2023 other than Japan where there was a marginal positive return. The fund’s properties in the US made the greatest negative contribution, followed by those in France and Germany. Office properties in particular underperformed, but logistics and retail also made negative contributions. Listed real estate investments made a positive contribution to the relative return of 0.11 percentage point. Broken down by country, the US and Germany made the most positive contributions.

We report unlisted real estate returns quarterly and annually, but it is important to assess the real estate strategy over a longer period. From the fund’s first unlisted real estate investment in 2010 through to the end of 2016, the annual return on unlisted real estate investments was 5.98 percent. During this period, real estate investments were funded by selling bonds. The annual return on bond investments in the same period was 4.37 percent. The annual return on the real estate portfolio from 2017 to 2023 was 3.0 percent. During this period, unlisted real estate was funded through sales of equities as well as bonds. The annual return on this funding was 3.7 percent.

Unlisted renewable energy infrastructure

We invest in unlisted renewable energy infrastructure to improve the fund’s risk/return profile. The fund’s strategy focuses on building up a portfolio of large-scale high-quality wind and solar power generation assets. The relative return for renewable energy infrastructure is the difference between the return on the fund’s total investments in these assets and the return on the bonds sold to buy them. The fund’s investments in renewable energy infrastructure returned 1.2 percent in 2023 measured in euros. From inception, this strategy has produced an annual return of 6.7 percent measured in euros.

TABLE 19 Relative return on the fund's asset management in percentage points.

|

Year |

Fund1 |

Equity management2 |

Fixed-income management2 |

Real estate management2 |

Infrastructure management |

|---|---|---|---|---|---|

|

2023 |

-0.18 |

0.38 |

0.51 |

-10.51 |

-5.67 |

|

2022 |

0.87 |

0.52 |

1.68 |

0.22 |

25.09 |

|

20213 |

0.75 |

0.78 |

-0.04 |

7.36 |

8.04 |

|

2020 |

0.27 |

0.98 |

0.76 |

-13.81 |

|

|

2019 |

0.23 |

0.51 |

0.11 |

-3.89 |

|

|

2018 |

-0.30 |

-0.69 |

-0.01 |

5.49 |

|

|

2017 |

0.70 |

0.79 |

0.39 |

0.70 |

|

|

2016 |

0.15 |

0.15 |

0.16 |

||

|

2015 |

0.45 |

0.83 |

-0.24 |

||

|

2014 |

-0.77 |

-0.82 |

-0.70 |

||

|

2013 |

0.99 |

1.28 |

0.25 |

||

|

2012 |

0.21 |

0.52 |

-0.29 |

||

|

2011 |

-0.13 |

-0.48 |

0.52 |

||

|

2010 |

1.06 |

0.73 |

1.53 |

||

|

2009 |

4.13 |

1.86 |

7.36 |

||

|

2008 |

-3.37 |

-1.15 |

-6.60 |

||

|

2007 |

-0.24 |

1.15 |

-1.29 |

||

|

2006 |

0.14 |

-0.09 |

0.25 |

||

|

2005 |

1.06 |

2.16 |

0.36 |

||

|

2004 |

0.54 |

0.79 |

0.37 |

||

|

2003 |

0.55 |

0.51 |

0.48 |

||

|

2002 |

0.30 |

0.07 |

0.49 |

||

|

2001 |

0.15 |

0.06 |

0.08 |

||

|

2000 |

0.27 |

0.49 |

0.07 |

||

|

1999 |

1.23 |

3.49 |

0.01 |

||

|

1998 |

0.18 |

0.21 |

1Includes real estate management from 2017. The fund's relative return prior to 2017 is calculated on equity and fixed-income management only.

2Measured against actual funding from 2017. The relative return on equity and fixed-income management before 2017 is measured against the respective Ministry of Finance asset class indices.

3The relative return on the fund and fixed-income management for 2021 have been adjusted by 0.01 percentage point as a result of an update of the return on the benchmark index.

Investment strategies

We employ a range of investment strategies in our management of the fund. They are grouped into three main categories: market exposure, security selection and fund allocation. These strategies are pursued across equity, fixed-income and real asset management.

Market exposure strategies consist of positioning and securities lending, and contributed 0.16 percentage point to the fund’s relative return in 2023. Positioning is about implementing market exposures in ways that increase investment returns and reduce transaction costs for the fund. The strategy aims to exploit relative valuations across instruments and issuers, the pricing effects of corporate and market events, and positioning in relation to developments in fixed-income markets, including interest rate levels, inflation, exchange rates and interest rate differentials between countries. Equity positioning contributed 0.02 percentage point to the relative return for 2023, the main contributors being Chinese stocks. Investments in the US and developed markets in Asia made negative contributions. Bond positioning contributed 0.10 percentage point to the fund’s relative return, with positive contributions from all regions. Securities lending contributed 0.04 percentage point to the fund’s relative return, most of which came from loans of equities.

Security selection strategies use deep insights into the fund’s largest investments provided by company analysis to enhance returns and support the fund’s work as a responsible and active owner. Positions under these strategies contributed 0.18 percentage point to the fund’s relative return in 2023. Internal equity selection contributed 0.10 percentage point, with investments in financials and technology making particularly positive contributions, and investments in consumer durables the most negative contribution. External equity selection contributed 0.11 percentage point to the relative return, with a positive contribution from emerging markets in every region, and a negative contribution from developed markets.

When it comes to fixed-income management, security selection focuses on corporate bonds. This strategy contributed -0.03 percentage point to the fund’s relative return, with credit positioning making a positive contribution, and issuer selection a negative contribution.

Fund allocation consists of a number of strategies that aim to improve the trade-off between return and risk in the fund. These strategies contributed -0.53 percentage point to the fund’s relative return in 2023.

Investments in real estate and renewable energy infrastructure are reported under fund allocation in our strategy reporting. Investments in real estate contributed -0.47 percentage point to the fund’s relative return in 2023, and investments in renewable energy infrastructure -0.01 percentage point.

In 2023, the fund was underweight in equities and overweight in bonds, and overweight in emerging-market bonds. The bond portfolio also had a lower duration than the benchmark index throughout the year. Taken together, allocation decisions of this kind made a contribution of -0.05 percentage point to the relative return.

TABLE 20 Contributions to the fund's relative return from investment strategies in 2023. In percentage points.

|

Equity management |

Fixed-income management |

Real assets management |

Allocation |

Total |

|

|---|---|---|---|---|---|

|

Market exposure |

0.06 |

0.10 |

0.00 |

0.16 |

|

|

Asset positioning |

0.02 |

0.10 |

0.00 |

0.12 |

|

|

Securities lending |

0.03 |

0.01 |

0.04 |

||

|

Security selection |

0.21 |

-0.03 |

0.18 |

||

|

Internal security selection |

0.10 |

-0.03 |

0.07 |

||

|

External security selection |

0.11 |

0.11 |

|||

|

Fund allocation |

-0.02 |

0.07 |

-0.48 |

-0.10 |

-0.53 |

|

Real estate |

-0.47 |

-0.47 |

|||

|

Unlisted real estate |

-0.58 |

-0.58 |

|||

|

Listed real estate |

0.11 |

0.11 |

|||

|

Renewable energy infrastructure |

-0.01 |

-0.01 |

|||

|

Allocation |

-0.02 |

0.07 |

-0.10 |

-0.05 |

|

|

Total |

0.25 |

0.14 |

-0.48 |

-0.10 |

-0.18 |

TABLE 21 Contributions to the fund's relative return from investment strategies annualised for 2013–2023. In percentage points.

|

Equity management |

Fixed-income management |

Real assets management |

Allocation |

Total |

|

|---|---|---|---|---|---|

|

Market exposure1 |

0.11 |

0.07 |

0.00 |

0.18 |

|

|

Asset positioning |

0.07 |

0.07 |

0.00 |

0.14 |

|

|

Securities lending |

0.04 |

0.01 |

0.05 |

||

|

Security selection |

0.16 |

0.01 |

0.17 |

||

|

Internal security selection |

0.07 |

0.01 |

0.08 |

||

|

External security selection |

0.09 |

0.09 |

|||

|

Fund allocation |

0.00 |

-0.01 |

-0.06 |

0.00 |

-0.06 |

|

Real estate |

-0.06 |

-0.06 |

|||

|

Unlisted real estate |

0.00 |

0.00 |

|||

|

Listed real estate |

-0.05 |

-0.05 |

|||

|

Renewable energy infrastructure |

0.00 |

0.00 |

|||

|

Allocation2,3 |

0.00 |

-0.01 |

0.00 |

0.00 |

-0.01 |

|

Total |

0.26 |

0.07 |

-0.06 |

0.01 |

0.29 |

1 Market exposure includes -0.01 percentage point from the systematic factors strategy which was ended in the second quarter of 2020.

2Regulations for Environmental related mandates for equities and fixed income were changed by the Ministry of Finance during 2022. The historic performance impact from Environmental related mandates until 2022 is included under Allocations.

3Specific allocation to Systematic factors was ended in 2022. The historic performance impact from Systematic factors is included under Allocations.

Risk relative to the benchmark index

The fund is invested differently to its benchmark index along various dimensions, including asset classes, currencies, sectors, countries, regions, individual stocks and individual bond issuers.

At the end of 2023, the equity portfolio was overweight in high-volatility stocks and a number of growth segments, including stocks with low dividend yields. The fixed-income portfolio had less exposure to corporate bonds than the benchmark index, but greater exposure to bonds from emerging markets and government-related bonds. The fund also had 301 billion kroner invested in unlisted real estate and an allocation to listed real estate investments of 309 billion kroner at the end of 2023. Real estate investments were among the fund’s largest relative exposures at year-end.

The Ministry of Finance and Norges Bank’s Executive Board have set limits for how far the fund’s investments may deviate from the benchmark index.

One of these limits is for expected relative volatility, or tracking error, and puts a ceiling on how much the return on the fund’s investments can be expected to deviate from the return on the benchmark index. The management mandate requires all of the fund’s investments to be included in the calculation of expected relative volatility and measured against the fund’s benchmark index, which consists solely of global equity and bond indices. The fund is to aim for expected relative volatility of no more than 1.25 percentage points. The actual level at the end of the year was 0.34 percentage point, down from 0.39 percentage point at the end of 2022. The decrease was due mainly to a lower expected relative volatility for real estate investments.

The fund invests in real estate to create a more diversified portfolio. We expect real estate investments to have a different return profile to equities and bonds in both the short and the longer term. The relative risk that this entails will impact on calculations of the fund’s expected relative volatility. As daily pricing is not available for our unlisted real estate investments, we use a model from MSCI to calculate the relative risk for these investments.

Norges Bank’s Executive Board has also set a limit for expected shortfall for the relative return between the fund and the benchmark index. The fund is to be managed in such a way that the expected negative relative return in extreme situations does not exceed 3.75 percentage points. The actual figure was 1.08 percentage points at the end of the year, down from 1.22 percentage points at the end of 2022.

TABLE 22 Key figures for the fund's risk and exposure.

|

Limits set by the Ministry of Finance |

31.12.2023 |

|

|---|---|---|

|

Allocation |

Equity portfolio 60–80 percent of fund's market value1 |

70.8 |

|

Unlisted real estate no more than 7 percent of the fund's market value |

1.9 |

|

|

Fixed-income portfolio 20–40 percent of fund's market value1 |

28.6 |

|

|

Unlisted renewable energy infrastructure no more than 2 percent of the fund's market value |

0.1 |

|

|

Market risk |

1.25 percentage points expected relative volatility for the fund's investments |

0.3 |

|

Credit risk |

Maximum 5 percent of fixed-income investments may be rated below BBB- |

1.1 |

|

Emerging markets |

Maximum 5 percent of fixed-income investments may be in emerging markets |

2.7 |

|

Ownership |

Maximum 10 percent of voting shares in a listed company in the equity portfolio2 |

9.6 |

1Derivatives are represented with their underlying economic exposure.

2Investments in listed and unlisted real estate companies are exempt from this restriction.

CHART 21 Expected relative volatility of the fund in basis points.

TABLE 23Expected relative volatility of investment strategies as at 31 December 2023. Each strategy measured stand-alone with the other strategies positioned in line with the benchmarks. All numbers measured at fund level in basis points.

|

Equity management |

Fixed-income management |

Real assets management |

Allocation |

Total |

|

|---|---|---|---|---|---|

|

Market exposure |

4 |

2 |

0 |

5 |

|

|

Asset positioning |

4 |

2 |

0 |

5 |

|

|

Security selection |

16 |

2 |

16 |

||

|

Internal security selection |

12 |

2 |

12 |

||

|

External security selection |

7 |

7 |

|||

|

Fund allocation |

6 |

4 |

34 |

9 |

34 |

|

Real estate |

34 |

34 |

|||

|

Unlisted real estate |

18 |

18 |

|||

|

Listed real estate |

23 |

23 |

|||

|

Renewable energy infrastructure |

4 |

4 |

|||

|

Allocation |

6 |

4 |

9 |

13 |

|

|

Total |

17 |

6 |

34 |

9 |

34 |

1From 2019 to 2022, the fund recognised a provision for future tax obligations relating to capital gains in India which was not included in the benchmark index. From 2023 onwards, this provision is not included in the fund’s market value. This change affected the relative return for 2023 by 4,488 million kroner. Viewed over the period from 2019 to 2023, however, these provisions had no impact on the relative return.

Responsible investment report

The fund’s work on responsible investment is presented in a separate report available on our website: www.nbim.no.

Our people are the heart of our business

Our people are our most important asset. We aim to attract, develop and retain leading talent. We aim to ensure that everyone can work efficiently and innovatively and has the skills to take on new challenges.

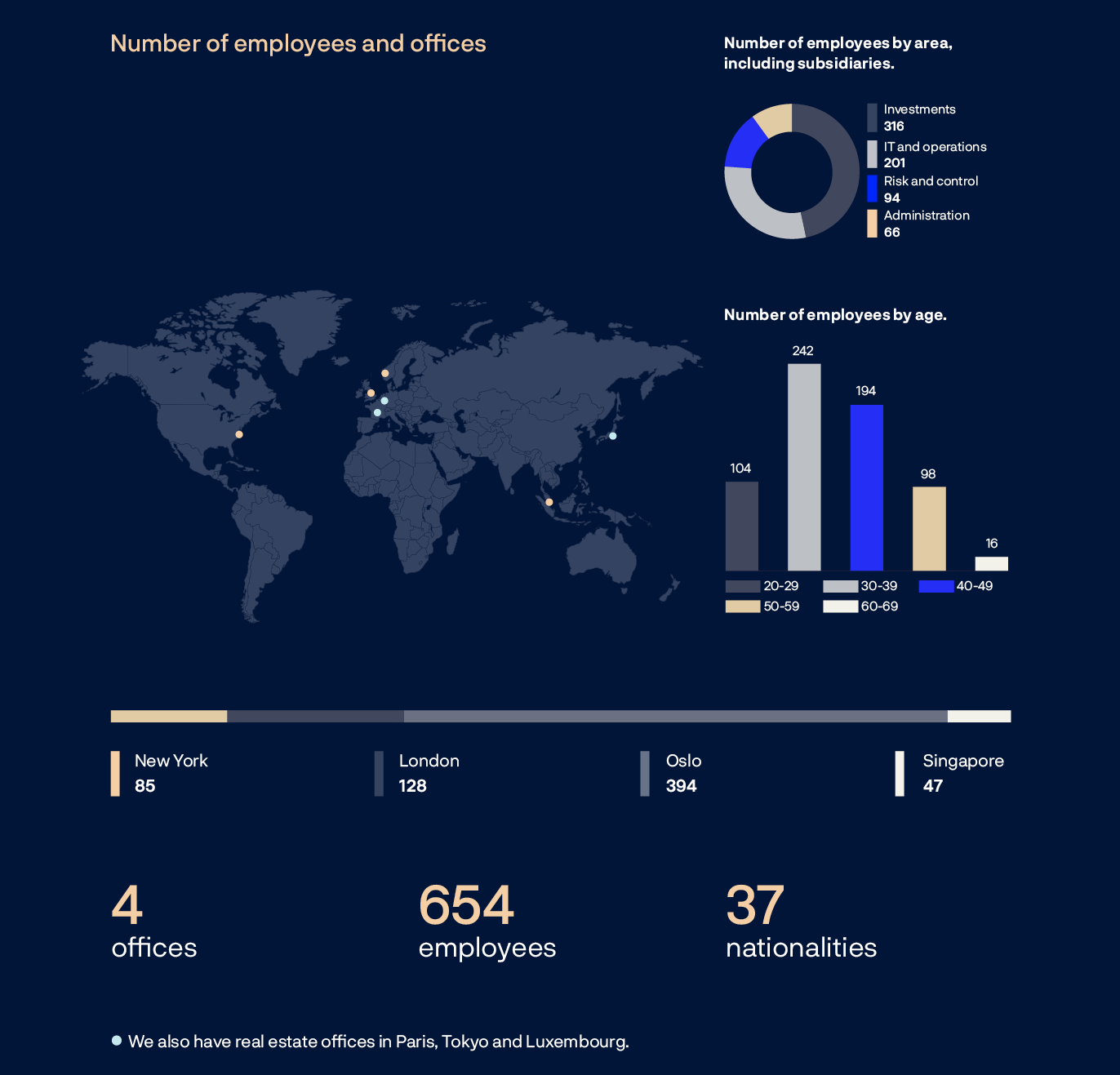

We are a global investment organisation. At the end of 2023, we had 654 employees across our offices in Oslo, London, New York and Singapore. We also have real estate offices in Paris, Luxembourg and Tokyo. Close collaboration across these offices is essential for achieving the fund’s objective of the highest possible return.

We decided in autumn 2023 to close our representative office in Shanghai. The Singapore office has been built up gradually to take care of all operational functions, including investments in China.

Learning and development opportunities

We believe in lifelong learning and give employees the chance to build relevant skills throughout their careers. We work systematically on developing managers and employees, offering a variety of learning and development opportunities.

In 2023, we launched our improved performance management process THRIVE where employees reflect on their performance and set targets for the year ahead. The aim is to promote professional development and increase interaction between managers, teams and individuals. We have clear expectations for all managers and employees.

We arrange regular physical and digital meet-ups for managers, and launched an induction programme for all new managers in 2023. Giving and receiving feedback is one of our core competencies. We believe that this brings personal and professional development at all career stages. Each year, managers carry out a 360 review where they gather feedback from their colleagues to help them develop further in their role.

We launched our own Investment Academy during the year to boost investment skills, value chain understanding and collaboration across the organisation through sessions with internal experts. In collaboration with Rystad Energy Institute, we arranged a lecture series on the energy transition and renewable energy for the entire organisation. For the first time, we arranged hackathons at all our offices. The aim was to explore the use of AI and understand how this technology can help us be more efficient.

We launched our own learning platform during the year with digital courses tailored to our organisation. We also offer more than 7,000 courses from leading universities and organisations.

Our 2023 people survey showed strong engagement among our employees. They are happy with their employer, they feel that their work is meaningful, and they are proud to work for Norges Bank Investment Management across gender, age and nationality.

Information and recruitment

We are keen to give young people a better understanding of the world of finance. In 2023, we gave 19 guest lectures at universities in Norway and abroad. The aim was to give students an insight into investment management in practice, increase knowledge about the fund and share our expertise with a younger target group so that more apply to work for us.

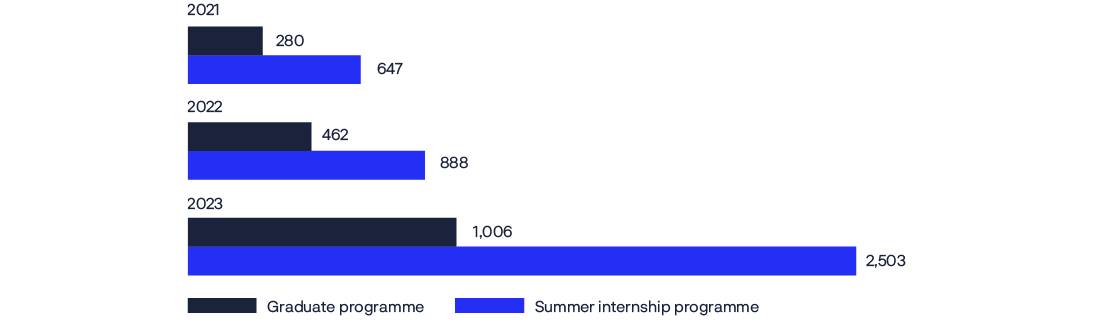

We work systematically to recruit the best candidates both in Norway and internationally. We seek talented individuals with varied skills and backgrounds. We saw a significant increase in the number of applicants for our vacancies from 2022 to 2023, including record-high applications for our graduate and summer internship programmes.

CHART 22 Number of applications for our graduate and summer internship programmes.

Diversity and inclusion

We aim to be an inclusive organisation with a diversity of mindsets, ethnicities, age groups, academic backgrounds and life experience. This brings a broader perspective, increases creativity and leads to better decisions.

We are working actively to increase the share of women in the organisation as a whole and in management positions. Norges Bank signed the Women in Finance Charter in 2021 and hosted the charter’s second status report in 2023. Our obligations under the charter’s four principles can be found on our website. We also have our own networks for female employees.

Our continuous efforts to increase the share of women have yielded positive results, partly through better retention of female employees.

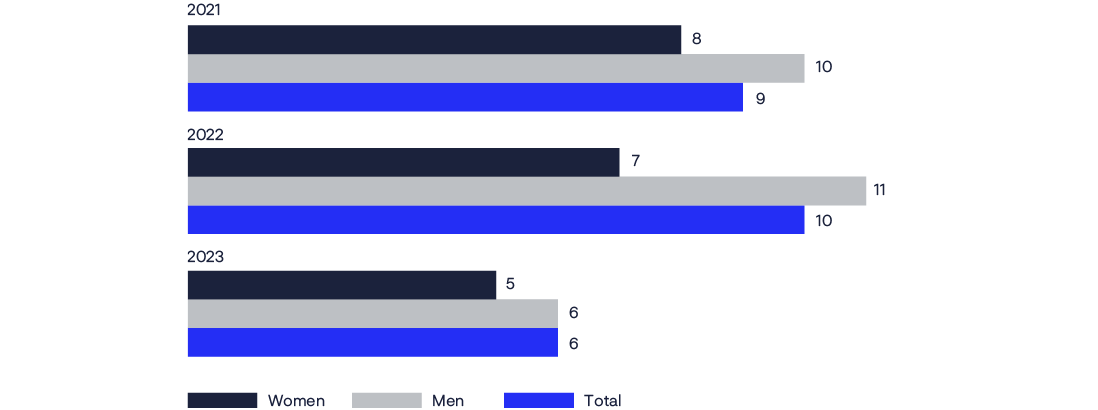

CHART 23 Employees who ended their employment, by gender in percent.

To ensure that we are consistent and fair in our approach to employees’ progression, promotion and remuneration, different areas of the organisation have their own career ladders. Each ladder can have up to five different grades with consistent job titles. Each grade reflects the expectations associated with the role that are to be met regardless of which area the employee works in. For example, a portfolio manager in Market Strategies, a senior adviser in Risk Management and a technical expert in Technology & Operations are considered to be the same grade in terms of capability, responsibility and behaviour.

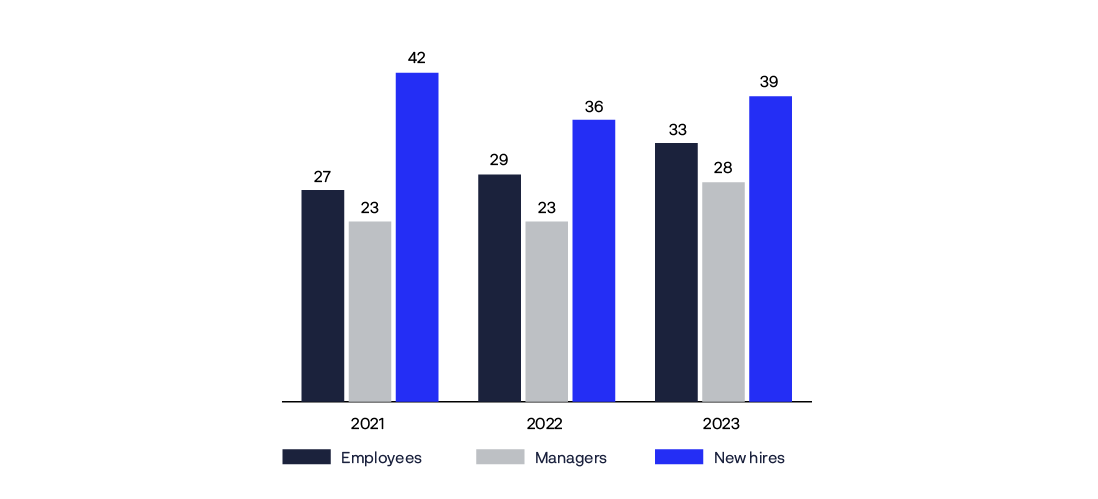

CHART 24 Share of employees, managers and new hires who are women, in percent.

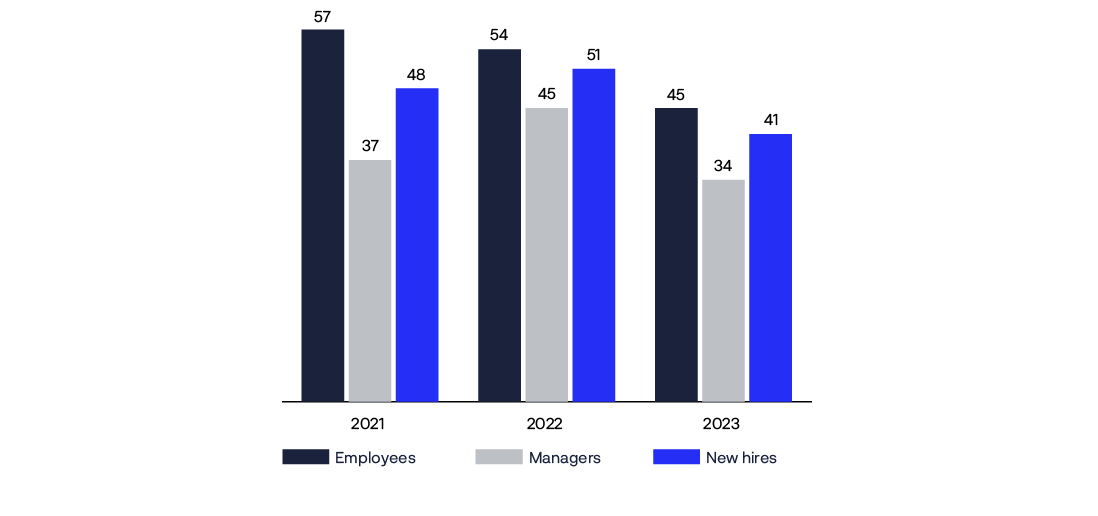

CHART 25 Share of employees, managers and new hires who are non-Norwegian, in percent.

TABLE 24 Gender balance by grade and office as at 31 December 2023. In percent.

|

Grade |

Oslo |

London |

New York |

Singapore |

||||

|---|---|---|---|---|---|---|---|---|

|

Share of employees |

Share of employees |

Share of employees |

Share of employees |

|||||

|

Men |

Women |

Men |

Women |

Men |

Women |

Men |

Women |

|

|

Global Head |

91 |

9 |

80 |

20 |

100 |

0 |

||

|

Head |

63 |

38 |

69 |

31 |

90 |

10 |

100 |

0 |

|

Level 5 |

100 |

0 |

100 |

0 |

60 |

40 |

||

|

Level 4 |

79 |

21 |

76 |

24 |

81 |

19 |

63 |

38 |

|

Level 3 |

63 |

37 |

56 |

44 |

67 |

33 |

78 |

22 |

|

Level 2 |

67 |

33 |

35 |

65 |

80 |

20 |

57 |

43 |

|

Level 1 |

53 |

47 |

40 |

60 |

100 |

0 |

50 |

50 |

Remuneration system

Norges Bank’s Executive Board sets limits for our remuneration system and monitors its implementation. Pay levels are to be competitive but generally not market-leading. Salaries are set individually and reflect the position’s responsibilities and the employee’s skills, experience and achievements. Total remuneration paid includes fixed salary and any performance-based pay and overtime payments.

In keeping with management mandate from the Ministry of Finance, the remuneration system complies with the requirements of the regulations issued under the Securities Funds Act with necessary adjustments. The Executive Board’s Remuneration Committee is to contribute to thorough and independent consideration of matters concerning Norges Bank’s remuneration arrangements. Norges Bank’s Internal Audit unit also issues an independent statement on compliance with rules and guidelines on remuneration. The review in 2023 confirmed that the remuneration system was operated in line with applicable rules in 2022. There were no significant changes to the remuneration system during the year.

Members of the leader group receive only a fixed salary. The CEO’s salary and pay bands for other members of the leader group are set by the Executive Board.

TABLE 25Fixed salary and other key information for senior management in 2023.

|

Position |

Name |

Gender |

Investment area |

Age |

Tenure in Norges Bank Investment Management |

Annual fixed salary in kroner |

|---|---|---|---|---|---|---|

|

Chief Human Resources Officer |

Aass, Ada Magnæs1 |

Woman |

44 years |

9 years |

2,300,000 |

|

|

Co-Chief Investment Officer Equities |

Balthasar, Daniel2 |

Man |

Investment area |

47 years |

17 years |

12,068,000 |

|

Chief Technology and Operating Officer |

Bryne, Birgitte |

Woman |

51 years |

8 years |

4,010,000 |

|

|

Co-Chief Investment Officer Equities |

Furtado Reis, Pedro2 |

Man |

Investment area |

48 years |

12 years |

12,068,000 |

|

Deputy Chief Executive Officer/Chief of Staff |

Grande, Trond |

Man |

53 years |

16 years |

5,225,000 |

|

|

Chief Investment Officer Real Assets |

Holstad, Mie Caroline |

Woman |

Investment area |

41 years |

13 years |

3,415,000 |

|

Chief Risk Officer |

Huse, Dag |

Man |

57 years |

20 years |

4,860,000 |

|

|

Chief Governance and Compliance Officer |

Ihenacho, Carine Smith2 |

Woman |

61 years |

6 years |

5,859,000 |

|

|

Co-Chief Investment Officer Asset Strategies |

Norberg, Malin1 |

Woman |

Investment area |

39 years |

14 years |

4,300,000 |

|

Co-Chief Investment Officer Asset Strategies |

Nygård, Geir Øivind |

Man |

Investment area |

43 years |

16 years |

4,750,000 |

|

Chief Communications and External Relations Officer |

Skaar, Marthe1 |

Woman |

40 years |

10 years |

1,950,000 |

|

|

Chief Executive Officer |

Tangen, Nicolai |

Man |

57 years |

3 years |

7,160,000 |

1 Member of Norges Bank Investment Management's leader group from 1 April 2023.

2 Receives a salary in pounds sterling. The amount shown includes the currency effect when translating into kroner.

TABLE 26 Remuneration of senior management in 2023. In kroner.

|

Position |

Name |

Paid salary |

Performance-based pay |

Value of other benefits4 |

Pension benefit earned |

Employee loan |

|---|---|---|---|---|---|---|

|

Chief Human Resources Officer |

Aass, Ada Magnæs1 |

1,711,965 |

7,261 |

274,828 |

||

|

Co-Chief Investment Officer Equities |

Balthasar, Daniel2,3 |

12,030,505 |

3,585,764 |

172,149 |

1,203,051 |

|

|

Chief Technology and Operating Officer |

Bryne, Birgitte |

3,964,247 |

16,555 |

437,723 |

||

|

Co-Chief Investment Officer Equities |

Furtado Reis, Pedro2,3 |

12,030,505 |

3,475,348 |

168,777 |

1,203,051 |

|

|

Deputy Chief Executive Officer/Chief of Staff |

Grande, Trond |

5,199,029 |

9,156 |

409,556 |

||

|

Chief Investment Officer Real Assets |

Holstad, Mie Caroline |

3,380,174 |

12,341 |

346,309 |

||

|

Chief Risk Officer |

Huse, Dag |

4,842,036 |

9,156 |

668,627 |

||

|

Chief Governance and Compliance Officer |

Ihenacho, Carine Smith3 |

5,800,948 |

155,701 |

580,095 |

||

|