Development of the investment strategy for the Government Pension Fund Global

Norges Bank's letter to the Ministry of Finance 6 July 2010

Norges Bank's letter to the Ministry of Finance 6 July 2010

Norges Bank aims to contribute to the Government Pension Fund Global being managed in a way that achieves the best possible trade-off between expected return and risk. This is reflected in both the operational management of the fund and the strategic advice that we provide. Several factors make it advisable now to assess the investment strategy for the fund in a broader perspective. In its annual report to the Norwegian parliament on the management of the fund, Report No. 10 (2009-2010) to the Storting, the Ministry of Finance discusses a number of concrete issues that may have far-reaching implications for the fund’s investment strategy.

One issue is the role that systematic risk factors are to play in the design of the fund’s benchmark portfolio. This issue was highlighted by the recommendations of professors Ang, Goetzmann and Schaefer in their report to the ministry on the management of the fund[1]. They argued that desired exposure to systematic risk factors should be reflected to a greater extent in the fund’s benchmark portfolio. In Norges Bank’s letter of 23 December 2009 on our active management of the fund, we argued that the management and control of systematic risk must be part of our management task. In its report, the ministry concludes that it will study this matter further.

A second issue is the consequences that greater inclusion of less liquid investments should have for the design of the investment strategy, including the limits for our operational management. In its report, the ministry suggests that it is now appropriate to increase the level of less liquid investments in the fund:

Future work on the investment strategy will focus in particular on evolving the strategy so as to exploit the special characteristics of the Government Pension Fund in the best possible manner… Further development will seek to diversify the risk further and increase the weight of investments that benefit from the Fund’s size, long-term perspective and ability to hold less liquid assets.

We share this view and have previously recommended that the fund’s investment universe should be expanded to include less liquid investments in private equity and infrastructure, as well as real estate.[2]

Norges Bank has previously noted weaknesses in the design of the fund’s benchmark portfolio for fixed income investments. A more appropriate design of the benchmark portfolio cannot be viewed in isolation from the benchmark portfolio’s currency distribution. The recent turmoil in financial markets may warrant a fresh assessment of the basis for the current rules. The principles for determining the fund’s benchmark portfolio, the definition of the fund’s investment universe, and increased investment in less liquid assets affect every aspect of the investment strategy. This letter outlines alternative approaches to these various aspects which could result in a better design of the overall strategy.

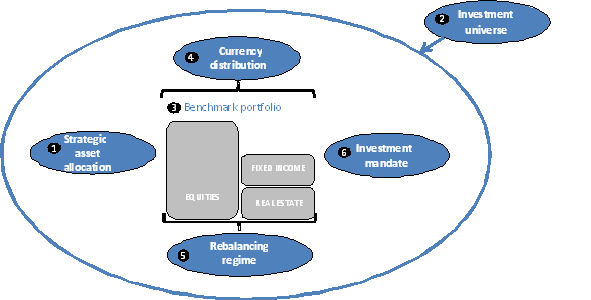

The purpose of the Government Pension Fund Global is to facilitate government savings necessary to meet the rapid rise in public pension expenditures in the coming years, and to support a long-term management of government petroleum revenues. The investment strategy is determined by the Ministry of Finance against this background and has a number of components. The diagram below attempts to illustrate the relationship between these components:

Chart 1: Key components of the fund’s investment strategy.

The strategic asset allocation expresses the desired level of risk. For a large and well-diversified fund such as the Government Pension Fund Global, the expected return will depend on the chosen level of risk. The single most important decision when determining the strategic asset allocation is the size of the allocation to equities. A high allocation to equities can produce a favourable return in the long term, but also demands relatively high tolerance to short-term variations in return.

The fund’s strategic asset allocation is 60 percent equities and 40 percent fixed income instruments. This allocation reflects considerable risk appetite and risk-bearing capacity. The Ministry of Finance has decided that up to 5 percent of the fund may now be invested in real estate. As the real estate portfolio is built up, these investments will be deducted from the allocation to fixed income instruments. A discussion of the fund’s future strategic asset allocation should be based on the portfolio characteristics of the different asset classes.

Equities

Equity investments confer ownership of the underlying production capacity at the companies in which the fund invests, and therefore represent real assets. The return on equity investments can be expected to vary more than the return on fixed income instruments. The risk associated with these variations is the basis for the equity premium. The equity premium is one reason why it is reasonable to expect a higher return on an equity investment than on a fixed income investment. Equity investments should account for the bulk of the fund’s strategic asset allocation, both because the expected return is higher and because equities confer ownership of real capital, which helps to safeguard the fund’s long-term purchasing power.

Fixed income

The fund’s strategic allocation to fixed income instruments currently includes both real (inflation-linked) bonds and nominal bonds. Investments with nominal and real returns play different roles in the portfolio. It is reasonable to consider whether this should be reflected in the strategic asset allocation.

Nominal fixed income investments of high credit quality – primarily government debt issued in local currency – offer a “safe” (nominal) periodic return and reduce fluctuations in the fund’s overall nominal return. This characteristic can be important in periods of economic downturn and in periods of rapidly growing risk aversion and negative returns in equity markets. We witnessed such a period in connection with the financial crisis in 2008/09. One additional factor is that government securities of high credit quality are generally liquid. This characteristic is important if we are to be in a position to rebalance the portfolio at all times.

However, nominal fixed income investments provide no protection against an unexpected rise in inflation and therefore make less of a contribution towards safeguarding the fund’s long-term international purchasing power. The combination of historically low government bond yields and growing government debt might suggest that we should reassess the proportion and composition of nominal fixed income investments in the portfolio. Inflation-linked bonds have different portfolio characteristics. Issuers of inflation-linked bonds undertake to pay the investor a given real return. The risk associated with the real return is essentially limited to the borrower’s ability to fulfil his obligations (credit risk).

Inflation-linked bonds are issued primarily by national authorities, and so the credit risk is considered to be relatively low. In contrast to nominal fixed income instruments, investments in inflation-linked bonds provide direct protection against an unexpected rise in inflation and so help reduce uncertainty about the fund’s long-term purchasing power.

Real estate

The long-term return on real estate investments is influenced by structural factors such as demographics and inflation. Tenancy agreements are often indexed to inflation, and so real estate investments can serve as inflation protection in the portfolio. The long-term return and risk profile of real estate investments will share common features with the fund’s investments in inflation-linked bonds, even though real estate investments mainly take the form of a contribution of equity.

The similarities between real estate and inflation-linked investments should be reflected in the strategic asset allocation. One way of achieving this might be to establish a separate strategic asset class for investments that help safeguard the fund’s long-term real return. Examples of investments that could be included in this strategic asset class are investments in inflation-linked bonds, real estate and infrastructure.

Investments in real estate and infrastructure confer direct ownership of real assets and an expected return in the form of stable, inflation-adjusted cash flows. This inflation adjustment comes from the periodic income from these investments often being linked to movements in inflation. An increase in this type of real asset in the portfolio should be aimed at, because this can help reduce uncertainty about developments in the fund’s international purchasing power. Increased inclusion of real assets in the portfolio should be matched by reduced inclusion of nominal fixed income investments. Investments in other real assets, such as real estate and infrastructure, will also be less liquid. The fund is well-suited to harvesting the liquidity premium from such investments, as the fund has no short-term liquidity needs.

Based on this review of the portfolio characteristics of the different asset classes, we believe that there is reason to consider changing the current strategic asset allocation with allocations to equity instruments, fixed income instruments and real estate so that it better reflects the portfolio characteristics of the different types of investment.

One possible approach might be:

The rest of this letter is based on such an approach. The discussion in the following sections assumes that the fund’s strategic allocation to equity investments of 60 percent is retained. The allocation to nominal fixed income instruments in this model will be 40 percent less the value of investments in the proposed asset class of other real assets.

Investments included in the asset class of other real assets, such as real estate, infrastructure and inflation-linked bonds, may not be very liquid. It will not therefore be possible to control the level of these investments through frequent transactions. Investment opportunities will also vary over time. The supply of suitable real estate and infrastructure investments will not be constant. Investment opportunities may be affected by such factors as the supply of alternative sources of financing, such as bank loans, and interest from fund managers. Investment opportunities may also be affected by political factors, such as decisions to allow private risk capital in the financing of infrastructure projects. The characteristics of this asset class therefore suggest that there should not be a fixed strategic allocation to this asset class, but a long-term strategic target.

The investment universe defines the fund’s investment opportunities. These opportunities must be adequately communicated, understood and anchored in all parts of the management structure. This is ensured by the Ministry of Finance as owner of the fund taking responsibility for defining the investment universe.

At the fund’s inception in 1996, the investment universe was limited to government bonds. Since then, the investment strategy has gradually been expanded to include a broader set of investment opportunities. Under the current rules, the fund is to be invested in:

The rules also permit the use of financial instruments, including derivatives naturally related to these asset classes, and investments in commodity-based instruments.

The Government Pension Fund Global has distinguishing characteristics that set it apart from the average investor. Norges Bank has highlighted the fund’s size and long-term horizon as the most important of these distinguishing characteristics. Given the fund’s size and long-term horizon, there is little to suggest that the fund’s investment opportunities should be more limited than those of comparable funds.

With the introduction of unlisted real estate investments as part of the universe in autumn 2007, the investment universe was expanded to include unlisted, less liquid assets. It is now natural to consider other unlisted investment opportunities.

We have previously recommended that the fund’s investment universe be expanded to include investments in private equity and infrastructure. This is in keeping with the line taken by the Ministry of Finance in Report No. 10 (2009-2010) to the Storting, namely that the weight of less liquid assets in the portfolio should be increased. Assuming such a change, the fund’s investment universe will approach what is usual for comparable funds. The fund is well-suited to bearing the risk and harvesting potential gains from investments in less liquid assets, as the fund does not have short-term liquidity needs. Nor is the fund subject to rules that could require adjustments to the portfolio at inopportune times.

In this letter, we have outlined a model where the strategic asset allocation consists of equity investments, nominal fixed income investments and investments in other real assets which help safeguard the fund’s long-term real return. With such a model, new investment opportunities should be assessed on the basis of the characteristics they represent and assigned to one of the three strategic asset classes.

In the same way as with other equity investments, investments in private equity would represent real assets through ownership of the underlying production capacity at the unlisted portfolio companies. As a result, any investments in private equity by the fund would be part of the asset class of equity investments.

Investments in traditional infrastructure projects would, in portfolio terms, be expected to contribute stable, inflation-adjusted cash flows and so help safeguard the fund’s long-term international purchasing power. Any investments in infrastructure would consequently be part of the asset class of other real assets.

There would still be a number of investments that lie outside the fund’s investment universe, such as investments in timberland, farmland, patents, commodities and insurance products. These are investments that are often included in the portfolios of other large, long-term investors. As Norges Bank builds up experience and expertise in less liquid investments in real estate, private equity and infrastructure, it will be natural to consider further expansion of the investment universe.

On the basis of the strategic asset allocation, the Ministry of Finance defines a detailed benchmark portfolio for each asset class.

The benchmark portfolio for equity instruments consists of shares in listed companies in developed and emerging markets and breaks down into 50 percent Europe, 35 percent Americas and 15 percent Asia. The benchmark portfolio for fixed income instruments consists of nominal and inflation-linked bonds which have a remaining maturity of more than one year and are rated BBB or higher, and breaks down into 60 percent Europe, 35 percent US and Canada, and 5 percent developed markets in Asia.

The benchmark portfolios have several functions:

For liquid investments in the equity and fixed income markets, the issue is the appropriate level of ambition in the design of the benchmark portfolio. One topical question is whether it is possible or desirable to build a number of systematic risk factors into the benchmark portfolio, or whether we are even now overburdening the benchmark portfolio at the expense of the aims of simplicity, transparency and verifiability.

For less liquid investments, it will not be possible in practice to establish transparent, verifiable, liquid and investable benchmark indices. The fund’s real estate investments fall into this category. For this asset class, the approach currently applied means that Norges Bank, on the basis of its mandate, is to attempt to generate a net return that matches or exceeds the Investment Property Databank (IPD) Global Property Benchmark for the Government Pension Fund Global (IPD SPU). The IPD SPU is based on IPD’s Global Property Benchmark, but adjusted for factors such as actual leverage and estimates of management and tax costs. The IPD SPU is not simple, transparent, investable or verifiable, and cannot play the same role as the benchmark index for the liquid asset classes. Development of the investment strategy along the lines presented by the Ministry of Finance in Report No. 10 (2009-2010) to the Storting, with increased inclusion of less liquid assets, would have to take place without concrete benchmark portfolios for these investments. The role that concrete benchmark portfolios play for liquid investments must then be played by limits or targets in the investment mandate.

The following sections review the basis for the benchmark portfolio’s currency distribution, look more closely at the degree to which systematic risk factors can be reflected in the benchmark portfolio, and describe how the benchmark portfolios for the three asset classes in our model might be designed.

The Government Pension Fund Global is part of Norway’s national wealth. The fund makes it possible to transfer parts of the wealth held by the government in the form of petroleum resources into savings and investments in global financial markets. The fund shelters the domestic economy and industrial structure from fluctuations in oil prices. When domestic production capacity is fully utilised, the fund can only be used to import goods and services. The aim of the management of the fund is to maximise the fund’s long-term international purchasing power. Key issues in the design of the strategy are the degree to which this international purchasing power is exposed to currency risk, and how this currency risk can best be managed.

One approach is that the currency distribution in the benchmark portfolio should correspond to the currency distribution of the fund’s anticipated future obligations. If the fund’s obligations are defined as Norway’s future net imports, the currency distribution of future net imports will be the currency distribution that minimises the currency risk.

Assuming purchasing power parity, differences in inflation will be matched by movements in exchange rates. In the long term, this may be a reasonable assumption. The benchmark portfolio should, in that case, be determined on the basis of expected return and diversification of risk, not on how the fund is to be used in the future.

Empirical analyses of long time series have previously indicated that deviations from purchasing power parity can be considerable and persistent. Some weight has therefore been given to the fund’s future obligations when determining the currency distribution for the benchmark portfolios. The desired currency distribution has been expressed through regional weights for the benchmark portfolio. The regional weights have been modified on a number of occasions since the fund’s inception. The need for diversification has been given more weight as the fund has grown in size, whereas the fund’s obligations in the form of future imports have been toned down.

There are reasons for reviewing whether today’s approach based on regional weights in the benchmark portfolio serves to support the overall aim of the management of the fund. There is no unambiguous relationship between regions and currencies, or between markets and currency exposure. This can be illustrated as follows:

The need for effective asset allocation should probably be given greater weight in the design of the benchmark portfolios:

Whether it is appropriate to retain today’s structure with regional weights needs to be reviewed. One possible approach would be to assume that the fund’s international purchasing power is best safeguarded through ownership of the means of production, as it is this capacity that generates the supply of goods and services that the fund can purchase.

In our opinion, there is much to suggest that the benchmark portfolio for equity investments should, in principle, be market-weighted. A strategy formulated on the basis of market value weights would ensure diversification and gives broad exposure to ownership of the production capacity that generates the supply of goods and services on the world market and forms the basis for our future imports. This change would mean including more US and Asian equities in the benchmark portfolio at the expense of European equities. We have carried out calculations which indicate that a change of this kind could be implemented within a reasonable time frame.

The benchmark portfolios for fixed income investments should be based on different criteria. A market-weighted benchmark for fixed income investments could have unfortunate consequences, as a high level of debt could result in high representation in the benchmark portfolio. Our view is that the fixed income benchmark should be weighted on the basis of the production capacity that is to service the debt. GDP weights would seem to be the most appropriate option.

More about the fund’s numéraire

The composition of the benchmark portfolios determines the fund’s strategic currency exposure and is currently used to determine the fund’s value and returns. It is debatable whether this is appropriate. One alternative to using the currency composition of the benchmark portfolios to ascertain value and returns would be to perform this type of calculation on the basis of a standardised currency basket such as the IMF’s Standard Drawing Rights (SDRs). The SDR weights are set by the IMF’s Executive Board and are intended to reflect each currency’s relative importance for world trade and the currency’s share of IMF member states’ foreign exchange reserves.

In connection with the evaluation of our active management of the fund, the Ministry of Finance commissioned a report by professors Ang, Schaefer and Goetzmann. Norges Bank has noted that this report contains recommendations that desired exposure to systematic risk factors should be reflected in the fund’s benchmark portfolio.

The Ministry of Finance follows up these recommendations in Report No. 10 (2009-2010) to the Storting and concludes that systematic risk factors should be given greater attention in the management of the fund, but that it is too early to take a position on whether systematic risk factors should be included in the benchmark index. The ministry also writes that there is a need to investigate further which factors should be included, which exposure would then be desirable, and how the fund is to achieve exposure to these factors.

In the appendix to our letter on active management of 23 December 2009, we wrote as follows:

Common to our report and the standpoint of the ministry’s external advisers is the view that today’s benchmark portfolios do not fully represent the best investment strategy for the fund.

Norges Bank has emphasised that our management will expose the fund to systematic risk factors to a greater or lesser extent, and that the management and control of systematic risk must therefore be included as a key element of our management task. Norges Bank needs to take an active approach to the measurement, control and reporting of systematic risk as part of the operational management of the fund.

The development of the investment strategy should reflect the fact that the fund is particularly well-suited to bearing certain types of systematic risk and should probably therefore have different exposure to these sources of systematic risk than the market portfolio would indicate. Although some systematic risk factors could have a major impact on returns in the short term, it would probably be to the fund’s disadvantage in the long term if we do not exploit these opportunities.

The benchmark portfolios should reflect desired exposure to sources of systematic risk where it is possible to construct simple, transparent, investable and verifiable indices. In terms of the benchmark index for equity investments, this may be possible in terms of desired exposure to small-cap stocks (the size premium) and structurally stronger growth in emerging markets. On the fixed income side, it is possible to define desired exposure to various types of credit.

For other risk premiums described in the literature, it is difficult to find simple decision parameters. Various approaches can be used to model systematic risk, such as momentum, value and volatility in the equity market, and carry and liquidity in the fixed income market. These factors are dynamic in the sense that a portfolio intended to represent stable exposure to them will evolve over time.

There are no generally accepted definitions or ways of constructing risk factors. Nor is there any answer as to what the optimal composition of dynamic factors of this type might be. An approach where the owner attempts to define a benchmark portfolio which reflects all dimensions of risk to which the fund should be exposed would, to a great extent, need to be based on discretion. This discretion should be part of the operational management of the fund. The Ministry of Finance should avoid introducing systematic risk factors in the benchmark portfolios which undermine transparency and verifiability or which increase transaction volumes or are not investable in practice.

Today’s benchmark portfolio for equity investments is considered to be a reasonable approximation of the investment opportunities in listed equities. In this letter, however, we have discussed two matters which may have implications for the future design of the equity benchmark portfolio.

First, we have questioned whether it is appropriate to retain the current structure with regional weights. In our opinion, there are factors suggesting that the benchmark portfolio for equity investments should be weighted by market value without separate regional allocations. Second, in our discussion of systematic risk factors in the benchmark portfolios, we have argued that it may be possible to construct simple, transparent, investable and verifiable indices for the fund’s exposure to small-cap stocks (the size premium) and structurally stronger growth in emerging economies. Consideration should probably therefore be given to whether desired exposure to these sources of systematic risk should be reflected in the benchmark portfolio for equity instruments.

In the appendix to our letter on active management of 23 December 2009, we wrote as follows:

The benchmark portfolio for fixed income investments does not fully represent the characteristics of this asset class. The definition of the benchmark portfolio can introduce bias, because it excludes bonds with short maturities, bonds downgraded below a certain ratings level, and floating-rate bonds. Through active management, we can achieve a portfolio which represents the fixed income market in a broader and more cost-effective way

We have previously highlighted liquidity as an important portfolio characteristic of the fund’s nominal fixed income investments. The fund will need a certain amount of liquidity in order to carry out rebalancing, especially in periods of stress in financial markets. A portfolio of nominal bonds contains a degree of natural liquidity due to bonds maturing. This liquidity is not currently part of the fund’s benchmark portfolio. Consideration should be given to whether the benchmark portfolio for nominal fixed income investments should be expanded to include money market instruments. In isolation, this would result in a lower duration than for today’s benchmark portfolio.

When specifying the benchmark portfolio for nominal fixed income investments, consideration should be given to whether the fund’s exposure to the term structure premium [4] should depart from that of the average investor. In this context, it is important to view the fund’s exposure to the term structure premium in nominal bonds in relation to exposure to the term structure premium in inflation-linked bonds and other investments that can safeguard long-term real returns.

The fund’s nominal fixed income investments can help reduce variations in the fund’s return. This presupposes, however, that the portfolio consists of instruments of high credit and liquidity quality, which would indicate that the benchmark portfolio for nominal fixed income instruments should consist of instruments issued in the major investable currencies. At present, this effectively means bonds issued in US dollars, pounds sterling, euro and Japanese yen.

The risk premium from investing in non-government bonds can be divided into several components. Besides a liquidity premium, the credit premium includes compensation for expected losses in the event of default. This latter component has many similarities with the risk premium that an investor can harvest in the equity market. A higher proportion of non-government bonds in the benchmark portfolio for nominal fixed income investments would increase this asset class’s covariance with the allocation to equity instruments. This would serve to reduce the diversification effect that can be achieved through allocation to safe issuers. In our opinion, consideration should be given to whether the strategic role played by nominal fixed income investments could best be achieved through a narrower definition of the benchmark portfolio than is currently applied.

Norges Bank intends to come back with a specific recommendation on the design of the benchmark portfolio for the fund’s nominal fixed income investments later in 2010. Our analysis will include:

The benchmark index for what we refer to in our model as other real assets could, for example, be based on the market for inflation-linked bonds. In our opinion, this could be an appropriate way of establishing a transparent and simple yardstick for this type of investment. With this model, specific benchmark portfolios would not therefore be established for alternative investments such as real estate and infrastructure.

The benchmark index would not be investable to the extent that we would prefer. It would need to be supplemented with limits in Norges Bank’s investment mandate. Regulation of risk stemming from the fund also exploiting investment opportunities that fall outside the benchmark index, such as investments in infrastructure, could be achieved through explicit limits in the investment mandate. The benchmark index could continue to serve as a suitable management tool, as it reflects the portfolio characteristics that we are aiming to achieve.

In its guidelines for the management of the fund, the Ministry of Finance has laid down rules on the rebalancing of the actual benchmark portfolio. Rebalancing ensures a more or less fixed asset allocation over time in line with the owner’s expressed risk preferences. A fixed asset allocation is also justified by an expectation that the return on equities will show mean-reverting properties and that periods of high returns tend to be followed by periods of low returns and vice versa.

The rebalancing rules currently have two main parts: rules on how inflows of new capital into the fund are to be managed in the benchmark portfolio through continuous rebalancing, and rules for full rebalancing.

The rules on managing the monthly inflows of new capital ensure that the weights in the actual benchmark portfolio move towards the strategic asset allocation by requiring that this capital is invested in the sub-portfolios that have a lower allocation in the actual benchmark portfolio than in the strategic benchmark portfolio.

The rules for full rebalancing are defined on the basis of six sub-portfolios: one for each of the three regions for equity and bond investments respectively. Full rebalancing is to be carried out if the weight of one of these six sub-portfolios exceeds a predetermined limit.

In this letter, we have outlined a model where the strategic asset allocation for the fund consists of three asset classes: equity investments, nominal fixed income investments and other real assets. The last of these three will consist largely of less liquid investments which cannot, by definition, be covered by mechanical rebalancing rules. For the fund’s less liquid real estate investments, the solution currently chosen is for real estate investments to be measured at their latest available market value and excluded from the rebalancing calculations for both partial and full rebalancing.

The rebalancing rules are defined on the basis of the regional weights. If the regional weights in the benchmark portfolios for equity and bond investments are abolished, the rebalancing rules will have to be changed.

If the benchmark portfolio for nominal fixed income investments is expanded to include money market investments, this will serve to increase the structural liquidity of the benchmark portfolio. This would make it natural to undertake a review of the rules on the management of inflows of new capital into the fund.

One such aspect is the current direct link between the timing of transfers of new capital into the fund and purchases of risk-bearing assets in the benchmark portfolio. The level of transfers to the fund has varied considerably over time, due partly to movements in the price of oil. The direct link between transfers and investments may mean that the fund increases its exposure to risk-bearing assets at inopportune times. One alternative strategy could be to establish rules that ensure that inflows of new capital are phased into risk-bearing assets at a more even rate. Money market investments in the benchmark portfolio for nominal fixed income instruments would make such a strategy possible. In this context, consideration should also be given to how any future withdrawals from the fund might best be managed.

Another aspect is that the rebalancing rules are not currently in the public domain. The full rules on rebalancing are very detailed. In principle, we believe that the rules for how and when rebalancing is to be carried out should be simple, predictable, verifiable and publicly available.

Any set of rules on managing inflows of new capital and rebalancing the benchmark portfolio will need to be based on a trade-off between the owner’s tolerance of deviations on the one hand and transaction costs and operational factors on the other. Consideration should be given to establishing a set of rules which mean that the timing of the fund’s investments in risk-bearing assets is less closely linked to inflows of new capital into the fund. This would mean allowing the fund’s actual portfolio to drift slightly further away from the actual benchmark portfolio within overall limits set by the ministry.

In addition, consideration should be given to simplifying the current structure for managing inflows into the fund. At present, new capital is transferred to the fund monthly. Capital to be transferred to the fund, including Norges Bank’s purchases of foreign exchange and transfers from the SDFI[5], accumulates during the month in a buffer portfolio which is currently managed as part of Norges Bank’s foreign exchange reserves, not as part of the fund. If money market investments are introduced into the benchmark portfolio, the fund should, in principle, be able to handle daily inflows of new capital. There would then no longer be a need for a separate buffer portfolio.

The investment mandate sets out the framework for the operational management of the fund.

The mandate needs to be designed such that the investment strategy is implemented in the best possible way.

The main objective specified in the current rules is for Norges Bank to seek to achieve the highest possible return on investments in foreign currency within the investment limits set out in the regulations and other guidelines.

The current rules are designed for investments in financial instruments with frequently quoted market prices. In this model, the benchmark portfolio is intended to reflect the owner’s risk preferences. The starting point is that it is possible to draw a clear distinction between the owner’s strategic decisions and the operational decisions for which Norges Bank is responsible. The rules can be understood such that Norges Bank’s objective is to generate a higher risk-adjusted excess return than the benchmark portfolio.

Our understanding of our management task is expressed, for example, in our letter on the active management of the fund of 23 December 2010, where we wrote as follows:

Through our management of the fund, we aim to build a portfolio which achieves the best possible trade-off between expected return and risk. This is reflected both in the operational management of the fund and in the advice we give the Ministry on the fund’s investment strategy.

Our implementation of the management task is based on time-varying investment opportunities in the markets. With time-varying investment opportunities, the benchmark portfolio will not represent the “correct” portfolio at any time. Management of various sources of systematic risk will then be necessary to achieve the main objective of the mandate.

In Report No. 10 (2009-2010) to the Storting, the Ministry of Finance writes as follows:

A better use of the Fund’s distinctive features will mean that the investment strategy will continue to be developed in the direction of unlisted and other less tradable assets… There are no investable benchmark indices for this type of investments. It is therefore not possible to distinguish between overarching strategy choices and decisions on operational execution in the same manner as for listed shares and bonds. Such investments require a different division of work between client and manager, with a larger degree of delegation.

Norges Bank shares the ministry’s view that increased inclusion of assets for which there are no investable benchmark indices will require a slightly different division of labour between client and operational manager. The fund is already exposed to risk that can be captured neither by the benchmark portfolio nor by the limit on tracking error. The tempo and orientation of the fund’s investments in real estate will be significant for the fund’s absolute return and for the relationship between return and risk. With a larger proportion of less liquid assets in the portfolio, this type of risk will increase.

In this letter, we have described a model where the investment strategy for the fund is expressed to a greater extent through concrete targets and limits for the management of the fund. The following provides some examples of how the alternative that we have outlined could be expressed in a mandate for Norges Bank.

[1]Evaluation of Active Management of the Norwegian Government Pension Fund – Global, 14 December 2009.

[2] Recommendations concerning the investment strategy for the Government Pension Fund – Global, letter to the Ministry of Finance of 20 October 2006.

[3] For the Government Pension Fund Global as a whole.

[4] Several studies show that a strategy where the investor borrows fixed income instruments with a short maturity and invests in fixed income instruments with a long maturity, when the yield spread is considerable, will generate an excess return over time. The return achieved by an investor using such a strategy can be viewed as reaping a term structure premium. A more detailed discussion of the term structure premium can be found in our letter of 23 December 2009.

[5] The State's Direct Financial Interest in petroleum activities.

Yours faithfully

| Svein Gjedrem | Yngve Slyngstad |