1. Introduction

Navigating a complex world

2025 has been marked by uncertainty. Wars continue, geopolitical tensions have deepened, and the policy landscape are shifting. Rapid technological change and the physical effects of climate change are increasingly visible in the global economy.

The fund is a long-term global investor in equities, fixed income, real estate and renewable energy infrastructure. Our mandate is to generate financial returns for current and future generations of Norwegians. This requires that our investments achieve sustainable value over time.

Our new strategy focuses on increasing the fund’s return and resilience through world-leading responsible investment. It is grounded in foundations built over time and adapts to a more demanding and unpredictable environment in a changing world. The conflict in Gaza and the discussions about the fund’s ethical framework and investments in Israel demonstrated in 2025 how complex and challenging this can be in practice. While the fund’s ethical framework is under revision, we continue our responsible investment work, strengthening the link between ownership and investment decisions and focusing on what is financially material.

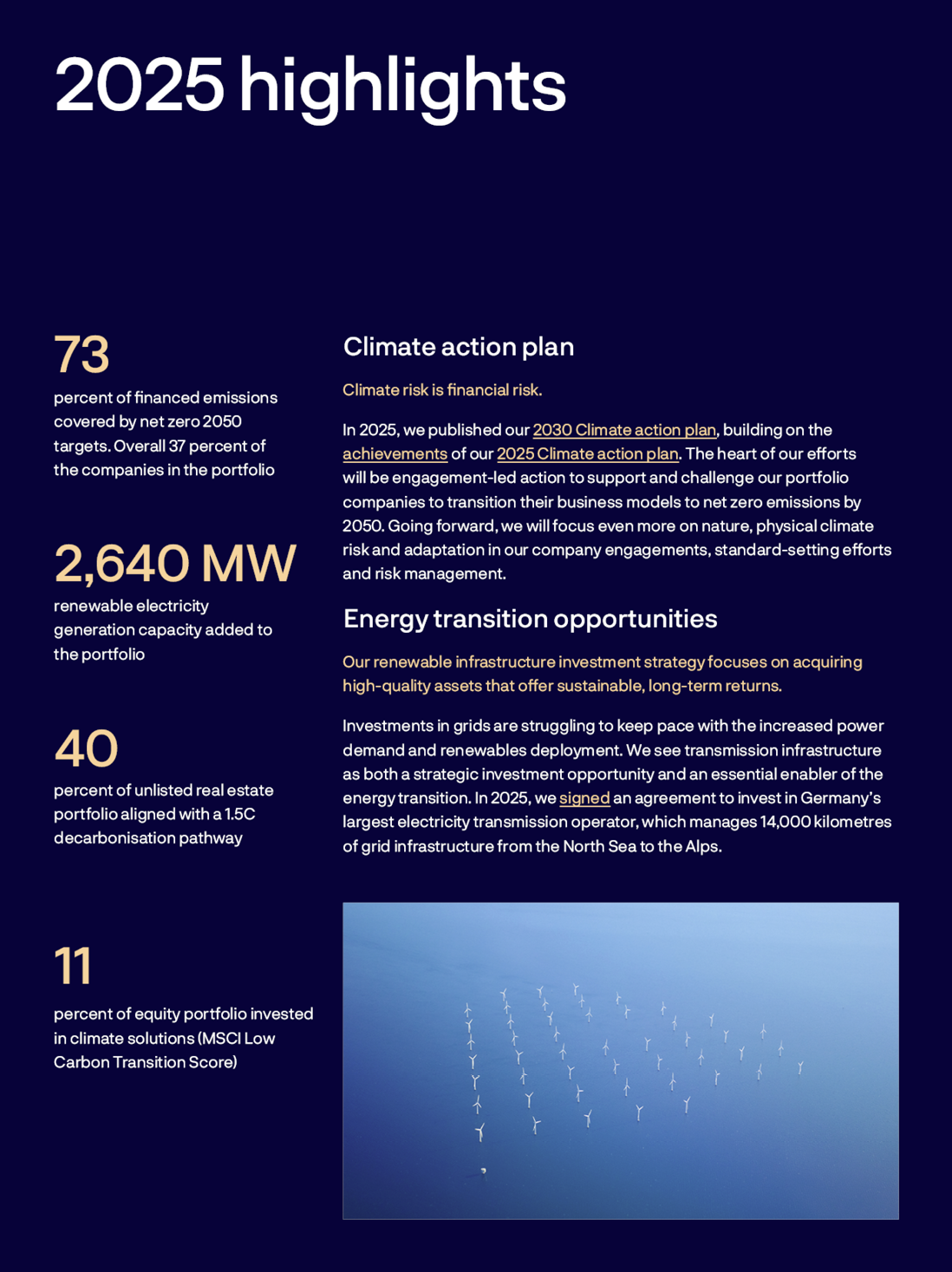

We aim to be a leader in managing the financial risks and opportunities arising from climate change. We have worked with climate risk in nearly twenty years. In 2025, we launched our updated Climate action plan towards 2030. It sets out actions and milestones for how we will engage with companies on climate and nature risk, the energy transition and related investment opportunities.

Artificial intelligence is changing how we work as an investor. New tools help us analyse risk, assess investments and evaluate our company engagement. It improves decision-making across our large and diverse portfolio.

Responsible investment reflects that sustainability and governance are inseparable from financial performance. Companies that manage risk well, adapt their business models and maintain sound governance are better placed to create long-term value.

The world will remain complex and uncertain. The fund is built to last for generations, and we invest with the same horizon. What matters is beyond the next year’s returns, but whether the companies we own can navigate this complexity in the long run.

Oslo, 26 February 2026

Nicolai Tangen

Chief Executive Officer Norges Bank Investment Management

Opportunities and limitations for a responsible investor

As a responsible investor, we face both opportunities and limitations. Our size and transparency give us a voice in the market, but this voice is grounded in our role as a minority shareholder in companies.

We have one mission – to generate long-term financial returns. Sustainable business practices and sound governance are essential for lasting value creation, and we depend on companies and boards making good decisions. Being a long-term investor, we have the patience many other lack. This allows us to withstand short-term volatility and pressures and focus on what matters for sustainable value creation.

Our size and permanence of capital provide good access to companies. When we discuss material issues with them - from climate risk to effective boards - companies listen. Our transparency extends our impact beyond our ownership stake. When we publish our voting decisions or explain our reasoning, others take notice.

Despite our size, we remain a minority shareholder in companies operating under diverse regulatory frameworks. We don’t micromanage companies’ boards or dictate operational decisions but communicate our views through a constructive dialogue. We believe this contributes to effective ownership over time.

The world is becoming increasingly complex. There are no simple solutions to challenges like climate change, technological disruption or shifting geopolitics. In 2025, markets were further polarised, with shareholder proposals often pulling companies in opposing directions. We are mindful of the difficult environment many companies operate in and navigate this complexity carefully.

Our ownership results depend on us being a credible actor in the global capital markets. Creating long-term sustainable value requires both patience and consistency. It requires policies facilitating efficient capital markets, providing predictability for investors and companies. It requires clear priorities and an honest recognition of what we can achieve and where our role as a responsible investor ends.

Oslo, 26 February 2026

Carine Smith Ihenacho

Chief Governance and Compliance Officer

How we work

We manage the fund according to a mandate from the Norwegian Ministry of Finance. The objective for the management of the fund is the highest possible return with acceptable risk.

Within this objective, our mandate requires us to manage the fund with high transparency and in line with internationally recognised principles and standards for responsible investing. The mandate also establishes that responsible investment activities shall be based on the long-term goal that the companies in the investment portfolio have activities that are compatible with global net zero emissions, in accordance with the Paris Agreement.

The fund’s long-term return is dependent on sustainable economic, environmental and social development, as well as well-functioning, legitimate and efficient markets. Through responsible investment, we seek to improve the financial performance of our investments and to reduce the financial risks associated with the governance, environmental and social practices of companies in our portfolio. In line with international standards, we also carry out sustainability due diligence and promote responsible business conduct. Our responsible investment work is directed at the market, portfolio and company level.

Starting from international standards and informed by our dialogue with companies, academics and stakeholders, we set our own priorities as an investor. Our public positions on governance and expectations of companies on sustainability matters, which are primarily directed at company boards, communicate our views to the wider market and ensure predictability for the companies we invest in.

Market

Our goal is to contribute to well-functioning markets, good corporate governance and strong shareholder rights . We promote these economic interests in a predictable way through clear and transparent principles and policy engagement. We support academic research to increase understanding of relationships between financial risk and return, and governance and sustainability.

Portfolio

Our goal is to integrate governance and sustainability considerations into investment decisions and assess companies’ ability to create value. This helps us manage risks and identify investment opportunities, including by investing in the transition to a low-carbon economy. There are also companies we choose not to invest in because of sustainability or governance issues that create high risks for the fund.

Companies

Our goal is to promote value creation and reduce risk at the companies we invest in through active ownership. We do this through dialogue with companies and voting at their shareholder meetings. We prioritise our largest holdings and companies with the most significant risks. Where alleged conduct raises significant concerns about market integrity, we may consider legal action to protect our interests.

2. Market

Market standards

As a market participant in 68 countries, we benefit from well-functioning and legitimate markets, global solutions to common challenges, and broadly agreed international standards.

Engaging with standard setters

We engage with relevant international organisations, standard setters and regulators to contribute to the development and adoption of standards on corporate governance, corporate disclosures, responsible business conduct and climate and nature risks. We also participate in the development of best practices for responsible investment. We share our investor perspective with standard setters by responding to public consultations and meeting their experts. We speak at conferences and take part in selected initiatives to reach a wider range of market participants. We do not engage with members of parliament or foreign governments, nor do we engage lobbyists or make political contributions.

“As a long-term investor, we support reporting frameworks that deliver financially material information without unnecessary burdens for companies. Whether for semi-annual corporate updates or sustainability disclosures, we advocate for streamlined approaches that focus on what matters for investment decisions and eliminate duplication.”

Nicolai Tangen

Chief Executive Officer

Responding to consultations and meeting with regulators

In 2025, we responded to 34 public consultations on issues related to corporate reporting, corporate governance, shareholder rights and climate and nature disclosure. We submitted 4 consultation responses to global standard setters, in addition to 13 consultation responses in Asia-Pacific, 12 in Europe, 3 in the Americas and 2 in the Middle East and Africa. We held meetings with standard setters, securities regulators, prudential supervisors, stock exchanges and other relevant stakeholders.

We published an Asset Manager Perspective on the frequency of corporate reporting, arguing that mandatory quarterly reporting, and the associated pressure on management to meet earnings guidance, can lead to short-term decision-making.

At the ASEAN Capital Markets Forum in Malaysia, we presented our investor views on physical climate risk mitigation and transition.

Improved sustainability reporting

Companies today navigate crowded sustainability reporting requirements that are duplicative and disconnected from financial statements, creating costs for companies and confusion for investors.

In 2025, we pushed for change. We want reporting that is simpler, more useful for decision making, and tailored to what matters in each industry. The information provided should enable investors to assess risks and opportunities without over-burdening companies.

Simplifying rules

The map to net zero is complicated enough - net zero standards should not make it harder. We urged the Science Based Targets initiative to balance scientific rigour with real-world implementation. We advocated for streamlined European Sustainability Reporting Standards that align with the International Sustainability Standards Board (ISSB) global baseline, reducing duplication.

Industry-specific focus

We supported the ISSB’s review of the industry-specific SASB standards, which provide metrics on sustainability issues that drive value in each sector. This sector lens helps for example steel companies report on metrics relevant to their businesses, while food companies focus on theirs - enabling more relevant and comparable disclosures within industries.

Staying connected

We called for consistency between companies’ financial statements and sustainability reports. When climate risks affect financial returns, both reports should consistently reflect that information.

Governance reform in Asia

Asia is a large market for the fund, with 18 percent of our holdings. We engage with financial regulators and stock exchanges in Japan, China, South Korea and Singapore to enhance corporate governance, protection of shareholder rights and disclosure standards.

To improve and attract global capital, Asian regulators are encouraging companies to move beyond a compliance mindset and use governance as a tool to increase long-term shareholder value creation. We support regulatory reforms that deliver stronger boards, greater transparency and accountability to shareholders. Improving the way Asian companies are governed and managed benefits the fund’s risk and returns.

We respond to public consultations and supported:

- Strengthened corporate governance code in China

- Enhanced disclosure requirements in China and Malaysia

- Robust minority shareholder protections in Singapore

- Stewardship codes promoting dialogue between boards and investors in Japan

We advocate for independent and diverse boards with industry expertise to guide companies to develop capital efficiency plans that consider the cost of capital. We encourage boards to consider the full range of measures to -improve price-to-book ratios and return on equity. These include optimising dividend policies, share buybacks, strategic investments, unwinding cross-shareholdings and divestments of non-core assets, accompanied by transparent disclosure practices.

Participating in organisations and initiatives

International organisations and standard setters

We have long contributed to the development of principles for responsible investment and participate in various organisations and initiatives. In 2025:

- We became a patron member of the European Corporate Governance Institute, continuing our longstanding collaboration. Exchanging views and considering evidence-based research on governance and sustainability questions remain fundamental to our responsible investment work.

- We joined the Singapore Sustainable Finance Association (SSFA) established by the Monetary Authority of Singapore and the financial industry to shape policy developments that support Asia’s climate transition. SSFA’s new project on adaptation and resilience aligns with the increased focus on physical risk in our climate action plan.

- We joined the ISO Working Group on Corporate Net Zero, which is developing the standard for Net Zero Aligned Organizations. This work complements our engagement with the Science-Based Targets initiative on the update to their corporate net zero standard.

- We have supported Carbon Risk Real Estate Monitor (CRREM) as a founding sponsor since 2019. CRREM aims to facilitate the global standard for climate transition risk analysis in real estate. In 2025, to further support these efforts, we joined its Foundation Board.

We were present at FIR – PRI Awards Ceremony at the Sorbonne University in Paris.

At Shanghai Stock Exchange, we presented to listed companies our investor expectations on sustainability-related financial information.

Working with other investors and companies

To share our views, we may join investor coalitions or initiatives that are consistent with the fund’s mandate and support our management objective. However, we do not collaborate with other investors on investment decisions or voting at shareholder meetings, nor do we participate in coalitions that are primarily aimed at policy makers.

- US CEO pay: : We have worked with other asset managers over the last three years to provide greater investor support for simple stock awards and extended stock lock-ins, to better align the interests of CEOs with the interests of long-term shareholders. In 2025, the proxy advisor Institutional Shareholder Services changed its US policy. It will now view simple stock awards with extended time horizons positively, removing a key obstacle for companies agreeing with our position paper. As part of our efforts, we hosted a session on executive pay at the Council of Institutional Investors Fall Conference. At a roundtable at the Securities and Exchange Commission, we suggested that current compensation disclosure rules may inadvertently drive incentive complexity.

- Ocean-related disclosures: We co-hosted an event with CDP alongside the UN Oceans Conference in Nice. We have advocated for standardised ocean sustainability disclosure standards for years, including through support for CDP’s work. From 2026, CDP will integrate ocean sustainability into its questionnaire, complementing frameworks such as the Taskforce on Nature-related Financial Disclosures.

Children's rights in the digital world

In a rapidly digitalising world, the safety and rights of children online have become increasingly important. UNICEF’s review of 195 corporate reports shows that only 27 percent of companies provide meaningful disclosure on children’s digital rights.

In 2024, together with UNICEF, we launched a collaboration to develop disclosure guidance designed to help companies report better on how they impact children’s rights in the digital environment. To make these disclosures applicable and tailored to what actually matters, a number of experts and businesses were consulted and contributed to shaping the recommendations - through workshops, webinars and bilateral consultations.

The guidance was launched in 2025, targeting businesses, civil society, and policymakers. The recommendations apply across multiple sectors, extending beyond technology companies.

Engaging with our stakeholders

We value the ongoing dialogue we have with stakeholders. The information they share with us forms an important part of our responsible investment work, informing both our company engagements and our risk monitoring.

In 2025, we organised seminars with civil society organisations at our Oslo, London and Singapore offices where we presented our work and received input on various topics. We also invite civil society to a presentation of our annual Responsible Investment report. In 2025, civil society shared information about a range of topics and company practices, including risks in war- and conflict-affected areas, transition plans, deforestation, nature and labour rights. We also received significant input on our 2030 Climate action plan.

NGO seminar in Oslo

We communicate our work on responsible investment through press conferences, seminars, interviews, and op-eds in Norwegian news media. At Arendalsuka, an annual festival for open public discourse in Norway, we discussed our work with companies in war- and conflict-affected areas, nature and AI. To strengthen understanding of the fund’s role, we held 13 guest lectures at Norwegian and international universities on our approach to responsible investment. Our CEO’s podcast interviewing CEOs of companies we invest in reaches a broad, global audience.

Transparency about our work builds trust and knowledge about the fund. For the third year in a row, the fund has been recognised as the world’s most transparent fund in the category Responsible Investing by the Global Pension Transparency Benchmark.

AI-event at Arendalsuka 2025.

Research

We aim to strengthen the scientific foundation of our responsible investment efforts. Academic research can help improve market standards, provide new data and inform our responsible investment with new insights.

We collaborate with academics and provide funding in areas where we need a better understanding of how governance and sustainability affect the fund’s financial risks and returns. We make the research findings publicly available, contributing to knowledge building.

Presenting our climate and nature disclosures in March.

Supporting academic research

|

Topic |

Partner |

Purpose |

|---|---|---|

|

Climate finance |

University of Cambridge and Imperial College London |

Publish a journal issue on Biodiversity and Natural Resource Finance to advance research in this developing field. Generate knowledge on how biodiversity loss affects asset prices, nature solutions interact with carbon markets, and supply chain dependencies create corporate risk exposures. |

|

National Bureau of Economic Research |

Host three annual conferences advancing research on climate and financial risk measurement, climate transition amid geopolitical tensions, and effectiveness of investor climate actions. Generate research findings to inform investment strategies, risk management, and ownership work. |

|

|

New York University |

Support two conferences and research on the interconnected risks of climate and biodiversity loss. Create publicly available data on companies’ exposure to nature risks and ecosystem fragility. Identify tipping points and feedback loops critical for systemic risks assessment. |

|

|

Economics of natural resources |

University of Minnesota |

Support research on how resource scarcity and climate impacts will reshape economies over long-term investment horizons. Provide frameworks to anticipate constraints on growth, evaluate climate vulnerabilities across geographies, and identify risk and opportunities in resource availability for investment decisions. |

|

Setting CEO incentives |

National Bureau of Economic Research |

Host conferences generating evidence on how CEO compensation drives corporate behaviour and long-term value creation. Address the complexity in incentive structures. Inform our stewardship work on compensation structures that align management interests with long-term shareholder interests. |

Collaborating with researchers

|

Topic |

Partner |

Purpose |

|---|---|---|

|

Corporate perceptions of nature risk |

University of Zürich |

Understand better our portfolio companies’ perception of nature risk and the actions taken to address it. |

|

Effect of voting pre-disclosure |

École Polytechnique Fédérale de Lausanne and HEC Lausanne |

Understand the effect of pre-disclosing our voting intentions prior to shareholder meetings on vote outcomes and ultimately corporate decisions. |

The corporate view on nature risk

We have known for a long time that climate and nature are interlinked. Climate risk is financial risk affecting the fund’s long-term returns. When we work with climate risk, we cannot ignore nature risk. We want to better understand how companies perceive and manage nature risk.

In 2025, we partnered with University of Zürich researchers to survey our portfolio companies on their perceptions of this emerging risk. The findings based on nearly 400 responses will guide us in the implementation of our 2030 Climate action plan:

- Nearly half of the responding companies view nature risks as financially material, with many reporting physical risks already having financial effects today.

- Among companies that have experienced investor engagement on nature topics, most view it as value-generating, and over half report it has influenced their strategic and operational decisions.

- While half of the companies believe investors continue to prioritise climate issues over nature in their strategies, many of these respondents consider climate and nature risks to be too intertwined to rank one over the other.

The research is published by the Review of Finance in a special issue on Biodiversity and Natural Resource Finance.

3. Portfolio

Investments

Governance and sustainability considerations are integrated into our investment processes across all asset classes. We believe this improves the fund’s returns and reduces risk.

Investing sustainably

Integrating governance and sustainability into investment processes

Our management mandate has specific requirements for responsible investment. Strong governance and sustainable business practices help companies create value, build resilience, and manage risks. This supports the fund’s financial goal.

We integrate governance and sustainability information throughout the investment process. Our portfolio managers are required to consider sustainability in their analyses. They are well-versed in our expectations on sustainability and positions on governance, and collaborate closely with our investment stewardship managers. In 2025, portfolio managers attended 3,078 meetings with companies, discussing governance and sustainability topics at 45 percent of them. Understanding the views of the company board or management improves the quality of our investment analysis and makes our responsible investment efforts more relevant.

In 2025, portfolio managers participated in voting decisions at 613 companies. These companies are among our largest investments and together made up 64 percent of the equity portfolio’s market value.

We use AI to provide governance and sustainability insights to our portfolio managers and stewardship professionals, building tools that strengthen our company meeting processes and deliver customised investment intelligence.

We screen potential initial public offerings for sustainability and governance risks. This integrates sustainability into our investment process from the earliest stages of companies’ entry into the fund’s investment universe.

“Active investing requires deep company understanding. When we analyse businesses, governance and sustainability are not separate considerations – they are central to assessing competitive advantage. We engage with companies to understand how they navigate complex challenges and create value over time. We want to identify companies with strategic clarity that will thrive over decades.”

“Strong governance and sustainable business practices indicate management quality and operational excellence. Our permanent capital allows us to support companies making necessary transitions, creating value beyond quarterly results.”

Daniel Balthasar

Co-Chief Investment Officer Active Strategies

* Companies are categorised as Solutions when companies’ avoided emissions from low-or zero-carbon products/services exceed their combined operational emissions and product emissions.

Investing in the energy transition

The fund has significant investments in companies supporting industrial decarbonisation and companies involved in the energy transition. Our investment efforts seek to capture the financial opportunities arising from the energy transition and enhance the way in which climate change considerations are integrated into investment decisions across relevant investment strategies.

Global energy investments have shifted significantly over the past decade. According to the IEA’s World Energy Investment 2025 report, capital flows to the energy sector are set to rise to USD 3.3 trillion in 2025. Between 2015 and 2025, investments in renewables more than doubled, and investments in grids and storage grew by more than 40 percent. Renewables, grids and storage represent the largest combined segment of global energy investment. At the same time, investments in grids are struggling to keep pace with increased power demand and renewables deployment.

Up to 2 percent of the fund can be invested in unlisted renewable energy infrastructure. At the end of 2025, these investments represented 0.4 percent of the fund, up from 0.1 percent in 2024. We conduct due diligence on every investment, assessing risk factors related to health, safety, environment, corporate governance and social considerations.

Further information about our investments in renewable infrastructure in 2025 can be found on our website, www.nbim.no.

Investing in Europe’s energy grid

Renewable generation in Europe is expanding rapidly, but transmission infrastructure could become a critical bottleneck. The European grid requires significant investments to ensure that clean electricity from wind and solar reaches industries and consumers efficiently.

We see transmission infrastructure as both a strategic investment opportunity and an essential enabler of the energy transition. In 2025, we signed an agreement to invest up to EUR 4.5 billion in Germany’s largest electricity transmission operator, which manages 14,000 kilometres of grid infrastructure from the North Sea to the Alps. Together with the Dutch pension provider APG and Singapore’s GIC, we collectively committed EUR 9.5 billion in new equity through 2029. The investment will finance the expansion of transmission infrastructure, integrating onshore and offshore wind, solar, and cross-border connections in Germany’s electricity network.

This investment is part of the fund’s renewable infrastructure strategy. Since 2021, we have invested in offshore wind across the Netherlands, UK, Germany and Denmark, and in onshore wind and solar in Spain.

As electricity demand and renewable generation grow, transmission systems will require significant capital and long-term commitment - characteristics that align with the fund’s investment horizon and return objectives.

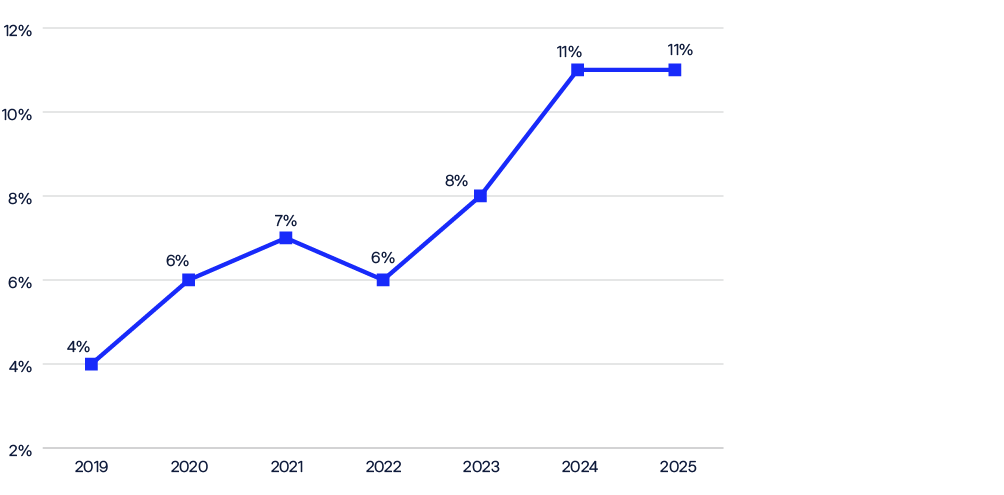

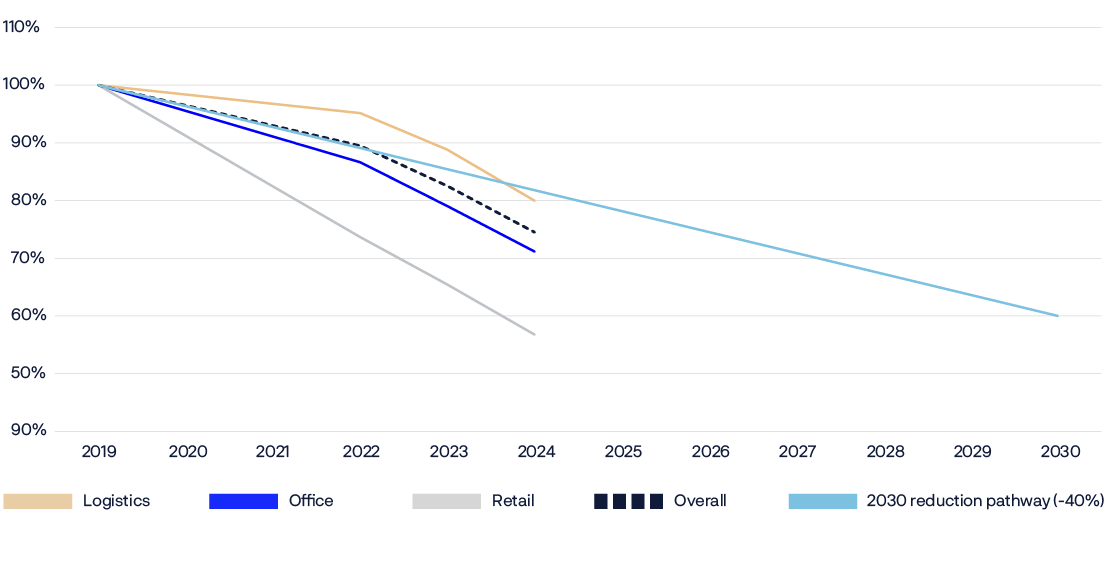

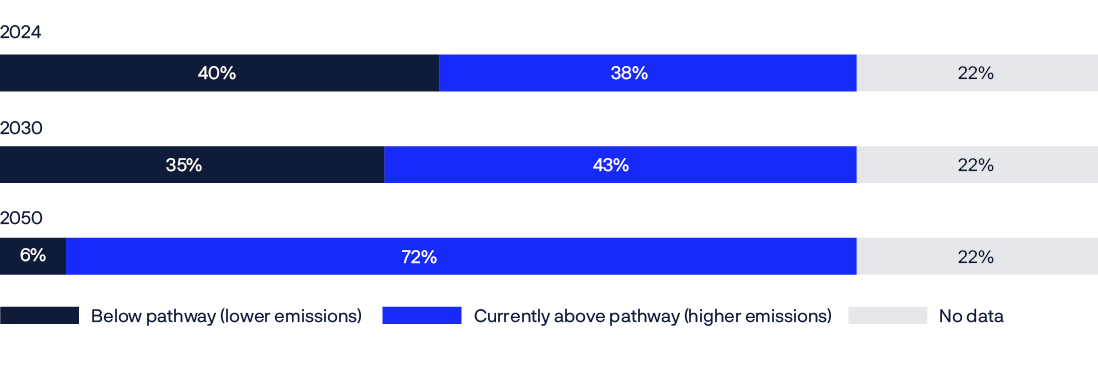

Managing sustainability risks and opportunities in unlisted real estate investments

Unlisted real estate investments represented 1.7 percent of the fund at the end of 2025. Climate risk has direct financial implications for real estate asset values through physical hazards and transition-related costs. We integrate sustainability risks and opportunities into our investment process to enhance operational efficiency and preserve long-term asset value. We have developed a framework to identify, assess and manage these risks across the fund’s unlisted real estate investments.

We are targeting net zero emissions by 2050 for our unlisted real estate investments. To measure progress, we have an interim target to reduce operational carbon emission intensity by 40 percent by 2030 against a 2019 baseline. From 2019 to 2024, the real estate portfolio’s carbon emission intensity fell by 25 percent.

Carbon emission intensity varies significantly across our unlisted real estate portfolio due to sector-specific characteristics and geographical market dynamics. We report emission reductions disaggregated by sector and geography to ensure transparency and enable targeted performance analysis. See our 2025 Climate and nature disclosures for further information.

We measure transition risk by comparing our unlisted real estate portfolio against 1.5°C decarbonisation pathways from Carbon Risk Real Estate Monitor (CRREM). This framework shows when buildings exceed their carbon budget and helps us prioritise retrofits and investment decisions.

In 2024, 40 percent of the unlisted real estate portfolio by value was below its carbon budget compared with 35 percent in 2023. Without further improvements, 35 percent of the portfolio is projected to be below its carbon budget by 2030. Planned interventions will aim to improve this over time.

Improving risk and return with external managers

We use external managers to manage parts of the fund’s equity investments, primarily in emerging markets and small-cap companies in developed markets. Their proximity to the markets and expertise in specific regions and sectors enhance returns and help mitigate investment risk. We conduct annual due diligence on our external managers, assessing their integration of governance and sustainability factors. The fund had 1,062 billion kroner, or 5.0 percent of its capital, invested with external managers at the end of the year.

In 2025, 59 percent of our external managers were signatories to the PRI.

Investing sustainably in fixed income

We own sustainability labelled bonds issued by public entities, including sovereign, supranational and agency issuers, and the private sector. Most of these labelled bonds are green bonds, a type of fixed-income instrument that is specifically aimed at raising money for climate and environmental projects. We also invest in social and other labelled bonds. Our view is that labelled bonds should adhere, at a minimum, to the International Capital Market Association’s principles.

At the end of 2025, green bonds in the fixed-income portfolio amounted to 113 billion kroner, based on the definition for the Bloomberg Barclays MSCI Green Bond Index.

Presenting our investor views at the KfW Capital Markets Conference on energy transition in Germany.

Building responsible investment knowledge

We foster a responsible investment mindset and build this awareness across the organisation. We regularly hold sessions for employees or invite external speakers to talk about governance and sustainability-related developments. Some of the topics covered in 2025 were nature finance, ethical considerations in responsible investment, human rights and the effectiveness of our engagements. We also included lectures on responsible investment in our internal Investment Academy training programme. During Norges Bank’s Climate Conference, experts were brought together to explore how climate change and the energy transition affect the macroeconomy and financial markets.

Our Climate Advisory Board has supported us in the implementation of the 2025 Climate action plan and the development of our 2030 Climate action plan. In 2025, we had three meetings with the Board, alongside several bilateral consultations. Our primary focus was finalising the 2030 Climate action plan. We received further advice on how to progress our work on nature risk, and the relevance of environmental attribute certificates.

We published our 2030 Climate action plan in October.

Risk management

We monitor sustainability risks in the portfolio and implement risk mitigation measures for companies with high risks. Which actions we take depends on the level of sustainability risks and the nature of our investment.

Risk monitoring

“Effective risk management requires understanding companies beyond their financial statements. Poor governance and unsustainable business models may face regulatory challenges which can impact profitability. Systematic monitoring of sustainability factors helps us detect emerging risks and consider their relevance to long-term value creation. AI technology is reshaping how we do this work.”

Patrick Du Plessis

Global Head of Risk Monitoring

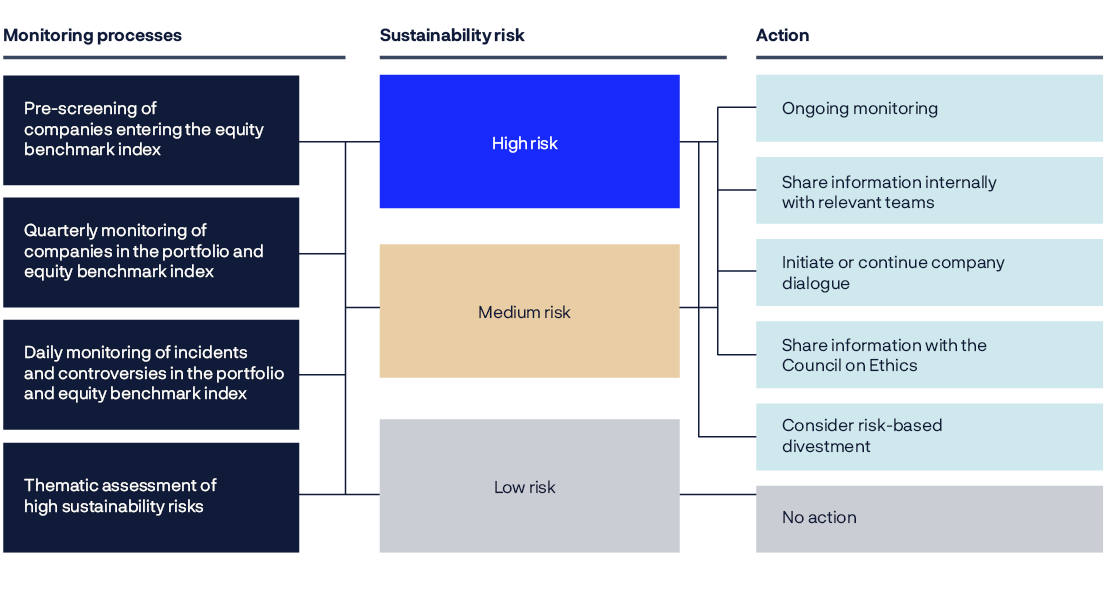

Each quarter, we screen all companies entering the fund’s benchmark (pre-screening) and all companies in the fund’s benchmark and portfolio (quarterly monitoring). Daily, we monitor news flows on sustainability-related incidents and controversies (daily monitoring). We may also conduct deeper analysis of companies in certain markets and sectors exposed to specific sustainability risks (thematic assessment). We implement risk mitigation measures for companies with heightened risks within the management mandate. As a result of our risk monitoring processes in 2025, we decided to divest or abstain from investing in 58 companies and initiated or continued dialogues with 73 companies.

Overview of our sustainability risk monitoring processes

Outcomes from our sustainability risk monitoring processes

|

Monitoring process |

Outcomes |

|

|---|---|---|

|

Number of companies |

Companies analysed |

Decided to divest from, or abstain from investing in |

|

Pre-screening |

423 |

17 |

|

Quarterly monitoring |

695 |

1 |

|

Daily monitoring |

200 |

18 |

|

Thematic assesment |

281 |

22 |

Pre-screening of sustainability risks

In line with the fund’s mandate, we invest in most companies entering our equity reference index. Four times a year, our index provider announces companies that will enter and exit the index. During that period, our risk and investment teams assess the sustainability risks of the companies’ business models.

When screening companies entering the benchmark, we may identify companies with significant governance or sustainability risks that could undermine long-term value. We can decide to abstain from investing. This creates a deviation to our benchmark and impacts the fund’s relative returns. These decisions are financially motivated, as we believe avoiding investments in companies with material sustainability risks reduces long-term financial risk.

In 2024, a small consumer staples company producing agricultural commodities entered our benchmark index. Our analysis identified indications of fraudulent financial reporting and corrupt business practices, including tax evasion and money- laundering schemes. The company’s financial track record was also concerning, with excessive debt and unpaid supplier obligations. We abstained from investing in the company. In 2025, this decision generated 52 million kroner in excess returns, as the company underperformed the market.

AI-enhanced risk monitoring

AI technology is becoming an integral part of our risk management work. Using AI, we have expanded the scope and scale of the information we analyse, enabling new forms of automation that lead to faster identification of material risks. These improvements contribute to more informed investment and risk decisions, safeguarding the fund’s financial returns.

In 2025, we deployed large language models (LLMs) to screen all companies on their first day of entering our equity portfolio. These tools help us rapidly scan a wide range of public information that goes beyond what data vendors typically cover. Where risks emerge around key themes, the LLM conducts deeper searches, providing contextual summaries.

We receive daily AI-generated risk assessments for investments made the previous day, enabling us to evaluate financial materiality and consider mitigation actions immediately.

Within 24 hours of our investment, the AI tools flag new companies in the fund’s equity portfolio with potential links to, for example, forced labour, corruption or fraud. Often, this information has not been captured in international media coverage or data vendor alerts. We always review the information before we make an investment or risk decision. In multiple instances, we identified and sold these investments before the broader market reacted to the risks, avoiding potential losses.

AI proves particularly valuable for researching smaller companies in emerging markets. In these cases, data vendor coverage may be limited, news may be limited to small media outlets in local languages, and controversies suggesting systemic failures in risk management may go unreported in international media.

Risk-based divestments

Risk-based divestments are investment decisions. They are active decisions within our tracking error limits that affect relative return. The risk and return implications for the fund are a central part of the assessment. If a divested company improves, we may reverse the divestment decision.

In 2025, we divested from 58 companies. Of these, 17 were companies that entered the fund’s benchmark index during the year. Altogether, we have made 633 divestment decisions since 2012.

We also reversed 14 risk-based divestments during the year. We re-assessed a range of cases from different industries, including healthcare facilities operators, pulp and paper manufacturers and professional services. These were initially divested for a variety of reasons, including patient abuse, aggressive tax minimisation or avoidance practices, labour mismanagement and contribution to climate change. Altogether, we have reversed 39 risk-based divestments since 2012.

Generating return through risk-based divestments

We divest from companies to reduce financial risk and generate excess return over time. We accept temporary underperformance if we believe the underlying risk motivating the divestment will not materialise in the short-term.

In 2018, we identified a steel producer with indications of systematic operational failures related to safety and environmental compliance. In one incident, dozens of workers were injured. The company faced ongoing regulatory actions, criticism and substantial environmental damage costs. We identified two critical risks to long-term value: inadequate operational controls around health and safety, and governance failures to address long-standing environmental liabilities. We decided to divest from the company.

During the initial years following the divestment, the stock tracked the broader market before outperforming slightly. This trend reversed. By 2025, our decision had generated 115 million kroner in cumulative excess returns as the company lost value relative to the market. The company exited the fund’s equity reference index in 2025.

Risk-based divestments in 2025.

|

Topic |

Criteria |

Divestments |

Reversed divestments |

|---|---|---|---|

|

Climate change |

Elevated risk related to high green house gas emissions, including coal mining and coal-based electricity generation |

5 |

3 |

|

Water management |

Insufficient risk management related to water use |

1 |

0 |

|

Biodiversity and ecosystems |

Exposure to markets associated with degradation of biodiversity and ecosystems |

5 |

1 |

|

Anti-corruption |

Exposure to markets with significant risk of corruption |

2 |

1 |

|

Insufficient risk management related to corruption and corporate governance |

0 |

||

|

Tax and transparency |

Elevated risk of aggressive tax planning |

0 |

4 |

|

Human rights |

Exposure to markets with significant risk of violations of human rights violations |

19 |

2 |

|

Insufficient risk management related to human rights |

0 |

||

|

Human capital management |

Exposure to markets with significant risks related to human capital management |

4 |

1 |

|

Insufficient risk management related to human capital management |

0 |

||

|

Consumer interests |

Insufficient risk management related to consumer interests |

5 |

1 |

|

Children’s rights |

Exposure to markets with significant risk of violations of children’s rights |

2 |

|

|

Insufficient risk management related to children’s rights |

0 |

||

|

Other |

Exposure to other significant sustainability risks |

15 |

1 |

Further information about our risk-based divestments can be found on our website, www.nbim.no.

Impact on the fund’s equity returns

The impact on the equity portfolio from risk-based divestments was -0.04 percentage points in 2025. Since 2012, risk-based divestments have increased the cumulative return on equity management by 0.68 percentage point, or 0.01 percentage point annually, equating to 12 billion kroner. Risk-based divestments linked to climate change and human rights have increased the cumulative return on equity management by 0.36 and 0.15 percentage point respectively.

However, like all equity positions, this portfolio experiences value fluctuations in the short- and medium- term driven by market factors.

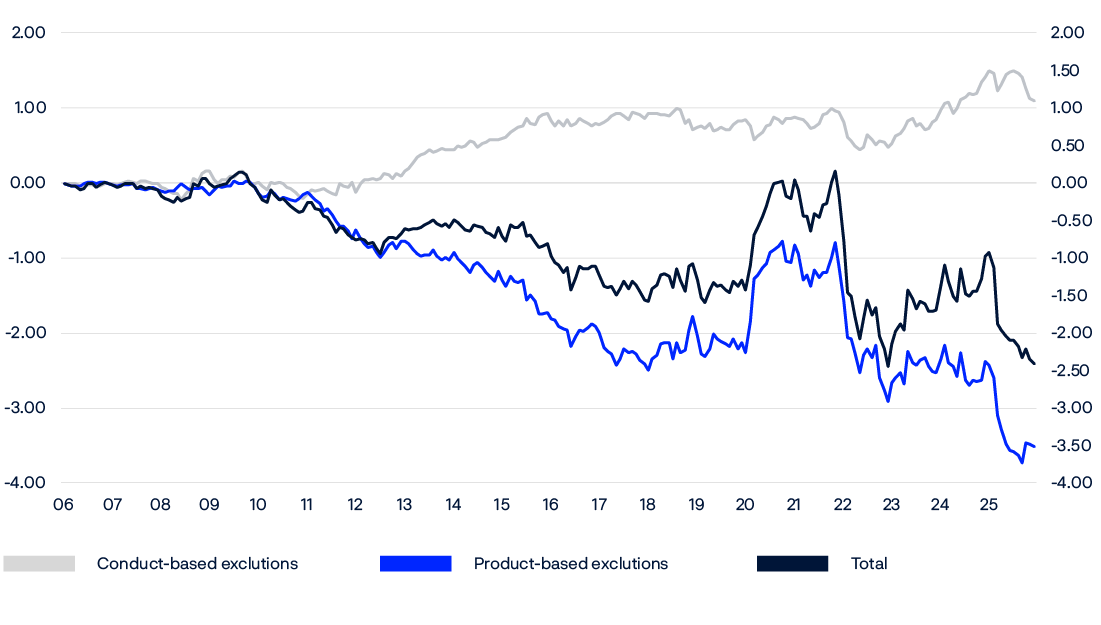

risk-based divestments. Measured in dollars. Percentage points.

Ethical considerations

Until November 2025, the Executive Board of Norges Bank decided whether companies should be excluded from the fund's investment universe or placed under observation, in accordance with guidelines established by the Ministry of Finance. The Executive Board's decisions on exclusion or observation of companies were based on recommendations from the independent Council on Ethics, which is appointed by the Ministry of Finance. For the product-based coal criterion, recommendations came from Norges Bank Investment Management.

In November 2025, the Government appointed a committee to review the ethical framework. The committee is to deliver its report by 15 October 2026. Pending a new framework, the Ministry of Finance has established temporary ethical guidelines.

Under the temporary ethical guidelines, Norges Bank shall not decide on observation or exclusion, but may reverse previous decisions on observation and exclusion. The Council on Ethics shall continue to monitor the fund’s investments and inform Norges Bank about companies where active ownership may be appropriate. The Council may recommend reversing previous decisions on observation and exclusion.

Under the guidelines effective until November 2025, Norges Bank announced the exclusion of 10 companies in 2025, placed three companies on the observation list, while reversing the exclusion of one company and removing one from observation. In addition, when the temporary guidelines came into effect, Norges Bank was in the process of implementing the exclusion of four companies based on a recommendation from the Council on Ethics and one company on Norges Bank’s own initiative based on the coal criterion.

Further information about ethical exclusions and list of companies excluded or under observation can be found on our website, www.nbim.no.

Impact on the fund’s equity returns

Product-based exclusions have reduced the cumulative return on the equity benchmark index by around 3.51 percentage points, or 0.04 percentage point annually. It is mainly the exclusion of weapons manufacturers that has reduced returns, but the absence of tobacco companies has also played a role. Conduct-based exclusions have increased the cumulative return on the equity benchmark index by around 1.10 percentage point, or 0.01 percentage point annually. The exclusion of companies due to severe environmental damage has contributed particularly positively.

Since 2006 the equity benchmark index has returned 2.42 percentage points less than it would have done without any ethical exclusions. On an annualised basis, the return has been 0.03 percentage points lower.

4. Companies

Dialogue

We meet the companies in the fund regularly to promote good corporate governance, sustainable business models and responsible business practices. Our investment and active ownership teams discuss a wide range of topics material to long-term value. The aim is to contribute to improved value creation and reduced risks.

“We are a long-term shareholder, and company dialogues are a central part of our investment management. Well-governed companies with sustainable business models are essential for the fund’s lasting value creation. We communicate our views to our portfolio companies through constructive dialogue. We do not micromanage them – we are there to understand their strategy and be a supportive investor while also challenge the board and management when needed. We want companies to succeed –when they win, we win.”

Carine Smith Ihenacho

Chief Governance and Compliance Officer

Our expectations of companies on key sustainability topics, position papers on corporate governance issues, voting guidelines and disclosure of voting intentions provide a basis for our company dialogues. Our expectations and responsible investment management policy are based on standards such as the UN Global Compact, the OECD Guidelines for Multinational Enterprises, International Labour Organization conventions and the UN Guiding Principles on Business and Human Rights. They also largely coincide with the UN Sustainable Development Goals.

Our ownership dialogues take various forms, depending on whether we or the company want to discuss specific issues or have a more wide-ranging discussion. Companies often reach out to us as part of their annual shareholder interaction, or ahead of their annual shareholder meeting, to discuss executive remuneration or other items submitted for shareholder approval. These regular dialogues are the largest category of our company meetings. We prioritise dialogues with our largest investments, or where risks and opportunities appear heightened.

In 2025, we held a total of 3,198 meetings with 1,341 companies on topics material to long-term value creation. During these conversations, we communicate our views while gaining insights from the companies that inform our investment and ownership decisions. The topics range from performance and market developments to corporate governance and sustainability. Overall, we held 1,498 meetings with 815 companies in 2025 where governance and sustainability topics were discussed, covering 47 percent of our company meetings and 61 percent of the value of the equity portfolio.

We prioritise topics carefully, and raise those that appear to be most financially relevant to the companies, given their governance, location, sector and business model. The governance and sustainability topics we raise most frequently include capital management, climate change and human capital.

Further information about our ongoing dialogues and company engagements can be found on our website, www.nbim.no

Number of company meetings where governance and sustainability topics were discussed.

|

Category |

Topic |

Number of meetings |

Share of equity portfolio in percent |

|---|---|---|---|

|

Environment |

Climate change |

422 |

34 |

|

Circular economy |

111 |

8 |

|

|

Biodiversity |

46 |

3 |

|

|

Water management |

45 |

7 |

|

|

Deforestation |

22 |

1 |

|

|

Ocean sustainability |

4 |

1 |

|

|

Other environmental topics |

123 |

6 |

|

|

Social |

Human capital |

369 |

25 |

|

Consumer interests |

97 |

8 |

|

|

Human rights |

84 |

19 |

|

|

Tax and transparency |

35 |

1 |

|

|

Data privacy |

16 |

3 |

|

|

Anti-corruption |

15 |

3 |

|

|

Children's rights |

14 |

5 |

|

|

Other social topics |

150 |

9 |

|

|

Governance |

Capital management |

863 |

39 |

|

Board Composition |

222 |

25 |

|

|

Remuneration |

185 |

25 |

|

|

Financial Reporting & Audit |

52 |

4 |

|

|

Shareholder Rights |

41 |

4 |

|

|

Other governance topics |

319 |

24 |

Building long-term, strategic relationships

Strategic board dialogues

We meet boards of our largest holdings regularly. In meetings at board level, we prioritise strategic topics that are important for long-term value creation, both for the companies’ and the fund. This includes strategy oversight, board and management team composition, effectiveness and succession, executive incentives, and material risks and opportunities - including those related to sustainability.

In 2025, many companies faced increased regulatory and geopolitical risks. How company boards work together with management to navigate this complexity was a frequent discussion topic.

In addition to our strategic board dialogues, we hold many more board-level meetings with portfolio companies, as part of our company engagements. In 2025, we had 193 meetings at board level with 165 companies, accounting for 21 percent of the equity portfolio by value.

Developments in corporate sustainability disclosure

We measure systematically whether our portfolio companies disclose information on material sustainability issues in line with our expectations. These evaluations - which result in what we call expectation scores - assess companies’ disclosures on material topics such as climate risk and human rights. They inform our engagement priorities and voting and help us track whether companies improve their practices over time.

Sustainability data may often be incomplete or difficult to access. AI and machine learning enable us to analyse thousands of companies by extracting information not readily available from data providers and estimating key data points for companies that do not report, giving us a more complete picture.

For years, we saw consistent year-on-year improvements in sustainability disclosures across all topics. In 2025, the pace of improvement has slowed across topics. Noting that small changes can also be driven by measurement and data changes, it seems that while human rights, anti-corruption and climate disclosures continue to strengthen, nature appears to have plateaued.

Further analysis on climate and nature expectation scores can be found in our 2025 Climate and nature disclosures.

Expectation scores. Change from 2024 to 2025.

![[Alt text was not generated.]](/contentassets/d1cd789ca888460db2a8d742a254fdb2/en-gb-639070092872727285/imageeng_tekstbokser.png)

Addressing material risks and opportunities

Net zero dialogues

Climate risk is financial risk. A core part of our 2025 Climate action plan is to engage with the highest emitters in the fund’s portfolio on their plans for achieving net zero emissions by 2050. In our 2030 Climate action plan, we aim to increase our emphasis on physical climate risk, adaptation and resilience, and the intersection with nature.

In 2025, we engaged with 428 companies on climate-related topics, representing 44 percent of the fund’s financed emissions and 34 percent of the equity portfolio’s market value. Of these, 132 companies were engaged in specific net-zero dialogues, accounting for 40 percent of the fund’s financed emissions.

An overview of our net zero dialogues can be found in our 2025 Climate and nature disclosures.

Do our climate engagements make a difference?

As we developed our new 2030 Climate action plan, we faced a fundamental question: When we engage with companies on climate, do we see differences at the companies?

Using AI, we examined 32,000 company meetings over the past decade and analysed the meeting notes to track patterns. We saw a substantial shift – while climate featured in 7 percent of our meetings in 2015, this figure increased to almost 30 percent in 2024. Our analysis indicated a qualitative shift as well- our conversations with the companies have become increasingly substantive and strategic.

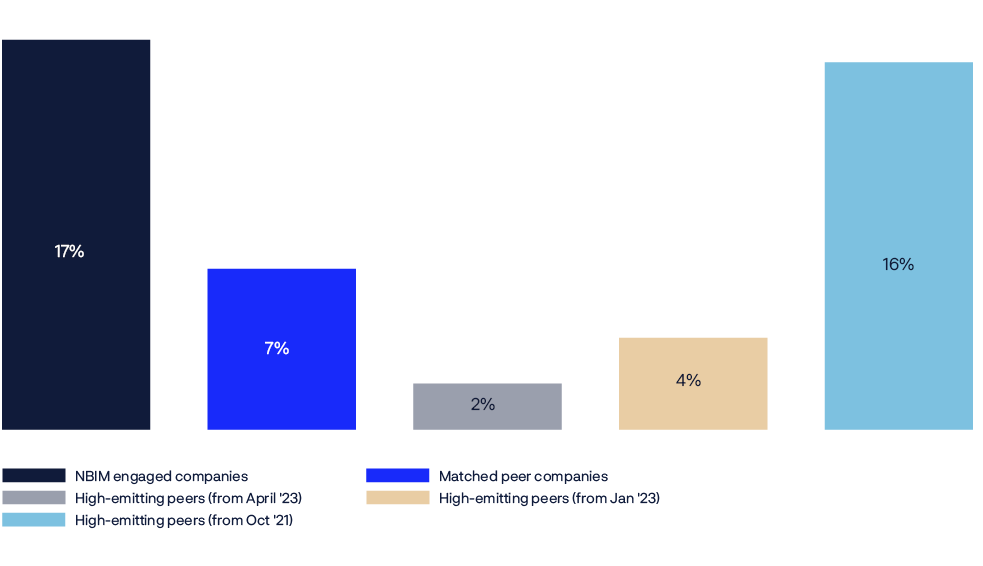

To better understand our impact, we concentrated our analysis on 59 companies from our 253 net zero company dialogues, where we had engaged specifically on net zero target adoption. We compared these companies with peer companies we did not engage with, using two control groups: companies matched on industry, size and emissions, and high-emitting companies just beyond our engagement threshold.

Our results showed that 17 percent of companies we engaged with established science-based net zero targets, compared to lower rates among comparable companies we did not engage. Although corporate decisions stem from many factors, this difference held across control groups. Our analysis suggests our company engagements can play a role in improving companies’ climate risk management, in line with the climate plan ambition.

Risk-based dialogues

We engage with companies on sustainability risks and opportunities that can be financially material and affect the fund’s value creation. Our risk-based dialogues are a central tool to address these risks as a long-term, minority investor.

We prioritise engagements based on the materiality of the topic, the severity of the risks and the size of our investment. We use different sources to identify which companies we should initiate dialogue with and which topics to address. These include outcomes from our risk monitoring processes and sustainability due diligence, as well as information from civil society or other third parties.

In 2025, we conducted 66 risk-based dialogues on topics across our sustainability expectations. The discussions are often part of a broader engagement with the company, or follow from our regular company dialogues.

Enhanced sustainability due diligence in war and conflict areas

Situations of war and conflict bring heightened risk for human rights violations, which requires enhanced due diligence. In 2025, we continued to strengthen our framework to better identify, assess and follow-up on portfolio companies’ exposure to conflict-affected and high-risk areas (CAHRAs).

We developed a systematic screening methodology that draws on multiple data sources to evaluate companies’ presence in regions where governance structures may be weak and human rights violations are more likely. AI tools enhance our ability to identify and assess these risks. This screening process helps us map heightened risks across our holdings, set engagement priorities, and focus relevant company dialogues on due diligence processes, stakeholder engagement, and risk mitigation measures.

This work is integral to our own sustainability due diligence. In 2025, we had 25 meetings as part of our dialogue focused on conflict-affected and high-risk areas. We encouraged companies to operate in accordance with emerging best practices, and gained valuable insights into company approaches, operational constraints, and potential risk mitigation actions.

In a letter to the Ministry of Finance, Norges Bank outlined its work under the mandate, the fund’s investments in Israeli companies and potential new measures that Norges Bank considered necessary. The Executive Board reviewed and updated their governing documents for the management of the fund, including the principles for responsible investment. The purpose was to strengthen Norges Bank’s overall responsible investment, particularly in situations that require enhanced due diligence.

We continue to prioritise this work given the volatile and rapidly evolving nature of conflict situations. At the same time, we recognise the complexity of the operating environments companies face, that investor engagement has its limits as an ownership tool, and the boundaries of our work as a responsible investor.

Dialogues about ethical criteria

We assess whether our portfolio companies’ operations violate fundamental ethical norms. Based on the ethical guidelines for the fund, we engage with companies to reduce the fund’s exposure to unacceptable risks.

Severe environmental damage

In 2013, the Ministry of Finance asked Norges Bank to include oil spills and environmental conditions in the Niger Delta in our ownership work with the oil and gas companies Eni SpA (Eni) and Shell PLC for a period of five to ten years. In 2023, the Executive Board of Norges Bank decided to extend this period by two additional years. The ownership dialogue with Eni ended in 2024. In March 2025, Shell PLC completed the sale of its onshore assets in Nigeria, and the Executive Board subsequently decided to end our ownership dialogue with the company.

In 2025, the Executive Board decided that we should initiate an ownership dialogue with the companies Rio Tinto Plc, Rio Tinto Ltd and South32 Ltd, based on a recommendation from the Council on Ethics related to a risk of severe environmental damage. The companies are part of the joint venture Mineração Rio do Norte (MRN), which operates a bauxite mine in the Brazilian Amazon.

We have three objectives for this engagement. First, we aim for MRN to adopt a leading practice, facility-level international environmental and social standard. Second, we seek to support MRN in achieving effective biodiversity management and restoration outcomes, including through a ‘no net loss of nature’ ambition. Finally, we aim for MRN to strengthen transparency around their environmental and social performance. In 2025, we conducted a site visit to the mine in Brazil and met each company separately and both companies together twice.

Serious violations of human rights

In 2024, the Executive Board decided that we should initiate an ownership dialogue with the companies Bolloré SE and Compagnie de l’Odet SE on their management of human rights risks, sexual violence, harassment and labor rights abuses over a period of up to two years. After attempted at engagement, the Executive Board decided in 2025 to exclude the companies based on the recommendation of the Council on Ethics from 2024.

Voting

We voted at 10,873 shareholder meetings in 2025, casting votes on 108,325 proposals, to express our views as an investor, promote long-term value creation by companies and safeguard the fund’s assets. We also published our third standalone voting review.

Our approach to voting

Voting is a core shareholder right and an important tool to support the fund’s long-term interests. Our company engagements, together with our global voting guidelines, inform our voting decisions.

We aim to be transparent, consistent and predictable in our approach to voting. To clarify our stance on corporate governance issues, we publish position papers. These are based on the G20/OECD Principles of Corporate Governance and best practices. Since 2021, we have published our voting decisions five days before the shareholder meeting.

We voted in line with the board’s recommendation

in 94% of all resolutions

for all agenda items in 70% of the shareholder meetings

How we voted in 2025

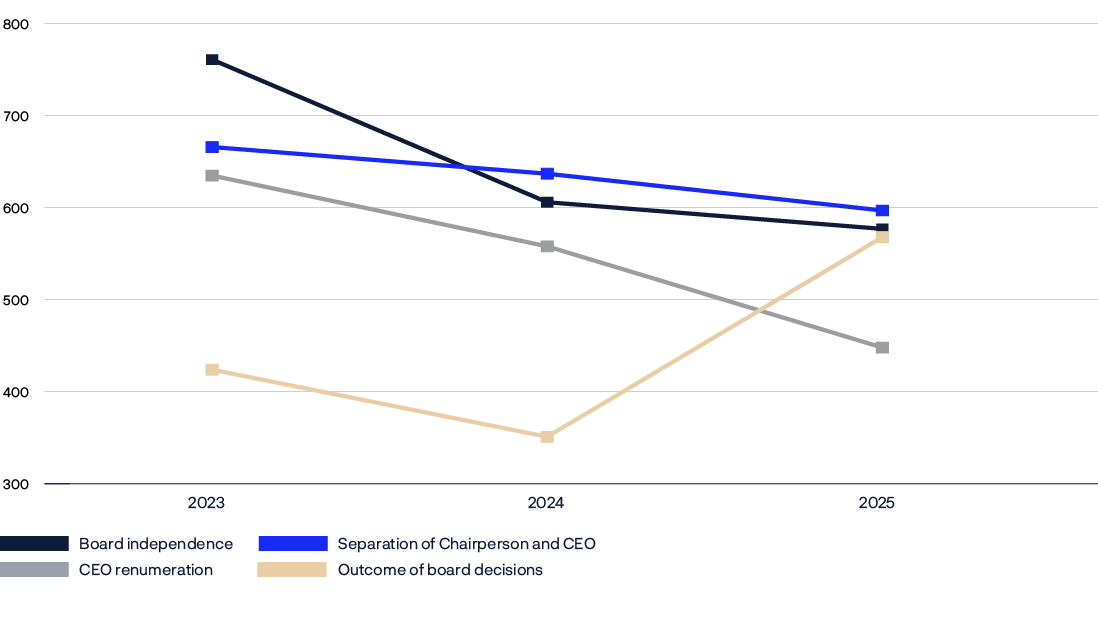

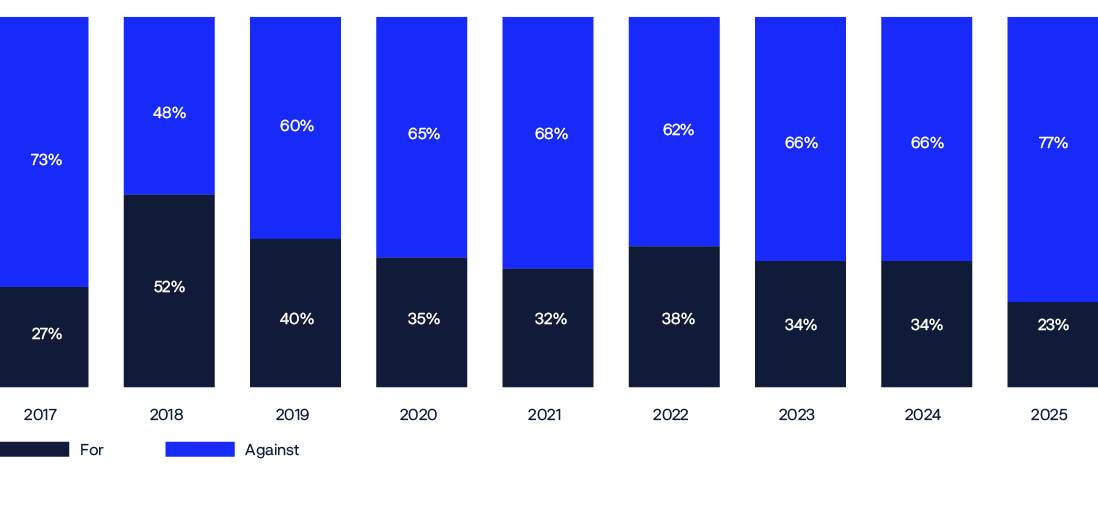

Our starting point is to support boards in their work. We voted in line with the board’s recommendations on 94 percent of all resolutions. Overall, we voted against a similar proportion of companies across different proposal types as in previous years, reflecting our aim to maintain a consistent approach. In some key areas, such as CEO pay, board independence and election of a combined chair/CEO, we voted against fewer proposals in 2025, reflecting evolving company practices, regulatory developments and changes to our portfolio.

Management proposals

Most items we vote on are management proposals, namely proposals submitted by the company’s board of directors. Items put to a vote vary by jurisdiction, but typically include the election of directors, approval of CEO pay, appointment of auditors, and changes to the company’s governing documents. In 2025, we voted on 105,985 management proposals, supporting 94 percent of these.

Effective boards

Director elections account for nearly four in ten of the resolutions we vote on. We delegate most decisions to companies’ boards and management teams - having boards that effectively represent our interests as a shareholder is critical to us and a topic we continuously engage on with companies. We supported 94 percent of the board members we voted on.

Board independence

We view board independence as a core component of good governance. Boards need a sufficient level of independence and objectivity to be well-equipped to guide strategy, oversee management and be accountable to shareholders.

Overall, we are seeing continued improvements in levels of board independence in developed and emerging markets. We saw a 4 percent reduction in votes against directors or other relevant proposals in 2025 due to independence concerns, compared to 2024. In Japan, improvements in board independence led to a 11 percent drop in votes against directors compared to 2024, and a 34 percent drop compared to 2023.

Separation of chair and CEO

We have a preference for the separation of chair and CEO roles. We believe that a non-executive chair is better positioned to guide strategy, oversee management and promote the interests of shareholders.

75 percent of the companies where we voted against proposals for this reason are in the US and South Korea. In the US , we opposed the election of the chair at 339 companies, or around 21 percent of the US companies where we voted. This number is down slightly from 343 companies in 2024, reflecting a steady, multi-year trend towards separation.

Board gender diversity

In our pursuit of effective boards with the diversity of skills, experience and perspectives necessary to fulfil their duties, we view having sufficient representation of each gender as an important indicator of board quality.

In 2025, our data continue to show a positive trend in the progress of women on boards in our portfolio, although the rate of improvement has slowed.

Board accountability

We believe that boards should be accountable, in their oversight role, for ensuring that companies manage material risks and do not contribute to unacceptable corporate governance and sustainability outcomes. In a small but important number of cases, we vote against directors and/or boards where we believe they have failed to fulfil their duties.

In 2025, we voted against board members at 222 companies due to governance concerns. A key driver was our strengthened stance on cross-shareholdings in Japan. We voted against board members at 116 Japanese companies where we assessed that cross-shareholdings were excessive and not aligned with shareholder interests.

We also voted against at least one director at 35 companies identified as having heightened sustainability risk. Of these votes, 28 were due to material failures in oversight, management and disclosure of environmental risks, while seven were due to social risks.

CEO pay

How a company’s management team is incentivised and rewarded can have a significant influence on decision-making and performance over time. This is particularly important in the case of CEOs, who we believe should be paid via simple packages primarily made up of a cash salary and shares that vest after five to ten years, regardless of resignation or retirement.

In 2025, we voted against a total of 315 pay packages globally. The US market continued to represent around four in ten of these votes (41 percent of votes against executive pay plans in 2025).

Shareholder proposals

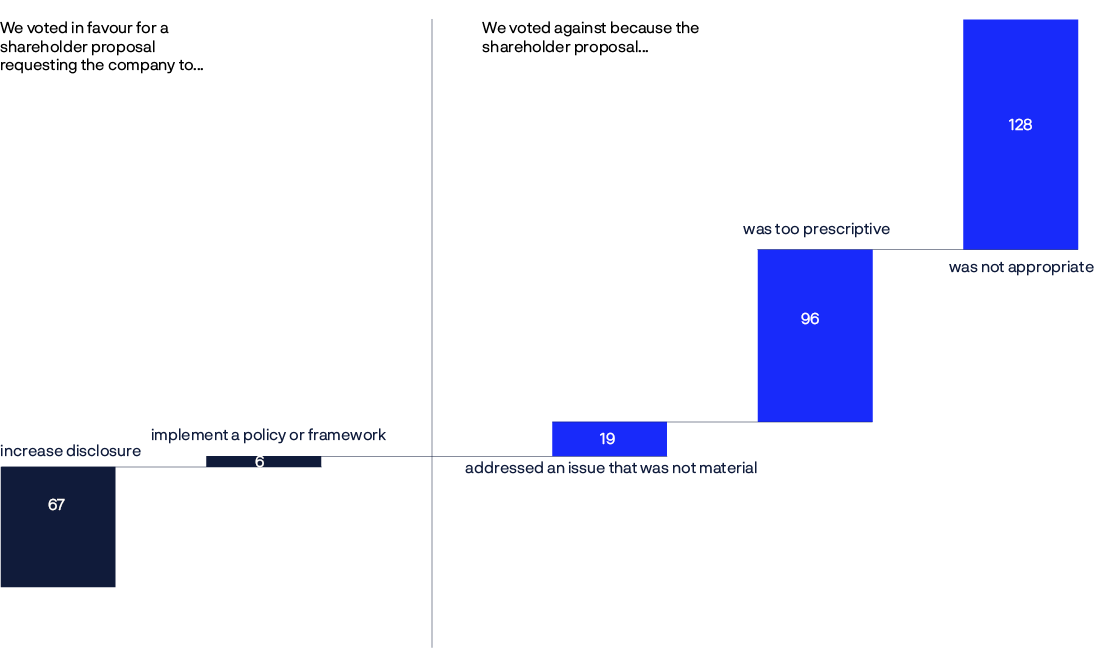

In many markets, shareholders can submit formal requests to companies, asking for a specific action, which all shareholders can vote on at the annual meeting. We conduct a case-by-case assessment of each shareholder proposal. Generally, we support proposals that highlight material gaps in disclosure, strategy or performance, especially where companies lag peers or our expectations of companies. However, we are cautious about proposals that impose rigid demands on companies and their boards.

As with all our voting, we aim to be consistent but may not vote the same way across different cases. Each year, companies make changes to their practices, standards evolve, and the risk picture changes.

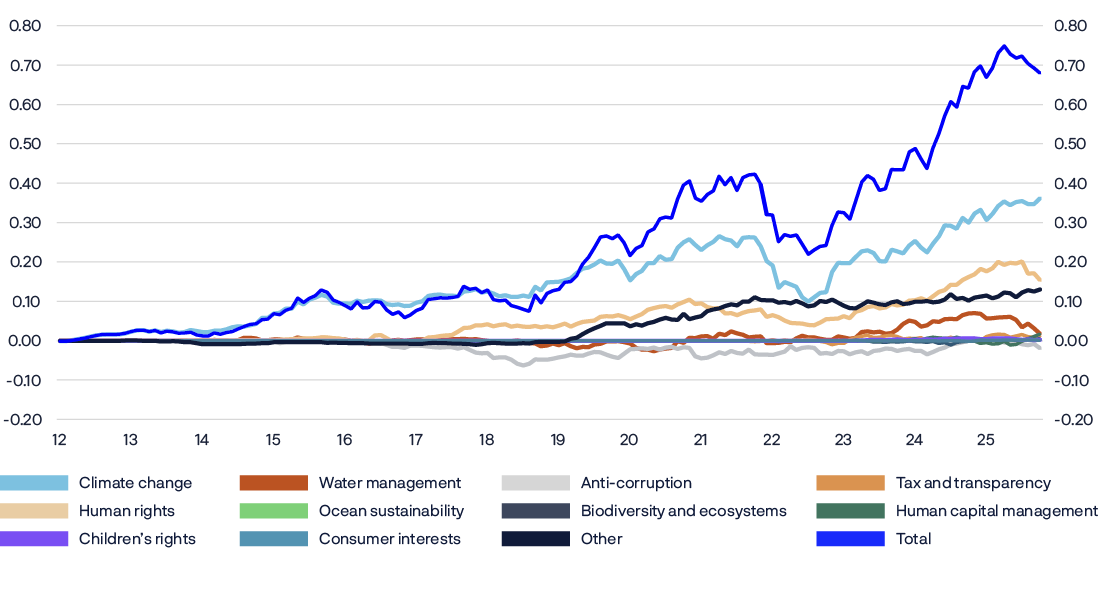

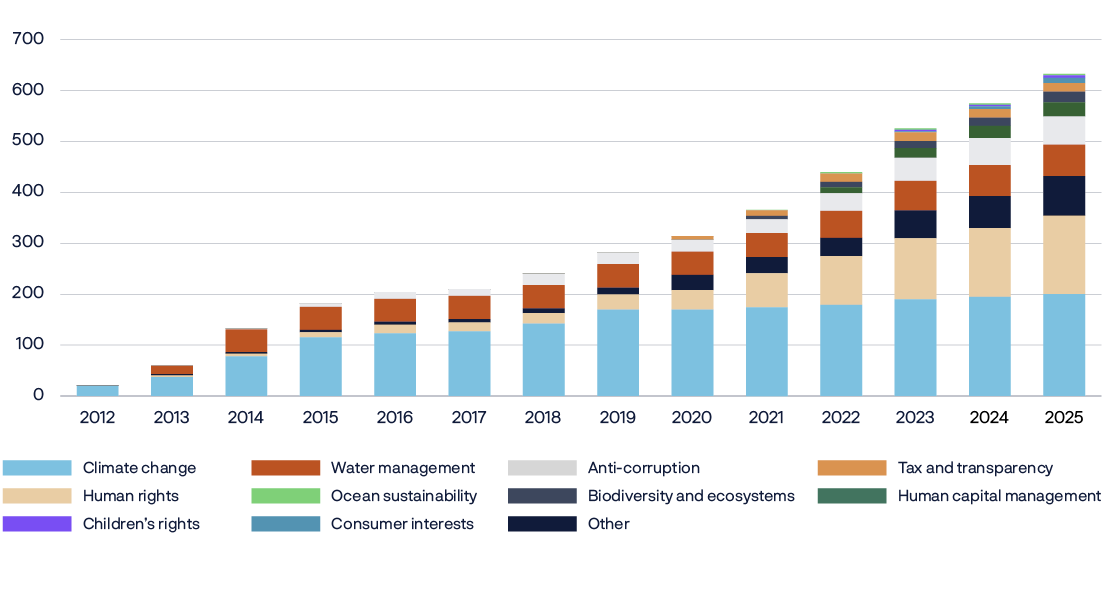

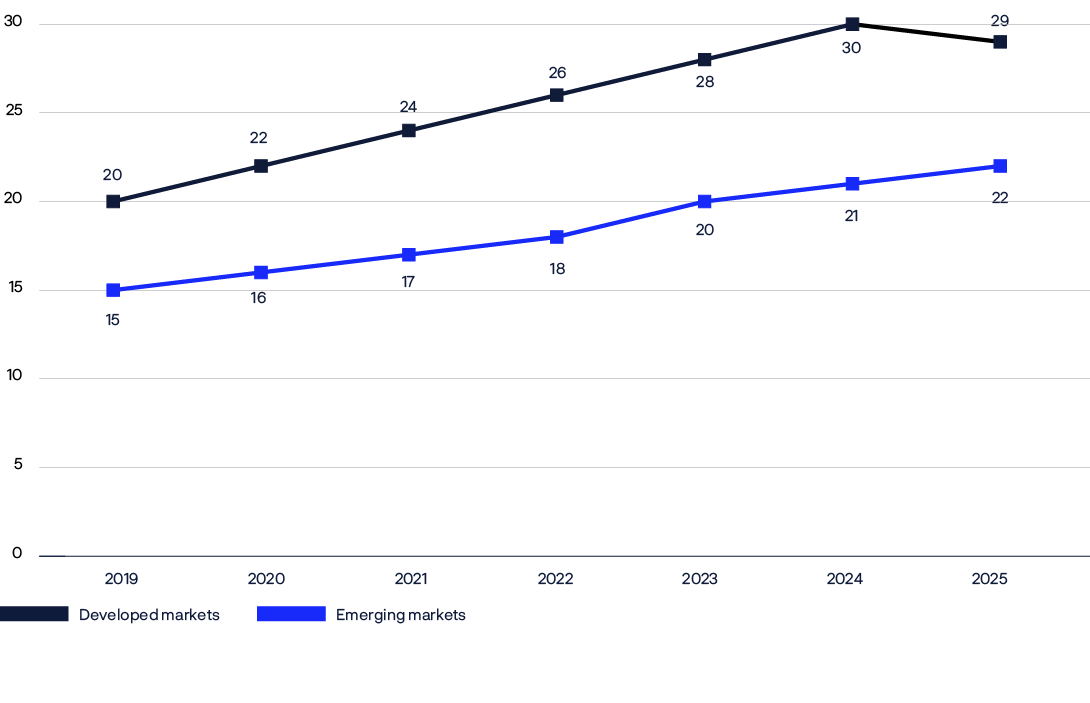

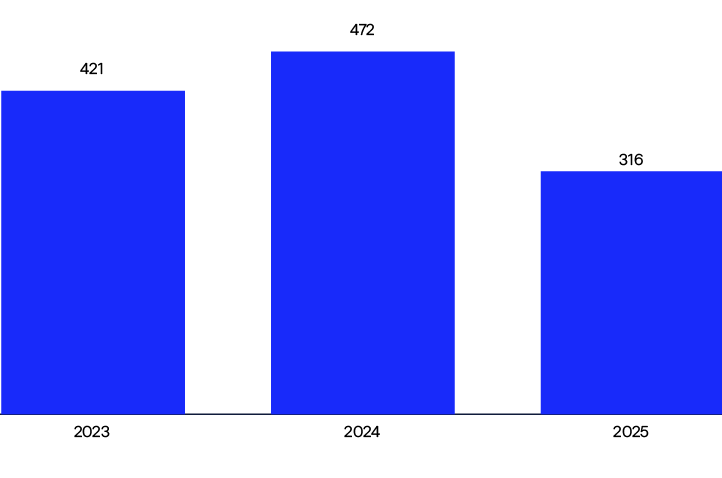

In 2025, the landscape for shareholder proposals changed. Companies are navigating an increasingly polarised landscape, with some facing competing shareholder proposals. We saw a notable drop in the number of sustainability proposals making it to the ballot – 316 in 2025 compared to 472 in 2024.

In 2025, we supported fewer sustainability-related shareholder proposals overall, reflecting what we considered to be a decline in the quality of the underlying proposals, with many appearing misdirected or lacking materiality.

Number of sustainability-related shareholder proposals

We continue to view well-structured shareholder proposals as a useful tool for escalating material concerns to the board, particularly where engagement has not led to sufficient progress. Support for proposals – even when non-binding – can prompt boards to act, especially when supported by a large share of the vote.

The main reasons for not supporting proposals are either that they are too prescriptive, or that we deem that the company already sufficiently meets our expectations on the topic.

Further information about our voting can be found on our website,

www.nbim.no.

Securities lending and voting

Securities lending is an integrated part of the fund’s investment strategy. In 2025, securities lending increased the return on the equity portfolio by 0.05 percentage point, or around 5.8 billion kroner. When we lend shares, we cannot vote on them. We therefore have internal guidelines to balance lending income with our ownership priorities.

What we always do

- Retain part of our shareholding so that we can vote all shareholder meetings

- Refrain from voting shares held as collateral

What we can do

- Limit lending when we a hold significant stake in a company

- Restrict lending when important votes are scheduled

Further reading

2025 Climate and nature disclosures

The management mandate for the fund, given to Norges Bank by the Ministry of Finance, includes requirements in the areas of responsible investment and climate risk. The mandate makes it clear that Norges Bank’s responsible investment efforts are to be based on a long-term goal that portfolio companies align their operations with global net zero emissions in line with the Paris Agreement. It also has requirements for managing and reporting on financial climate risks in line with international standards. Our 2025 Climate and nature disclosures, building on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and the Taskforce on Nature-related Financial Disclosures (TNFD), can be found on our website, www.nbim.no.

Sustainability due diligence

Conducting ongoing due diligence on environmental and social topics in line with international standards is integral to our work as a responsible investor. We seek to identify and assess potential and actual adverse impacts which our portfolio companies may cause, contribute to, or be directly linked to. As a minority investor, we cannot direct companies to take action, but we seek to use our influence to encourage them to take steps to prevent and mitigate these impacts. Our sustainability due diligence process is described on our website.

Abbreviations

|

Abbreviation |

Explanation |

|---|---|

|

AI |

Artificial intelligence |

|

APG |

Algemene Pensioen Groep NV |

|

CAHRA |

Conflict-affected and high-risk areas |

|

CDP |

Carbon Disclosure Project |

|

CEO |

Chief Executive Officer |

|

CRREM |

Carbon Risk Real Estate Monitor |

|

GIC |

Government of Singapore Investment Corporation |

|

HEC |

Hautes Etudes Commerciales |

|

ISO |

The International Organization for Standardization |

|

ISSB |

International Sustainability Standards Board |

|

LLM |

Large language model |

|

MRN |

Mineração Rio do Norte |

|

MW |

Megawatt |

|

NGO |

Non-governmental organisation |

|

NBIM |

Norges Bank Investment Management |

|

OECD |

Organisation for Economic Co-operation and Development |

|

PRI |

Principles for Responsible Investment |

|

SASB |

Sustainability Accounting Standards Board |

|

SBTi |

Science Based Targets initiative |

|

TCFD |

Task Force on Climate-Related Financial Disclosures |

|

TNFD |

Taskforce on Nature-related Financial Disclosures |

|

UN |

United Nations |

|

UK |

United Kingdom |

|

US |

United States of America |

|

UNGPs |

United National Guiding Principles on Business and Human Rights |

Responsible investment 2025

Government Pension Fund Global

Norges Bank Investment Management

Design: TRY

Production: Aksell AS

Images: Halvor Njerve, Olav Vhile, GettyImages, Shutterstock and Unsplash