The benchmark index for the Government Pension Fund Global

Letter sent to the Ministry of Finance, 28 August 2020

Letter sent to the Ministry of Finance, 28 August 2020

The Ministry updated the benchmark index for the bond portfolio with effect from 30 November 2019. Norges Bank manages the government portion of the bond portfolio close to the benchmark index, and changes to the composition of the index will generate a need for transactions in the actual portfolio during the year. In this letter, we present proposals that could reduce the transactions needed to track the index and so enable more cost-effective implementation of our management assignment.

Background

The bonds in the government bond portion of the benchmark index are currently assigned adjustment factors based on their country affiliation. The adjustment factors are based on GDP weights, but limited to twice each country’s market value. The adjustment factors are set for a period of 12 months, but the mandate also requires them to be updated in the event of changes to the market composition of the government bond portion.

In the periods between updates of the adjustment factors, the distribution between countries in the benchmark index will move with changes in market value. The country distribution of the benchmark index is affected by more factors than the country distribution of the bond portfolio. The country weights in the benchmark index move with movements in bond prices and exchange rates, when new government debt is issued, and when bonds drop out of the index for various reasons. The country weights in the portfolio are affected only by the first two of these factors – bond prices and exchange rates (index return).

In periods with substantial issuance of government debt and/or major changes in which bonds are included in the benchmark index, for example as a result of large purchases from the Federal Reserve, the deviation between the benchmark index and the actual portfolio will increase. Country deviations arising between the benchmark index and the portfolio will draw on the Bank’s limit for relative volatility. To keep the government bond portfolio close to the index, the Bank will normally choose to minimise temporary currency deviations of this kind through transactions in the market. At the same time, many of the transactions made to close unintended currency deviations during the year will be reversed in connection with the annual updating of the adjustment factors.

The mandate also requires the adjustment factors to be updated in the event of changes to the market composition of the government bond portion. Since the country weights in the benchmark index move away from the set weights during the course of the year, the country weights when a new market is included may differ considerably from when the adjustment factors were determined in December. The challenges this entails crystallised when Estonia was included in the sub-index from Bloomberg Barclays at the end of June. Had the adjustment factors been updated in this context, this alone would have resulted in transactions in the index of around 100 billion kroner. The Ministry therefore decided in its letter of 24 June, in line with the Bank’s letter of 15 June, that Estonia should not be included in the bond index until the annual update of the adjustment factors takes place.

Proposed adjustments to Section 2-2 of the mandate

The Executive Board proposes amending Section 2-2 (5) on changes to the market composition of the government bond portion. Experience from the operational management of the fund suggests that changes to the market composition of the government bond portion should undergo a special assessment, with the Ministry issuing a phase-in or phase-out plan to enable cost-effective adjustment to changes of this kind. We propose establishing the same type of process for new markets as for new currencies.

A phase-in or phase-out plan might mean that the composition of markets or currencies in the government bond portion change immediately. Other alternatives could be to not change the composition of markets or currencies until the annual update, or setting a plan that runs over a longer period. It is reasonable to expect that such cases will arise rarely, but that they could result in substantial transactions in the benchmark index when they first arise. The proposal to adjust the mandate ensures that every such case would undergo a special assessment.

If the Ministry heeds the Bank’s proposal to amend Section 2-2 (5), it can be adjusted to:

If new currencies or markets are included in or removed from the government bond portion of the benchmark index, the Ministry shall adopt a phase-in plan or phase-out plan.

The index weights assigned to individual markets are defined in Section 2-2 (7). To eliminate unintended deviations between the country distribution of the benchmark index and the country distribution of the actual portfolio, the Executive Board proposes that the country weights in the government bond portion move during the year with the index return in each market, and that the mandate is amended accordingly. The proposed change would help reduce transactions in the operational management of the bond portfolio and so enable more cost-effective management of the portfolio.

Section 2-2 (7) could be adjusted to:

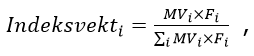

The weight for country i in the government bond portion of the benchmark index is determined according to the following formula:

with MVi and Fi denoting the market value of country i and the associated adjustment factor, cf. Section 2-2, Sub-sections 4 and 5. The index weight for country i shall move with the index return in country i in the period between updates of Fi, and shall be normalised such that they add up to 1.

Other matters

The GDP weights are currently calculated on the basis of historical exchange rates for the past three years. This is in line with the method used by Bloomberg. To reduce further the need for transactions in connection with the annual updating of the adjustment factors, consideration could be given to using more up-to-date exchange rates when calculating the GDP weights. One possibility would be to use the average rates for the past 12 months.

Yours faithfully

Øystein Olsen Jon Nicolaisen